Should You Replace Poly B Before Selling in Alberta?

Should You Replace Poly B Plumbing Before Selling Your Home in Alberta?

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

If you’re selling a home with Poly B plumbing in Alberta, you’re facing a key decision:

Replace it now—or let buyers deal with it?

The answer can significantly impact your sale price, time on market, and deal success rate.

How Poly B Affects Selling Your Home

Poly B creates:

- Buyer hesitation

- Financing complications

- Insurance concerns

Full buyer-side breakdown:

→ https://markherman.ca/how-to-buy-a-home-in-alberta-with-poly-b-plumbing/

Option 1: Replace Poly B Before Listing

Pros:

- Higher sale price

- More buyer interest

- Fewer deal conditions

Cons:

- Upfront cost

- Renovation hassle

Option 2: Sell As-Is With Poly B

Pros:

- No upfront cost

- Faster listing

Cons:

- Lower offers

- More failed deals

- Smaller buyer pool

What the Calgary Market Typically Does

Most sellers:

- Do NOT replace upfront

- Accept a negotiated discount

How Much Value Does Replacement Add?

Typical:

- Replacement cost: $8K–$20K

- Value increase: often similar or slightly higher

But the real benefit is:

Deal certainty

When You SHOULD Replace Poly B

- Competitive market

- Higher-end home

- You want top dollar

When You SHOULDN’T Replace It

- Entry-level home

- Investor buyers

- Fast sale priority

Negotiation Strategy for Sellers

If not replacing:

- Price slightly below market

- Be transparent upfront

- Expect inspection-based negotiation

Pricing strategy guide:

→ https://markherman.ca/home-appraisal-alberta/

FAQ

Do buyers always ask for a discount?

Almost always.

Does Poly B stop homes from selling?

No—but it narrows the buyer pool.

Bottom Line

Replacing Poly B doesn’t always increase profit—but it often increases certainty and speed.

Author Bio

Mark Herman is a Calgary mortgage broker with 22 years of experience helping sellers and buyers navigate complex property issues.

RRSP vs TFSA vs FHSA for Down Payments in Canada (2026 Complete Guide)

RRSP vs TFSA vs FHSA for Down Payments in Canada (2026 Guide)

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience in First Time Buyers and Move Ups, and New Builds, in Calgary, Alberta & Victoria, BC.

If you’re buying a home in Canada, you have three powerful tools to build your down payment: RRSP (Home Buyers’ Plan), TFSA, and FHSA.

Used properly, these accounts can combine into $100,000+ per person tax-efficiently—but the rules, tax treatment, and transfer strategies are very different.

This guide breaks it down clearly—and shows how to stack them strategically.

Quick Comparison: RRSP vs TFSA vs FHSA

| Feature | RRSP (HBP) | TFSA | FHSA |

|---|---|---|---|

| Tax deduction on contribution | ✅ Yes | ❌ No | ✅ Yes |

| Tax-free withdrawal | ⚠️ Yes (if repaid) | ✅ Yes | ✅ Yes (if buying home) |

| Repayment required | ✅ Yes (15 years) | ❌ No | ❌ No |

| Max usable for down payment | $60,000 per person | No limit | $40,000 lifetime |

| First-time buyer required | ✅ Yes | ❌ No | ✅ Yes |

RRSP Home Buyers’ Plan (HBP): Powerful—but Comes With Strings

How it works

The RRSP Home Buyers’ Plan allows you to withdraw up to:

$60,000 per person

-

Couples can access $120,000 combined

-

Withdrawals are not taxed upfront

-

BUT treated like a loan to yourself

Key rules

-

Must repay over 15 years

-

Payments start after a grace period (typically year 2–5 depending on timing)

-

Missed payments = taxable income

What the chart got right…

✔ Tax deductible going in

✔ Tax-deferred on withdrawal

✔ Contribution room is lost permanently

What it missed (important nuance)

-

It’s not truly tax-free—it’s a tax deferral

-

Repayment reduces your future investing capacity

TFSA: The Most Flexible (But No Tax Break Up Front)

How it works

-

Contributions are not tax deductible

-

Growth and withdrawals are completely tax-free

-

No restrictions on use (including down payment)

Key advantages

✔ Withdraw anytime, for any reason

✔ Contribution room comes back the next year

✔ No repayment required

Limits

-

Annual limit: ~$7,000 (2025)

-

Lifetime room accumulates

Best use case

Emergency fund + down payment flexibility

Bridge gaps between FHSA/RRSP strategies

FHSA: The Ultimate First-Time Buyer Account

This is the most powerful tool right now.

How it works

-

Contributions are tax deductible (like RRSP)

-

Withdrawals are tax-free (like TFSA)

Limits

-

$8,000/year

-

$40,000 lifetime

Key benefits

✔ No repayment required

✔ Tax deduction on contributions

✔ Tax-free withdrawal for home purchase

Your chart nailed it:

✔ “Best of both worlds” (RRSP + TFSA)

How These Accounts Work Together (The Real Strategy)

Here’s where things get interesting—and where most buyers miss opportunity.

The “Stacked Down Payment” Strategy

You can combine:

-

FHSA: $40,000 (tax-free, no repayment)

-

RRSP (HBP): $60,000 (must repay)

Total = $100,000 per person

Couples = $200,000+ potential down payment

Transferring Between Accounts (Critical Planning Tool)

1. RRSP ➜ FHSA (Allowed + Strategic)

-

You can transfer RRSP funds into FHSA

-

No immediate tax consequence

-

Does NOT restore RRSP room

Strategy:

-

Move RRSP funds → FHSA

-

Convert “repayable” money → non-repayable tax-free money

2. FHSA ➜ RRSP (If You Don’t Buy a Home)

-

Fully allowed, tax-deferred rollover

-

No impact on RRSP contribution room

Safety net: no downside to opening FHSA early

3. FHSA ➜ TFSA (Not Efficient)

-

Treated as:

-

Taxable withdrawal

-

New TFSA contribution

-

Avoid this move unless necessary

4. TFSA ➜ RRSP or FHSA

-

Allowed, but:

-

No tax advantage on transfer itself

-

Only useful if creating deduction room

-

Which Account Should You Use First? (Simple Priority Order)

1. FHSA (Always first)

-

Tax deduction + tax-free withdrawal

-

No repayment

2. RRSP (If income is high)

-

Use if:

-

You’re in a high tax bracket

-

You want refund to boost savings

-

3. TFSA

-

Use for:

-

Flexibility

-

Overflow savings

-

Short-term timelines

-

Example: Smart Calgary Buyer Strategy

Let’s say a buyer earns $110,000:

-

Max FHSA → $8,000/year

-

Contribute to RRSP → get ~$3,000 tax refund

-

Put refund into TFSA

-

Repeat annually

Result:

-

Tax refunds accelerate savings

-

FHSA builds tax-free down payment

-

RRSP adds leverage via HBP

Common Mistakes to Avoid

❌ Using RRSP before FHSA

❌ Not planning RRSP repayment impact

❌ Ignoring contribution room strategy

❌ Missing transfer opportunities

Bottom Line

-

FHSA = best account (no debate)

-

RRSP = powerful but comes with repayment

-

TFSA = flexibility tool

The real advantage comes from using all three together strategically

FAQ

How much can I take from my RRSP for a down payment?

Up to $60,000 per person under the Home Buyers’ Plan.

Can I use RRSP and FHSA together?

Yes—you can use both for the same home purchase.

Do I have to repay FHSA withdrawals?

No—FHSA withdrawals are tax-free and do not require repayment if used for a qualifying home.

What’s the best account for first-time buyers?

The FHSA, because it combines RRSP tax deductions with TFSA tax-free withdrawals.

Rental Property Mortgage Renewal Alberta: Insured vs Insurable Rates Explained

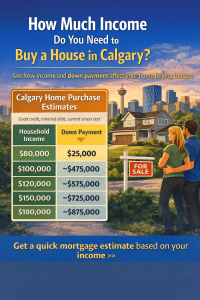

What Income Do You Need to Buy a House in Calgary? Real Examples

How Much Income Do You Need to Buy a House in Calgary?

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

One of the first questions many home buyers ask is:

“How much income do I need to buy a house in Calgary?”

Quick Answer (Snippet Call-Out)

In Calgary, a household earning about $100,000 per year can typically afford a home between $450,000 and $500,000, assuming a 5–10% down payment, good credit, minimal debt, and current Canadian mortgage stress test rules.

The exact number depends on several factors including your down payment, existing debts, and the mortgage rate used in the stress test.

Below are realistic examples based on typical Calgary home buying scenarios.

Example chart showing estimated home prices in Calgary based on household income and typical mortgage approval guidelines.

Example: Income vs Home Price in Calgary

These examples assume:

-

Good credit

-

Minimal debt

-

25-year amortization

-

Current Canadian mortgage stress test rules

-

Average Calgary property taxes

| Household Income | Down Payment | Estimated Purchase Price |

|---|---|---|

| $80,000 | $25,000 | ~$400,000 |

| $100,000 | $30,000 | ~$475,000 |

| $120,000 | $40,000 | ~$575,000 |

| $150,000 | $60,000 | ~$725,000 |

| $180,000 | $80,000 | ~$875,000 |

Calgary remains one of the more affordable major cities in Canada, which is why many first-time buyers are surprised by how much home they may qualify for.

How Mortgage Lenders Calculate Affordability in Canada

Canadian lenders use two main ratios to determine mortgage affordability.

Gross Debt Service (GDS)

Gross Debt Service measures the percentage of your income that goes toward housing costs.

Housing costs include:

-

mortgage payment

-

property taxes

-

heating costs

-

condo fees (if applicable)

Most lenders require GDS to stay below 39% of gross income.

Total Debt Service (TDS)

Total Debt Service includes all other monthly debts such as:

-

car loans

-

student loans

-

credit cards

-

lines of credit

Most lenders require TDS below 44% of income.

If your debts are higher, your mortgage approval amount may decrease.

The Mortgage Stress Test Explained

All insured mortgages in Canada must pass the mortgage stress test.

This means buyers must qualify at:

-

the contract mortgage rate or

-

the government qualifying rate

whichever is higher.

The stress test ensures borrowers can still afford payments if interest rates rise.

How Your Down Payment Changes Your Buying Power

Your down payment affects both your approval amount and whether mortgage insurance is required.

Minimum down payment rules in Canada:

-

5% on the first $500,000

-

10% on the portion between $500,000 and $999,999

-

20% for homes $1 million or higher

Many Calgary first-time buyers purchase homes using 5% down payment programs.

How Debt Affects Mortgage Approval

Existing debt can significantly reduce borrowing power.

Example:

| Monthly Debt | Approximate Mortgage Reduction |

|---|---|

| $300 car payment | ~$60,000 less borrowing power |

| $600 debt payments | ~$120,000 less borrowing power |

Paying down consumer debt before applying for a mortgage can dramatically increase your approval amount.

Calgary First-Time Buyers Often Qualify Sooner Than Expected

Many buyers assume they need a very high income before purchasing their first home.

However, programs such as:

-

insured mortgages

-

5% down payments

-

extended amortizations

allow buyers to enter the Calgary housing market earlier than they expect.

Calgary Mortgage FAQ

What salary do you need to buy a house in Calgary?

Most buyers need a household income between $90,000 and $120,000 to comfortably afford homes priced between $450,000 and $600,000, depending on their down payment and debt levels.

Can I buy a house in Calgary with $80k income?

Yes. Buyers earning around $80,000 per year may qualify for homes around $375,000 to $425,000, assuming minimal debt and a typical down payment.

How much mortgage can I qualify for in Calgary?

Most lenders allow housing costs up to 39% of gross income and total debts up to 44% of income, subject to the mortgage stress test.

Get a Personalized Mortgage Estimate

Online examples are helpful, but every mortgage approval depends on:

-

income structure

-

employment history

-

credit score

-

debt levels

-

down payment

If you want a personalized estimate of how much house you could afford in Calgary, feel free to reach out.

I’m happy to review your situation and give you a realistic price range before you start house hunting.

Author

Mark Herman, MBA

Mortgage Broker – 22 Years of Experience

Mark helps Calgary home buyers navigate mortgage approvals, complex income situations, and lender options. His goal is to help clients secure the right mortgage strategy before they start shopping for a home.

Approved: Mortgage with U.S. Income, Remote Work & Gifted Down Payment (CMHC Deal)

Cross-Border Mortgage Approved: U.S. Income + Gift Funds + CMHC

This Mortgage Deal Looked Impossible (But CMHC Approved It Anyway)

We recently completed a mortgage deal that even I assumed is impossible.

We got it done — and now that we’ve successfully navigated the process, we’re ready to help more buyers in similar situations.

This file was a great example of how the right strategy, documentation, and lender experience can turn a complicated deal into a clean approval.

Mortgage Mark Herman, Best Alberta, Canada mortgage broker for Americans buying in Canada.

The Buyers

This purchase involved two applicants:

-

Buyer #1: Canadian citizen, stay-at-home mom, currently with no income

-

Buyer #2: Permanent resident (PR), employed as a lawyer for a U.S. company, paid in U.S. dollars

Files like this can get tricky quickly, especially when one borrower has no income and the other is employed outside of Canada.

The Property

This was a primary residence purchase.

The buyers also had no other properties, which helped strengthen the application and simplify insurer review.

The Biggest Challenge: U.S. Income + Remote Work

The income-earning borrower worked for an American employer and was able to work 100% remotely.

The key detail? Their employment letter confirmed remote work was permanent, not temporary.

The documentation included:

-

Employment letter confirming permanent remote work status

-

U.S. income documents (W-2 and 1040)

-

A clear written narrative summarizing income and filing history

When borrowers are paid in U.S. dollars, lenders and insurers need to clearly understand consistency, deductions, and income stability. Presentation matters.

Down Payment Structure

The buyers had a 15% down payment, structured as follows:

-

5% from their own funds

-

10% gifted from a family member in the United States

Gifted down payments are common, but cross-border gifted funds require extra documentation and clean sourcing. We made sure everything was properly verified and acceptable for insurer guidelines.

CMHC Approval (Including an American Credit Report)

This mortgage was approved through CMHC, and one of the most interesting parts of the deal was that CMHC accepted an American Equifax credit bureau report.

That’s something many buyers don’t realize is even possible — but in the right scenario, it can absolutely work.

Why This Deal Was Unique

This was not a typical mortgage approval.

It required:

-

Cross-border income verification

-

Review of U.S. tax documents

-

Confirmation of permanent remote employment

-

Gifted down payment verification from the U.S.

-

Credit review using an American credit bureau report

-

Proper structuring and presentation for insurer underwriting

But in the end, the deal was approved — and the buyers are now homeowners.

The Takeaway

If you’re a Canadian citizen or PR earning U.S. income, working remotely, or receiving gifted funds from outside Canada, you may still qualify for a mortgage — even if your situation feels complicated.

A bank “no” doesn’t always mean the deal is dead. It often just means it needs the right approach.

Need Help With a Complex Mortgage File?

If you’re buying in Canada but your income, credit, or down payment involves the U.S., I can help you structure it properly from the start.

Mark(at)MaMaRv.ca

Or call/text directly to discuss your options.

Buying a Home with a Basement Suite – Some Details

Buying a home with a basement suite can be a powerful way to increase affordability, improve cash flow, and build long-term wealth — but not all suites (or lenders) are treated the same. If you’re considering a home with a suite, here are four important things to think about before you buy.

1) The type of suite matters.

If a suite is legal (fully permitted and meets municipal bylaws), all lenders will accept the rental income for qualification. If it’s not legal, make sure it’s at least fully self-contained, meaning it has its own entrance, its own kitchen, and its own bathroom. Many lenders will still consider rental income from these types of suites, but not all.

2) Your lender choice can change how much you qualify for.

Different lenders treat rental income very differently. Some will only allow 50% of the rental income to be used, while others allow up to 100%. Some lenders make you debt-service property taxes and heat, while others do not. These differences can have a huge impact on your approval amount, which is why working with a broker who understands rental income policy is so important.

3) Whether the suite is already rented or not DOES matter.

If the suite is currently rented, you should obtain a copy of the lease, make sure the purchase contract clearly states that the tenant is staying, and ensure the monthly rent amount is documented. If the suite is not already rented when you purchase the home, lenders will typically require an appraisal to confirm market rent. It’s very important to be conservative about what you expect the suite to rent for — especially if that rental income is crucial to comfortably affording the home.

What about adding a basement suite OR Mother-in-Law suite to the home I am buying?

Great idea, adding a suite to the home that you are buying AND at the same time, using the expected rental income from that same suite to qualify for the mortgage IS possible. There are a few lenders that allow this to happen and we do deals like this all the time. (No shortcuts though, as the final step is a final inspection and also providing the lender a copy of the occupancy permit from the City before the funds can be released.

Obviously there are some details involved but adding a suite and using the expected rental income to qualify for the mortgage is a huge helper for buyers looking to push a bit higher and get a “mortgage helper.”

Mortgage Mark Herman, 1st time home buying mortgage specialist

Summary: RE/MAX Canada Fall 2025 Housing Market Outlook

“54% of Canadians believe this fall is a good time to strike a deal on a home.”

Here’s a summary of the RE/MAX Canada Fall 2025 Housing Market Outlook piece, released Sept 21st:

- Pricing Trends: Residential price trends varied regionally, rising across Atlantic Canada and the Prairies, while declining in major urban centres in Ontario and British Columbia.

- National average home prices are expected to decrease by about 6.5% this fall.

- 68% of Canadians say a five- to 10-per-cent drop in property prices would make a meaningful difference in their ability to enter the market.

- Sales Activity: Home sales declined year-over-year in 62% of markets analyzed between January 1 and July 31, 2025.

- Buyer Optimism:

- 38.2% of housing markets are sitting firmly in buyer’s territory this Fall.

- 7% of Canadians say they intend to buy their first home within the next 12 months.

- 28% of Canadians planning to buy their first home in the next 12 months say they have saved at least 20 per cent for their down payment.

- 64% of Canadians say they’d feel ready if interest rates fell by 0.5 to one per cent.

- Seller Market:

- 26.4% of housing markets are expected to favour sellers this Fall.

- 8% of Canadians say they plan to sell their home in the next year, and among them, confidence is strong.

- 63% of those planning to sell believe they’ll be able to secure their asking price.

- Homeowner Sentiments:

- 92% of Canadian homeowners see their homes as a solid long-term investment.

Click here to read the full report!

Now is the perfect time to buy a home in Alberta as it is a solid BUYERS MARKET!

Mortgage Mark Herman, best first time home buying mortgage broker in Calgary Alberta

Or call me for a chat at your convenience.

Mortgage Mark Herman

GST Rebate for 1st Time Home Buyers

We have had lots of questions about this proram.

The legislation has been tabled, but is not done yet. As of today, and it is for contracts written May 27, 2025 or later.

Updates as they come in.

We have a 4-plex buyer who is purchasing a newly constructed 4-plex in Calgary at $1,250,000. His rebate is about 60k – now that is now pretty substantial!

Mortgage Mark Herman, 1st time buyer and move up mortgage specialist in Calgary Alberta.

Completed 2% of all FTHBI mortgages in YYC

Are you looking for a Mortgage Broker who specializes in the FTHBI in Calgary? That would be us!

We have completed 6 of these deals in 2019. There was as total of 260. So that puts us at completing 2.5% of the entire Calgary market for this program. Interesting!

Obviously, we love this program for these 2 reasons:

- You save between $100 and $200 per month on the mortgage payments. For sure. From Day 1.

- The point of the program is to lower your mortgage payments. When the government puts 5% down for you, it lowers the total balance outstanding and this lowers the payments.

- You save about $4000 in the CMHC fees.

- You put down 5%, and the government matches 5% on existing homes. That means your CMHC fee is based on 10% down and not 5% down, and you save that from Day 1 as well.

The down side

The down side is this is registered as an interest free loan from the government. You still pay them back 5% of the sale price when you sell. That is 5% of whatever the sale price is so it could be more or less, but it is still 5%.

“The down side is not a big deal!

Guaranteed lower mortgage payments and lower CMHC fee! This is a win!”

Mortgage Mark Herman, Top Calgary Mortgage Broker near me.

FREE RESEARCH Data on the First Time Home Buyer Incentive from Mortgage Mark Herman.

- Call us for all the data you need on this program.

- We have it all and can explain it to you -it is a long, boring read.

Here is the link to the full article, pasted below https://www.canadianmortgagetrends.com/2020/02/cmhcs-first-time-home-buyer-incentive-off-slow-start/

Four months after its official launh, CMHC’s First-Time Home Buyer Incentive had funded just 4% of its three-year goal, according to new data provided by the agency.

From the time the down payment assistance program launched on Sept. 2 to Dec. 9, CMHC received just 3,252 applications from across Canada, 2,730 of which were approved. That translated into total funding of $51.3 million—well off pace of the agency’s three-year target of $1.25 billion.

Under the program, the government will provide first-time buyers with an interest-free down payment loan of up to 5% for resale purchases, and 10% if the property is a new build. The CMHC then participates in any rise or fall in value of the home, and the loan must be repaid either when the house is sold or within 25 years.

Interest in the program was highest in Quebec, where 1,300 applications were received. Comparatively, just 436 Ontarians applied, according to statistics that were tabled in Parliament last week.

Here’s a look at the breakdown of applications from some of the major housing markets across Canada:

- Greater Toronto Area: 148

- Vancouver: 45

- Edmonton: 447

- Calgary: 260

- Winnipeg: 144

- Montreal 654

- Halifax: 64

- New Brunswick: 60

- PEI: 12

CMHC head Evan Siddall defended the results via Twitter on Friday:

“In addition to CMHC’s challenges in estimating demand for the FTHBI, uneven lender support is a complicating factor,” he tweeted on Friday. “It may also be evidence that there is less unsatisfied FTHBI demand due to the stress test than people claim. People can always buy less expensive homes.

Why is the FTHBI Unpopular?

Since the initiative was first announced in the Liberals’ spring budget, many in the industry have criticized it for being overly complicated and promising negligible benefits.

One of the biggest restrictions of the program is that it’s currently limited to purchases of up to $565,000. In markets like Toronto and Vancouver, buyers can be hard-pressed to find available properties under that threshold. According to recent data from the Toronto Real Estate Board, the average sale price in December was $837,788.

Many buyers have also expressed unease at the thought of giving up equity in their home, particularly with prices rising rapidly in many markets across the country.

While Prime Minister Justin Trudeau promised tweaks to the FTHBI during last year’s federal election, no additional updates have since been provided. The proposed changes would increase the maximum purchase price eligible under the program to $789,000 for buyers in Toronto, Vancouver and Victoria.

It remains to be seen whether the FTHBI’s slow start is a harbinger of future demand over the coming years, or whether first-time buyers will grow more receptive to sharing a chunk of their home equity with the government.

UPDATE: NHBI Canada

Here is an UPDATE to the Canadian New First Time Home Buyer Incentive Program

A Calgary lawyer recently had an opportunity to review the program and attend a basic seminar. He said he would not recommend the “down payment equity share” program to a first time home buyer for the following reasons – BUT here are our replies … and the Program DOES make sense to do.

NEGATIVE POINTS and the reasons FOR the program are below:

- It will take much longer to be approved for this program than for a normal mortgage loan and sellers may not accommodate the longer condition time.

- We normally pre-approve buyers with these files and this program in advance so there is no extra time needed at the lenders for conditions.

- The math for this program is complicated and buyers that use this program need to be pre-approved as they need the mortgage to match the affordability guidelines and to shop in the right price range.

- The extra time is at closing when 2 sets of documents are needed by the lawyer. As long as this is known in advance, the closing date can be long enough to allow for the extra paperwork to be requested and completed.

- Higher legal and appraisal costs will result as two separate mortgages have to be prepared and registered (one for the lender and one for the equity share) and an extra appraisal will have to be obtained and paid for by the owner if paying out the incentive mortgage prior to the ultimate sale of the property.

- A 1st and 2nd mortgages go on title at the same time as closing.

- Appraisal on purchase is not involved as it has to be a CMHC approved mortgage (CMHC is responsible for the appraisal in this case) and the program is based on the purchase price.

- If the owner wants to pay it off / back sooner, then an appraisal is needed at buyer cost ~$350.

- This would happen if the owner wanted to do extensive renovations to the home.

- An appraisal should not be needed on a bonafide sale, to a 3rd party, via a realtor, and when listed on MLS.

- An appraisal MAY be needed – as the owners cost – if the sale if it is a “private sale” and/ or believed to be below market value.

- (This is to stop the owner from selling the home to a family member for $1.00 and then attempt to repay the loan with $0.05.)

- The buyer has already saved many times the extra costs, savings are about $100 – $150/ month, from day 1. Paying-out at 10, 15, 20 years later … they have already saved $100 x 12 x 10 years = $12,000, in the bank, already.

- A disincentive to improve/renovate the property will exist as any appreciated value is shared with the government notwithstanding that they don’t contribute to the renovation costs.

- True.

- Upon repayment, improvements will be included when determining the market value, therefore the Homebuyer will have to consider the cost and benefit of the planned renovations, and decide whether to repay the Incentive prior to making any home improvements.

- IMPORTANT: It may be beneficial to the Homebuyer to repay the Incentive prior to conducting any major renovations to the home.

- A potential trap is being created for non-permanent residents who are legally authorized to work in Canada who can qualify to buy under this program but will have extreme difficulty in selling when their work permit expires as they will not have sufficient equity to satisfy the required withholding requirements under the Income Tax Act

- We have been the largest Mortgage Alliance brokerage in Canada for 6 years in a row, and we do about 20 deals a year for 9xx SIN buyers; 99% of our customers are unaffected by this.

- Again, this program is surgical in for who it works for. The program is not for everyone.

- It may be more difficult to refinance the property (it is not clear whether the Government will permit refinancing of the first mortgage and postpone their security to the new financing)

Updated rules have been released:

- The home CAN be refinanced without triggering repayment of the incentive, however, the shared equity mortgage will only be postponed to the outstanding balance that would otherwise be owing under the first ranking mortgage (i.e. no equity take-out will be permitted ahead of the shared equity mortgage).

Note:

- The combination of all charges on a refinance must not exceed 80%.

- This program DOES allow Assumption of the mortgage. Standard rules apply: full requalification by the parties assuming the mortgage directly with the lender. The standard on-going ramifications to the seller still apply.

- This program does NOT allow a PORT of the mortgage to another property. It would have to be paid out at that time.

- If refinancing of the first mortgage will not be possible without paying out the government’s equity share, then the first mortgage lender will have a captive borrower. The lender will have no incentive to reduce posted mortgage rates on renewal resulting in substantially higher interest rates in the second and subsequent mortgage terms for the homeowner.

- As above, the rules do allow the home to be refinanced without triggering repayment of the incentive.

- The renewal rate offered by the lender is independent of the 2nd charge on title.

Side note: We see that lenders are already applying the “Stress Test” under-the-covers on renewals when calculating the renewal rates. More on my blog here: http://markherman.ca/2019/06/

We love this New Home Buyer Incentive Program – NHBI

Mortgage Mark Herman; Best, Top Calgary Mortgage Broker

Details of the FTHBI – First Time Home Buyer Incentive

The First-Time Home Buyer Incentive (FTHBI) officially starts on September 2, 2019. Introduced help first-time home buyers, the FTHBI will provide shared equity loans of 5% toward the down payment of a resale home, and 5% or 10% for newly-built homes.

The idea is that by boosting the size of buyers’ down payments, the FTHBI lowers the monthly mortgage payment and is some relief on the costs of home ownership.

Details of Qualification

To qualify for the FTHBI, home buyers must satisfy the following:

- At least one person in the household must be a first-time home buyer, meaning they have not owned a home, or dwelled in a home owned by their spouse, over the last four years. (An exception is made for buyers who’ve had a breakdown of marriage or common-law relationship.)

- Buyers must have a minimum of 5% down payment from “own resources” to qualify for a CMHC insured mortgage.

- Buyers’ combined household income cannot exceed $120,000. This includes the income of any guarantors co-signing on the mortgage, as well as any rental income generated if part of the home is tenanted out.

- The buyers’ Mortgage-to-Income Ratio (MTI) cannot exceed 4x their income, including the portion that’s provided by the FTHBI. This means the maximum down payment for a resale home cannot exceed 14.99%, and 9.99% for a new build.

Details of How It Works

The funds provided are registered as a second mortgage on title, and don’t incur interest.

This second mortgage must be paid back in full when the first insured mortgage matures at 25 years or when the home is sold, whichever comes first. Homeowners may pay it back as a lump sum early without penalty. (Details of how the value at the time of payout are yet to be released.)

Because it is a shared equity mortgage, the amount to be paid back fluctuates along with the value of the home over time: if the home’s assessed value rises, the loan repayment will increase by the same percent. However, the same will occur if the home has lost value by the time it is sold or the mortgage matures.

There are more details on the last post on savings including this chart below: http://markherman.ca/updates-to-cmhc-first-time-buyer-incentive-program/

Savings Over Time

This is a handy chart to see the savings on the monthly payment when using the program.

OVERALL

The program looks to be a helper for saving on payments and that is a great thing.

Mark Herman, Top& Best Calgary Mortgage Broker