Fixed vs Variable Mortgage Calgary 2026 | Should You Lock In Now?

Fixed vs Variable Mortgage in Calgary (2026): Why Locking In May Be the Safer Move Right Now

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

Mortgage rates in Canada—and specifically here in Calgary—are starting to trend upward again. After a period where variable rates often came out ahead, the risk equation has shifted.

If you’re trying to decide between a fixed or variable mortgage today, the key question is no longer just “which is cheaper right now?” — it’s how much risk are you willing to take on?

What’s Changed: Rates Are Gradually Rising Again

Over the past year, many buyers benefited from improving affordability after the housing correction. But now:

-

Bond yields are creeping higher

-

Lenders are adjusting fixed rates upward

-

Variable rates remain exposed to future increases

This creates a very different environment than what borrowers faced even 6–12 months ago.

The Real Question: Certainty vs Flexibility

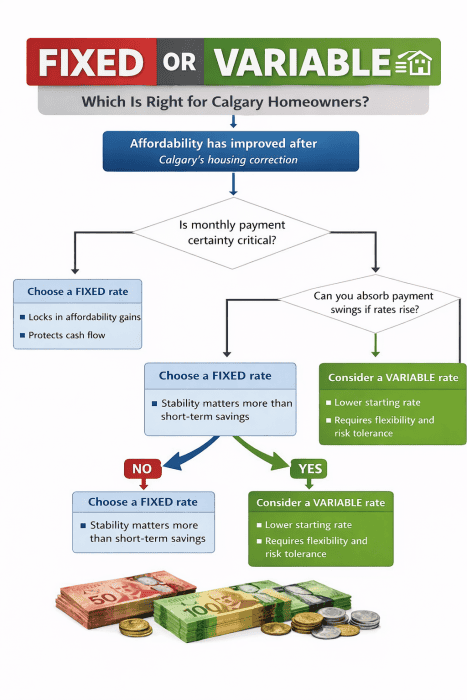

Your decision tree graphic captures this perfectly.

At its core, the choice comes down to one key question:

Is monthly payment certainty critical to you?

If the answer is yes, a fixed rate is usually the better fit.

If the answer is no, then you need to ask:

Can you comfortably absorb payment increases if rates rise further?

Right now, that second question matters more than ever.

Why Fixed Rates Are Becoming More Attractive in Calgary

Here’s what I’m seeing with clients in Calgary right now:

1. Cash Flow Is Getting Tighter

With higher home prices and cost of living, many borrowers don’t have as much room to absorb rising payments.

A fixed rate:

-

Locks in your payment

-

Protects your monthly budget

-

Eliminates uncertainty

2. The Risk of Being Wrong Has Increased

Variable rates can still win—but only if rates stabilize or fall.

If rates continue rising:

-

Payments can increase significantly

-

Stress levels go up

-

Flexibility becomes a liability instead of an advantage

Right now, the downside risk is larger than the potential upside reward.

3. Fixed Rates Lock In Today’s Affordability

Even though fixed rates are slightly higher than they were, they still:

-

Lock in your current qualification

-

Protect your purchasing power

-

Remove future surprises

In a rising rate environment, that stability has real value.

When a Variable Rate Still Makes Sense

Variable isn’t “wrong”—it just requires a higher risk tolerance right now.

It may still be a fit if you:

-

Have strong cash flow and savings

-

Can handle payment increases without stress

-

Believe rates will stabilize or decline in the near future

But this is no longer the “default smart choice” it once was.

Calgary-Specific Insight: Why This Matters More Locally

In Calgary, many buyers are:

-

Stretching slightly more on affordability

-

Entering the market after sitting out during higher rates

-

Managing variable income (commission, bonuses, self-employed)

That makes payment stability more valuable here than in lower-cost markets.

Simple Rule of Thumb (2026)

-

Want stability and peace of mind → Choose fixed

-

Comfortable with risk and volatility → Consider variable

But today, more borrowers are landing on fixed—not because it’s exciting, but because it’s safer.

FAQ: Fixed vs Variable Mortgages in Calgary

Is it better to go fixed or variable in 2026?

Right now, fixed rates are generally the safer option due to rising interest rate risk.

Will variable rates come down?

They might—but timing is uncertain, and borrowers need to be able to handle increases in the meantime.

Can I switch later if I choose fixed?

Yes, but there may be penalties depending on your lender and timing.

Final Thoughts

This isn’t about predicting the market perfectly.

It’s about choosing a mortgage that lets you:

-

Sleep at night

-

Stay in control of your finances

-

Avoid unnecessary risk

Right now, for many Calgary homeowners, that points clearly toward locking in a fixed rate.

Need Help Deciding?

If you’re unsure which direction makes sense for your situation, I can walk you through the numbers and stress-test both options.

Author Bio

Mark Herman is a Calgary-based mortgage broker with 22 years of experience and an MBA in Finance. He helps homebuyers and investors make smarter mortgage decisions by focusing on strategy, risk management, and long-term financial outcomes.