Minimum Down Payment Canada: Rules, Examples & Options, 2026 Guide for Home Buyers

written by Mortgage Mark Herman; MBA with 22 years as a top mortgage broker

Minimum Down Payment in Canada: What Home Buyers Need to Know

One of the first questions people ask when they start thinking about buying a home is:

What is the minimum down payment in Canada?

The answer depends on the price of the home and how the mortgage is structured.

Understanding the rules early can help you figure out how much you need to save and what you qualify for.

Let’s walk through the basics.

Minimum Down Payment Rules in Calgary, and all of Canada

In Canada, the minimum down payment depends on the purchase price of the home.

Current rules are:

-

5% down on the first $500,000

-

10% down on the portion between $500,000 and $999,999

-

20% down for homes $1,000,000 or more

For example:

If you buy a $600,000 home, the minimum down payment would be:

-

5% on the first $500,000 = $25,000

-

10% on the remaining $100,000 = $10,000

Total minimum down payment = $35,000

High-Ratio vs Conventional Mortgages

Your down payment also determines the type of mortgage you qualify for.

High-Ratio Mortgage (5% – 19% Down)

If your down payment is less than 20%, your mortgage is considered a high-ratio mortgage.

This means the mortgage is more than 80% of the home’s value, so lenders require mortgage default insurance through providers like:

-

CMHC

-

Sagen

-

Canada Guaranty

The insurance premium is added to your mortgage amount and paid over time.

The upside? High-ratio mortgages often qualify for lower interest rates.

Conventional Mortgage (20% Down or More)

If you put 20% down or more, the mortgage is considered conventional.

This means:

-

No mortgage insurance required

-

Lower borrowing costs overall

-

More flexibility with lenders

Down Payment Requirements for Calgary Buyers

The minimum down payment rules in Canada apply nationwide, including here in Calgary.

However, many Calgary buyers are surprised to learn how little down payment they actually need. For example, a $500,000 home in Calgary could require as little as $25,000 down, which is often less than people expect.

If you’re buying in Calgary or Alberta and want to see what your numbers look like, it’s worth running the calculations early so you know your options.

Where Your Down Payment Can Come From

Lenders also need to verify where the down payment funds come from.

Here are the most common sources.

Savings or Investments

If your down payment is coming from:

-

savings

-

chequing accounts

-

investments

Lenders will require 90 days of account history.

This verifies that the funds belong to you and were not recently borrowed.

Your statements must clearly show:

-

your name

-

the account number

-

the transaction history

Gifted Down Payment in Canada

A gift from family is one of the most common ways buyers fund their down payment.

The gift can come from a family member not only in Canada but from almost anywhere in the world. It does need to be transferred into any Canadian financial institution to be used though.

However, lenders require confirmation that the gift does not need to be repaid.

This is done with a gift letter signed by both parties confirming it is a non-repayable gift.

The gift must come from a direct family member; mother, father, brother, sister, grandparent, legal guardian.

Using RRSPs for Your Down Payment

Canada has a program called the Home Buyers’ Plan (HBP).

It allows first-time buyers to withdraw up to $35,000 from their RRSP tax-free for a down payment.

Key details:

-

You have 15 years to repay it

-

Repayment starts two years after withdrawal

-

If you don’t repay it, the amount becomes taxable income

To verify RRSP funds, lenders will need:

-

the RRSP withdrawal form

-

your RRSP statement

Using RRSPs if You’re Not a First-Time Buyer

You can still withdraw RRSP funds even if you’re not a first-time buyer, but it will be taxed as income.

The financial institution usually withholds about 30% for taxes.

This isn’t always ideal, but it can still work depending on the situation.

Borrowing Against Another Property

If you already own property, you may be able to use the equity in that property for your down payment.

This can be done through:

-

a refinance

-

a home equity line of credit (HELOC)

We just need to verify the available equity through your current mortgage statements.

Down Payment From the Sale of Your Current Home

Many buyers use equity from selling their existing home as their down payment.

In that case lenders require:

-

the firm sale contract

-

your current mortgage statement

-

confirmation of the sale proceeds

If your purchase closes before your sale, bridge financing can cover the gap.

This is a very common situation and usually easy to arrange.

Borrowing Your Down Payment

Some borrowers with strong income can qualify to borrow their down payment from an unsecured line of credit.

This strategy isn’t right for everyone, but it can work if your income supports the additional debt.

With rents rising and many buyers trying to enter the market, some people choose this route instead of continuing to rent.

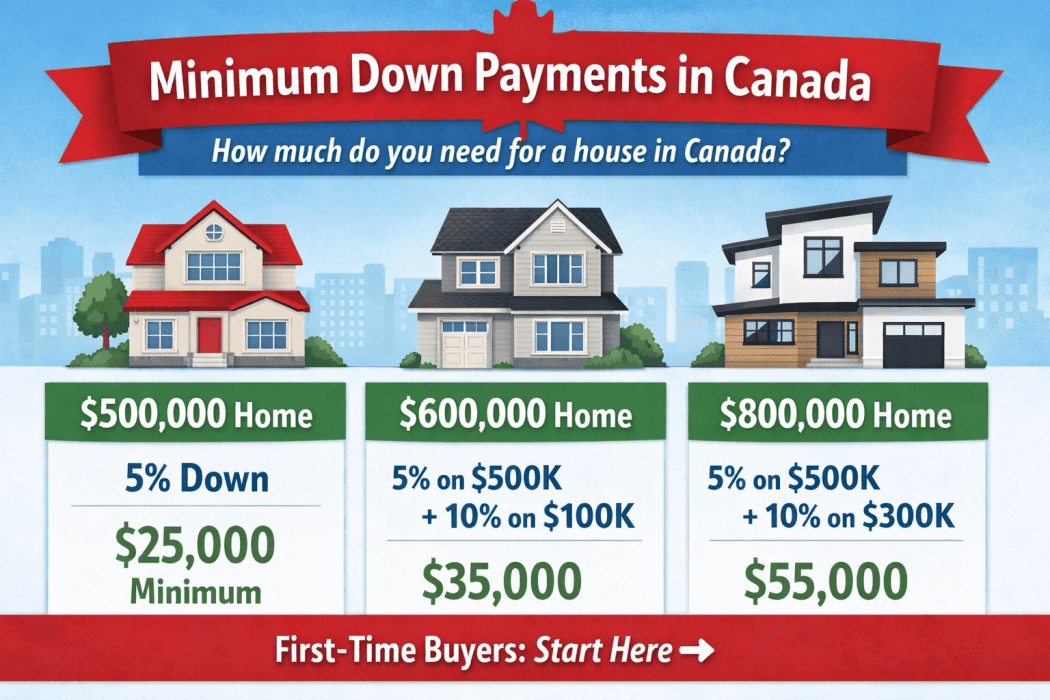

Down Payment Examples in Canada

Here are some quick examples of minimum down payments based on purchase price:

$500,000 home

Minimum down payment:

5% = $25,000

$600,000 home

5% on first $500,000 = $25,000

10% on remaining $100,000 = $10,000

Minimum down payment = $35,000

$800,000 home

5% on first $500,000 = $25,000

10% on remaining $300,000 = $30,000

Minimum down payment = $55,000

FAQ: Down Payment Questions in Canada

What is the minimum down payment for a house in Canada?

The minimum down payment is 5% for homes under $500,000, with additional requirements for higher price ranges.

Can my down payment be a gift?

Yes. Many buyers use gifted down payments from family, but lenders require a signed gift letter confirming it is not repayable. Each bank has it’s own template so don’t try to do one yourself, we will send it to you to fill in and e-sign.

Can I borrow my down payment?

In some cases, yes. Borrowers with strong income may qualify to borrow their down payment from a line of credit.

Can I use my RRSP for a down payment?

Yes. The Home Buyers’ Plan allows withdrawals of up to $60,000 tax-free, with 15 years to repay the funds.

Final Thoughts

There are many ways to structure a down payment, and the right strategy depends on your finances and long-term plans.

If you’re thinking about buying, it’s worth running the numbers early so you know exactly what you qualify for and how much you need to save.

If you want help figuring out your options, you can start here:

https://markherman.ca/contact

About the Author

Mark Herman is a mortgage broker with 22 years of experience helping Canadians finance their homes. He holds an MBA in Finance and specializes in structuring mortgages for first-time buyers, self-employed borrowers, and real estate investors. He can be reached at 403-681-4376.