Calgary Bridge Financing | Buy Before You Sell in Alberta

Buying a new home before your current home sells can feel impossible.

You find the right property. The closing date is coming fast. Your existing home is listed, but it has not sold yet. Your down payment is tied up in equity. The bank may not be able to move quickly enough. And now you are stuck between two houses, two timelines, and a lot of pressure.

한국 신용기록으로 캐나다 모기지 가능할까? | 캘거리 한인 모기지 전문가

한국 신용기록으로 캐나다에서 주택담보대출(모기지)을 받을 수 있을까요? | 앨버타 한인 커뮤니티를 위한 모기지 가이드

작성자: Mark Herman, MBA – 22년 경력의 모기지 전문가

앨버타 한인들을 위한 특별한 모기지 솔루션

캘거리(Calgary), 에드먼턴(Edmonton), 그리고 앨버타 전역에 거주하는 많은 한인들은 집을 구매할 때 같은 문제를 경험합니다.

Korean Mortgage Program in Alberta: Use Your Korean Credit History to Buy a Home in Canada

Korean Mortgage Program in Alberta: Can Your Korean Credit History Help You Buy a Home in Canada?

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

A Unique Mortgage Solution for Alberta’s Korean Community

Many Korean families moving to Calgary, Edmonton, and other Alberta communities face the same challenge when buying a home in Canada:

Down Payment Verification Requirements in Canada | Calgary Mortgage Broker

Down Payment Verification Requirements in Canada: How to Avoid Mortgage Approval Delays

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience in getting down payments to work in sticky situations and tight spots.

One of the most common reasons mortgage approvals are delayed is incomplete down payment documentation. With Calgary’s summer real estate market remaining active and purchase activity staying strong across Alberta, lenders are paying close attention to verifying the source and availability of down payment funds.

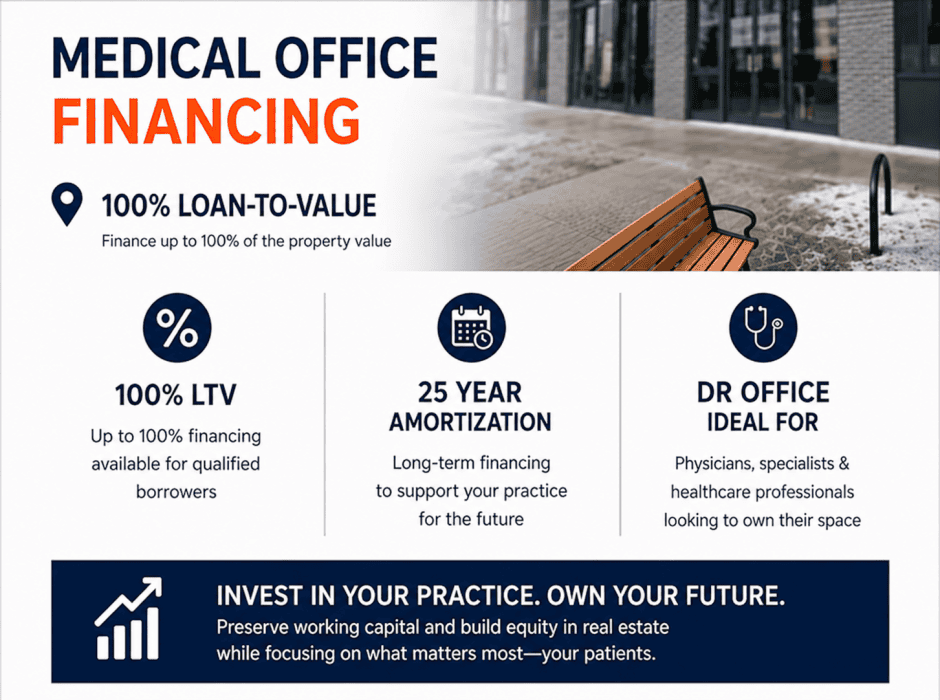

100% Medical Office Financing in Canada: How Physicians Can Buy a Clinic with No Down Payment

100% Medical Office Financing in Canada: How Physicians Can Buy a Clinic with No Down Payment

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience and an MBA in Finance, who still answers his own phone from 9 – 9 x 365.

Many physicians dream of owning their medical office instead of paying rent to a landlord. Yet one of the biggest obstacles is coming up with the down payment needed to purchase commercial real estate.

Korean Mortgage in Canada Using Korean Income & Credit History | Calgary Mortgage Broker

Korean Home Buyers in Canada: Get a Mortgage Using Korean Income, Korean Tax Documents, and Korean Credit History

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience specializing in unique and difficult to do deals.

Buying a home in Canada can be challenging if you recently arrived from Korea or still earn most of your income there. Many (as in ALL) of the traditional Canadian lenders (Big6- banks) require extensive Canadian employment history, Canadian tax returns, and established Canadian credit.

Mortgage Financing Fell Through After Waiving Conditions? How We Save Calgary Home Purchases Fast

Mortgage Financing Fell Through After Waiving Conditions? Here’s How We Save Calgary Home Purchases Fast

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

One of the most stressful calls we get is from a buyer who says:

“My bank just declined the mortgage… and we already waived financing conditions.”

Unfortunately, this is happening more often lately.

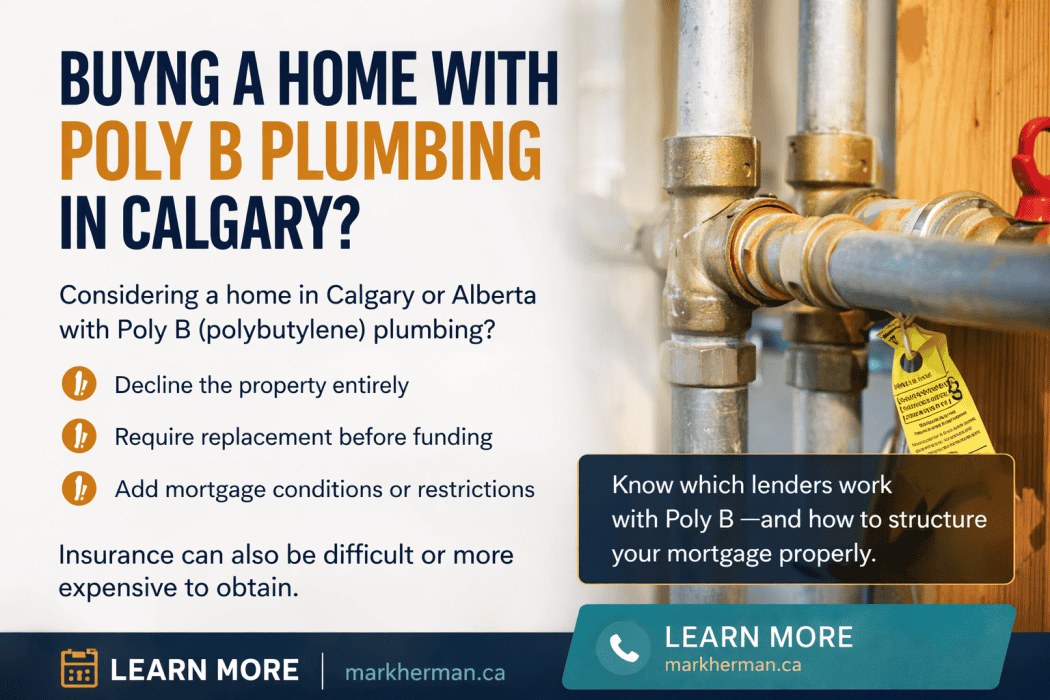

Should You Replace Poly B Before Selling in Alberta?

Should You Replace Poly B Plumbing Before Selling Your Home in Alberta?

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

If you’re selling a home with Poly B plumbing in Alberta, you’re facing a key decision:

Replace it now—or let buyers deal with it?

Buying a Home With Poly B Plumbing in Alberta (2026 Guide)

Buying a Home in Alberta With Poly B Plumbing (2026 Guide for Buyers & Sellers)

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

Buying a home with Poly B plumbing in Alberta can feel like a deal-breaker—but it doesn’t have to be. The reality is that thousands of homes in Calgary and across Alberta still have Poly B, and many are financed every year.

Divorce and Mortgage Options in Calgary: What to Know Before You Sign

Divorce and Mortgages in Canada: What You Need to Know Before Signing a Separation Agreement

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience, specializing in complicated and standard divorces in Alberta and BC.

Divorce is one of the most stressful financial events you’ll go through. Emotions are high, timelines are tight, and most people just want to get things settled and move on.