Fixed vs Variable Mortgage Calgary 2026 | Should You Lock In Now?

Fixed vs Variable Mortgage in Calgary (2026): Why Locking In May Be the Safer Move Right Now

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

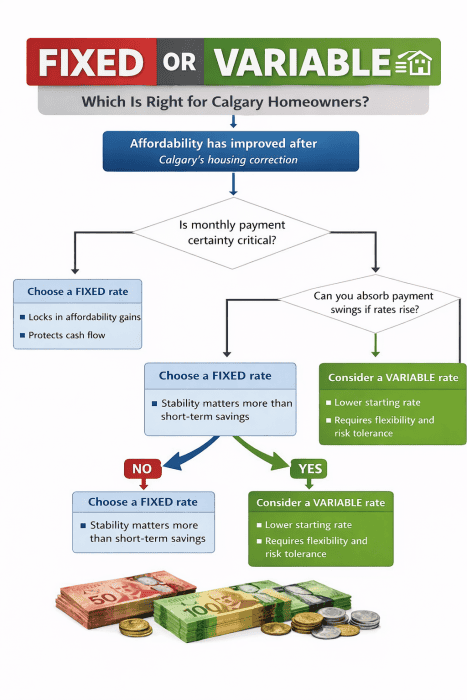

Mortgage rates in Canada—and specifically here in Calgary—are starting to trend upward again. After a period where variable rates often came out ahead, the risk equation has shifted.

If you’re trying to decide between a fixed or variable mortgage today, the key question is no longer just “which is cheaper right now?” — it’s how much risk are you willing to take on?

What’s Changed: Rates Are Gradually Rising Again

Over the past year, many buyers benefited from improving affordability after the housing correction. But now:

-

Bond yields are creeping higher

-

Lenders are adjusting fixed rates upward

-

Variable rates remain exposed to future increases

This creates a very different environment than what borrowers faced even 6–12 months ago.

The Real Question: Certainty vs Flexibility

Your decision tree graphic captures this perfectly.

At its core, the choice comes down to one key question:

Is monthly payment certainty critical to you?

If the answer is yes, a fixed rate is usually the better fit.

If the answer is no, then you need to ask:

Can you comfortably absorb payment increases if rates rise further?

Right now, that second question matters more than ever.

Why Fixed Rates Are Becoming More Attractive in Calgary

Here’s what I’m seeing with clients in Calgary right now:

1. Cash Flow Is Getting Tighter

With higher home prices and cost of living, many borrowers don’t have as much room to absorb rising payments.

A fixed rate:

-

Locks in your payment

-

Protects your monthly budget

-

Eliminates uncertainty

2. The Risk of Being Wrong Has Increased

Variable rates can still win—but only if rates stabilize or fall.

If rates continue rising:

-

Payments can increase significantly

-

Stress levels go up

-

Flexibility becomes a liability instead of an advantage

Right now, the downside risk is larger than the potential upside reward.

3. Fixed Rates Lock In Today’s Affordability

Even though fixed rates are slightly higher than they were, they still:

-

Lock in your current qualification

-

Protect your purchasing power

-

Remove future surprises

In a rising rate environment, that stability has real value.

When a Variable Rate Still Makes Sense

Variable isn’t “wrong”—it just requires a higher risk tolerance right now.

It may still be a fit if you:

-

Have strong cash flow and savings

-

Can handle payment increases without stress

-

Believe rates will stabilize or decline in the near future

But this is no longer the “default smart choice” it once was.

Calgary-Specific Insight: Why This Matters More Locally

In Calgary, many buyers are:

-

Stretching slightly more on affordability

-

Entering the market after sitting out during higher rates

-

Managing variable income (commission, bonuses, self-employed)

That makes payment stability more valuable here than in lower-cost markets.

Simple Rule of Thumb (2026)

-

Want stability and peace of mind → Choose fixed

-

Comfortable with risk and volatility → Consider variable

But today, more borrowers are landing on fixed—not because it’s exciting, but because it’s safer.

FAQ: Fixed vs Variable Mortgages in Calgary

Is it better to go fixed or variable in 2026?

Right now, fixed rates are generally the safer option due to rising interest rate risk.

Will variable rates come down?

They might—but timing is uncertain, and borrowers need to be able to handle increases in the meantime.

Can I switch later if I choose fixed?

Yes, but there may be penalties depending on your lender and timing.

Final Thoughts

This isn’t about predicting the market perfectly.

It’s about choosing a mortgage that lets you:

-

Sleep at night

-

Stay in control of your finances

-

Avoid unnecessary risk

Right now, for many Calgary homeowners, that points clearly toward locking in a fixed rate.

Need Help Deciding?

If you’re unsure which direction makes sense for your situation, I can walk you through the numbers and stress-test both options.

Author Bio

Mark Herman is a Calgary-based mortgage broker with 22 years of experience and an MBA in Finance. He helps homebuyers and investors make smarter mortgage decisions by focusing on strategy, risk management, and long-term financial outcomes.

Mortgage Penalty Calculator Canada: How Fixed-Rate Penalties Are Calculated (2026 Guide)

Written by Mark Herman; MBA in Finance – Mortgage Broker with 22 Years of Experience

Quick Answer: Mortgage Penalty in Canada

If you break a fixed-rate mortgage in Canada, your penalty is usually:

- 3 months’ interest, or

- Interest Rate Differential (IRD)

You pay whichever is higher.

Most fixed-rate penalties in 2026 fall between:

- $5,000 to $30,000+

The exact amount depends heavily on how your lender calculates IRD.

Mortgage Penalty Calculator (Quick Estimate)

Use this simple method to estimate your penalty:

Step 1: 3 Months’ Interest

Formula:

Mortgage balance × interest rate × 3 ÷ 12

Example:

- $400,000 mortgage

- 5.00% rate

Penalty ≈ $5,000

Step 2: Estimate IRD – Interest Rate Differential

Formula:

(Your rate − current comparable rate) × balance × remaining months ÷ 12

Example:

- Balance: $400,000

- Your rate: 5.00%

- Current rate: 3.50%

- 24 months remaining

IRD ≈ $12,000

Your real penalty = the higher of the two

What Is a Mortgage Penalty?

A mortgage penalty is a fee you pay if you break your mortgage early by:

- selling your home

- refinancing

- switching lenders

- paying off your mortgage before the term ends

Fixed-rate mortgages almost always have higher penalties than variable-rate mortgages.

Why Fixed Mortgage Penalties Are So High

1. IRD replaces simple interest

Variable mortgages:

- 3 months’ interest is the max payout penalty

Fixed mortgages:

- The GREATER of 3-months interest or the IRD calculation (which ever is higher)

2. Rate changes increase penalties

If rates drop after you lock in:

- Your rate = higher

- Current rate = lower

Bigger gap = bigger penalty.

The bank says they were making all that interest before and now that you pay them back they will lend the money out at a lower rate so they need to “re-capture the interest that they expected to get before.”

During Covid when Calgary home owners mortgage rates were about 4% and the rates dropped to 2%, the IRD payout penalties were in the range of $20,000 to $45,000 on 5-year fixed mortgages!! What?

3. Each bank uses a different formula

This is the most important point.

Two identical mortgages can have very different penalties depending on the lender.

How Banks Calculate Mortgage Penalties (Canada)

RBC

- Uses IRD based on:

- posted rate for similar term

- minus your original discount

More complex than a simple “current rate” comparison

TD

- Uses posted rate for similar term

- subtracts your original discount

Often results in higher penalties than expected

BMO

- Similar to TD and RBC

- Uses posted rates and discount adjustments

Scotiabank

- Uses posted rate for closest remaining term

- adjusted for your original discount

- includes present-value calculation

CIBC

- Uses a comparison mortgage method

- compares:

- your rate (plus discount)

- vs current posted rate

Can produce significantly higher penalties

National Bank

- Uses a standard rate / posted rate approach

- adds capped 1 month interest component

Different structure than other banks

Why This Matters (Real Calgary Examples)

Example 1: Move-Up Buyer in Calgary

- Bought in 2023

- Needs bigger home in 2026

- Mortgage: $520,000

- Fixed rate: 4.79%

- 3 years remaining

Penalty could be $15,000–$25,000

Example 2: Refinancing to Pay Off Debt

- Calgary condo owner

- Wants to consolidate debt

- Mortgage: $300,000

- Fixed rate: 5.19%

Penalty: $8,000–$12,000

Still worth it in some cases—but must be calculated properly

Example 3: Rental Property Sale

- Investor selling in Calgary

Difference between lenders:

- Bank A: $9,000 penalty

- Bank B: $14,000 penalty

Same borrower, different lender = big difference

Fixed vs Variable Mortgage Penalties

| Mortgage Type | Typical Penalty |

|---|---|

| Variable | 3 months interest |

| Fixed | IRD or 3 months (whichever is higher) |

Fixed penalties are often 2–5x higher

How to Reduce or Avoid a Mortgage Penalty

1. Use prepayment privileges

Most lenders allow:

- 15% lump sum annually

- 15% payment increases, and doubling the payment

2. Consider portability

You may be able to transfer your mortgage to a new property and not pay the penalty as you are not closing down your mortgage. You are porting it to another address.

3. Time your refinance

Waiting until renewal = no penalty

4. Choose the right lender upfront

This is the biggest factor.

Rate matters—but penalty structure matters more long-term

Internal Resources (Recommended Reading)

- Minimum Down Payment Canada: Rules, Examples & Options

- How Much Income Do You Need to Buy a House in Calgary

- Fixed vs Variable Mortgage Rates in Canada

- OnlyFans Mortgage in Canada

- Mortgage Renewals Guide

FAQ: Mortgage Penalties in Canada

How is a mortgage penalty calculated?

It is the greater of:

- 3 months’ interest

- IRD (interest rate differential)

Why are fixed mortgage penalties so high?

Because IRD estimates the lender’s lost interest over time—not just a simple fee.

Can two banks charge different penalties?

Yes—and the difference can be thousands of dollars.

Can I avoid a mortgage penalty?

Sometimes, by:

- porting your mortgage

- waiting until renewal

- restructuring your mortgage

Is there a standard penalty formula in Canada?

No. Each lender uses its own variation of IRD.

Bottom Line

Most borrowers focus on:

getting the lowest rate

But ignore:

how expensive it is to break the mortgage

In many cases:

The penalty matters more than the rate. Depending on your situation – like moving out of the country in 1 or 2 years.

If you’re planning to:

- refinance

- sell early

- restructure your mortgage

I can help you:

- estimate your real penalty

- compare lender formulas

- avoid costly mistakes

Reach out for a personalized strategy.

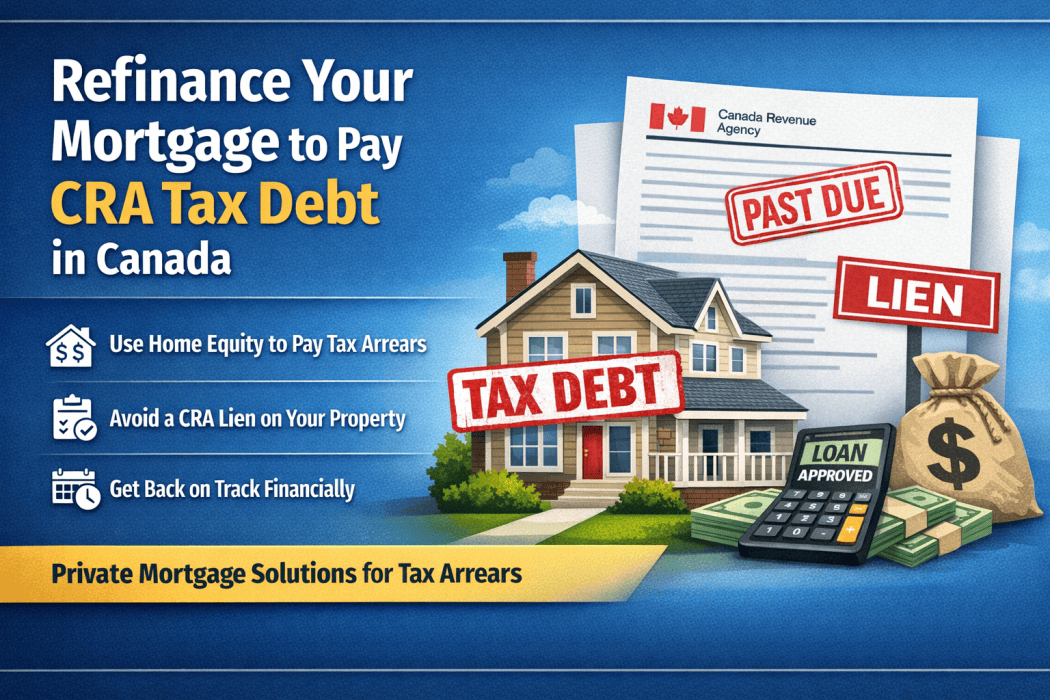

Can I Use a Mortgage to Pay CRA Tax Debt in Canada? (A Real Example of a Private Refinance)

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience specializing in new home buyers and tough deals.

Many Calgary and Canadian homeowners are surprised to learn that the CRA can place a lien on their home for unpaid taxes. Once that happens, refinancing becomes much harder.

The good news is that homeowners with equity often still have options. In many cases, a private mortgage refinance can be used to pay CRA tax debt, remove the lien risk, and give you time to get your finances back on track.

Below is a real example of how this works.

Real Example: Refinancing to Pay $29,000 in CRA Tax Debt

A self-employed homeowner recently contacted me about refinancing their mortgage to deal with back taxes owed to the Canada Revenue Agency (CRA).

Here was the situation:

Business tax situation

-

Business filings completed up to Oct 2022 – Sept 2023

-

Currently working with an accountant to file Oct 2023 – Sept 2024

-

Next filing period 2024–2025 still pending

-

GST paid up to end of 2024

-

GST may still be owing but amount unknown until filings are complete

Income structure

-

Owner pays themselves from the business when income comes in

-

No dividends issued

-

Most tax liability flows to personal taxes

Personal tax situation

-

Approximately $29,000 in personal tax debt to CRA

CRA had indicated they may place a lien on the property, which would make financing much more difficult.

The homeowner didn’t currently have the cash to pay the taxes, and they were also trying to pay their accountant to complete outstanding business filings.

Why CRA Debt Is a Problem for Mortgage Lenders

Most traditional lenders (banks and credit unions) require that CRA debt be fully paid before they approve a mortgage refinance.

They want to ensure:

-

There is no CRA lien registered

-

All tax filings are up to date

-

There are no outstanding collection issues

If these conditions are not met, the bank will usually decline the mortgage.

How a Private Mortgage Can Solve the Problem

In situations like this, a private lender refinance can be used to:

-

Pay off the CRA tax debt

-

Prevent or remove a CRA lien

-

Provide time to complete tax filings

-

Stabilize finances before returning to a traditional lender

Private lenders focus primarily on:

-

Equity in the property

-

Property value

-

Exit strategy (how the loan will be repaid or refinanced later)

They are often much more flexible when dealing with self-employed borrowers or tax arrears.

Typical Structure of a CRA Tax Debt Refinance

A refinance for tax debt usually works like this:

Step 1 – Property appraisal

The lender confirms the home’s value and available equity.

Step 2 – Mortgage approval

A private lender approves a mortgage based on the equity position.

Step 3 – CRA payout

Funds from the refinance are used to pay CRA directly.

Step 4 – Short-term mortgage

The homeowner keeps the private mortgage for 12–24 months while fixing their tax situation.

Why Acting Before a CRA Lien Matters

Timing is critical.

If CRA registers a tax lien on your property, refinancing becomes significantly more complicated because:

-

The lien must be paid during the refinance

-

Some lenders refuse to fund if the lien is already registered

-

Legal costs can increase

Getting financing before the lien is registered gives homeowners far more options.

Who This Strategy Works Best For

Using a private mortgage to pay CRA debt can work well if you:

-

Own a home with significant equity

-

Are self-employed

-

Have unfiled taxes that are being completed

-

Need time to catch up financially

This strategy is common for:

-

Business owners

-

Contractors

-

Real estate investors

-

Commission-based professionals

The Exit Plan: Moving Back to a Traditional Mortgage

Private mortgages are usually short-term solutions.

During the term, the goal is to:

-

Complete all tax filings

-

Pay CRA balances

-

Improve income documentation

-

Refinance into a lower-rate bank mortgage

Featured Snippet – Q&A Section

Frequently Asked Questions About CRA Tax Debt and Mortgages

Can you refinance your home to pay CRA tax debt in Canada?

Yes. Homeowners with sufficient equity can often refinance their mortgage to pay CRA tax debt. If traditional lenders will not approve the refinance, a private mortgage lender may still provide financing based on the home’s equity.

Can CRA put a lien on your house for unpaid taxes?

Yes. The Canada Revenue Agency can register a tax lien against your property if taxes remain unpaid. Once registered, the lien attaches to your home and must usually be paid before selling or refinancing.

How much equity do I need to refinance to pay tax debt?

Most private lenders will allow refinancing up to approximately 75–80% of the home’s value, depending on the situation and property location.

Will banks refinance if I owe CRA money?

Most banks require that CRA debts be paid first and tax filings be up to date. If taxes are still outstanding, homeowners often need to use a short-term private mortgage to pay CRA and then refinance with a bank later.

Mortgage Example Calculator Section

Example: Using a Mortgage Refinance to Pay CRA Tax Debt

Let’s look at a simplified example.

Home Value: $700,000

Current Mortgage: $420,000

Maximum Refinance at 80%: $560,000

Potential equity available:

$560,000 – $420,000 = $140,000 available

If the homeowner owes $29,000 in CRA taxes, they could refinance and:

-

Pay the CRA debt in full

-

Cover legal and appraisal costs

-

Possibly consolidate other high-interest debts

This type of refinance is commonly used as a temporary strategy, allowing the homeowner to clean up their tax situation before moving back to a traditional lender.

Frequently Asked Questions

Can CRA force the sale of my home?

Yes, in extreme cases CRA can pursue legal action that could eventually lead to the forced sale of property.

However, most homeowners resolve the issue by paying the tax debt through refinancing.

Can I get a mortgage if my taxes aren’t filed?

Traditional lenders usually require all tax filings to be current.

Private lenders may still consider the mortgage if:

-

You are actively working with an accountant

-

The property has enough equity.

How much equity do I need to refinance CRA debt?

Most private lenders require the mortgage to stay below about 75–80% of the home’s value, although this varies.

Final Thoughts

Tax debt with CRA is stressful, especially for self-employed homeowners. But if you own property with equity, a private mortgage refinance can provide a solution to clear the debt and buy time to get your finances organized.

The key is acting early — before CRA registers a lien on your home.

Author Bio

Mark Herman, MBA is a mortgage broker with 22 years of experience helping homeowners across Canada solve complex financing situations, including tax debt, private mortgages, and self-employed income challenges.

What Income Do You Need to Buy a House in Calgary? Real Examples

How Much Income Do You Need to Buy a House in Calgary?

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

One of the first questions many home buyers ask is:

“How much income do I need to buy a house in Calgary?”

Quick Answer (Snippet Call-Out)

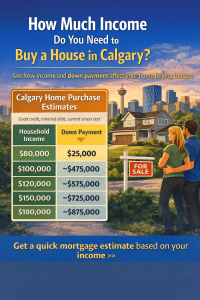

In Calgary, a household earning about $100,000 per year can typically afford a home between $450,000 and $500,000, assuming a 5–10% down payment, good credit, minimal debt, and current Canadian mortgage stress test rules.

The exact number depends on several factors including your down payment, existing debts, and the mortgage rate used in the stress test.

Below are realistic examples based on typical Calgary home buying scenarios.

Example chart showing estimated home prices in Calgary based on household income and typical mortgage approval guidelines.

Example: Income vs Home Price in Calgary

These examples assume:

-

Good credit

-

Minimal debt

-

25-year amortization

-

Current Canadian mortgage stress test rules

-

Average Calgary property taxes

| Household Income | Down Payment | Estimated Purchase Price |

|---|---|---|

| $80,000 | $25,000 | ~$400,000 |

| $100,000 | $30,000 | ~$475,000 |

| $120,000 | $40,000 | ~$575,000 |

| $150,000 | $60,000 | ~$725,000 |

| $180,000 | $80,000 | ~$875,000 |

Calgary remains one of the more affordable major cities in Canada, which is why many first-time buyers are surprised by how much home they may qualify for.

How Mortgage Lenders Calculate Affordability in Canada

Canadian lenders use two main ratios to determine mortgage affordability.

Gross Debt Service (GDS)

Gross Debt Service measures the percentage of your income that goes toward housing costs.

Housing costs include:

-

mortgage payment

-

property taxes

-

heating costs

-

condo fees (if applicable)

Most lenders require GDS to stay below 39% of gross income.

Total Debt Service (TDS)

Total Debt Service includes all other monthly debts such as:

-

car loans

-

student loans

-

credit cards

-

lines of credit

Most lenders require TDS below 44% of income.

If your debts are higher, your mortgage approval amount may decrease.

The Mortgage Stress Test Explained

All insured mortgages in Canada must pass the mortgage stress test.

This means buyers must qualify at:

-

the contract mortgage rate or

-

the government qualifying rate

whichever is higher.

The stress test ensures borrowers can still afford payments if interest rates rise.

How Your Down Payment Changes Your Buying Power

Your down payment affects both your approval amount and whether mortgage insurance is required.

Minimum down payment rules in Canada:

-

5% on the first $500,000

-

10% on the portion between $500,000 and $999,999

-

20% for homes $1 million or higher

Many Calgary first-time buyers purchase homes using 5% down payment programs.

How Debt Affects Mortgage Approval

Existing debt can significantly reduce borrowing power.

Example:

| Monthly Debt | Approximate Mortgage Reduction |

|---|---|

| $300 car payment | ~$60,000 less borrowing power |

| $600 debt payments | ~$120,000 less borrowing power |

Paying down consumer debt before applying for a mortgage can dramatically increase your approval amount.

Calgary First-Time Buyers Often Qualify Sooner Than Expected

Many buyers assume they need a very high income before purchasing their first home.

However, programs such as:

-

insured mortgages

-

5% down payments

-

extended amortizations

allow buyers to enter the Calgary housing market earlier than they expect.

Calgary Mortgage FAQ

What salary do you need to buy a house in Calgary?

Most buyers need a household income between $90,000 and $120,000 to comfortably afford homes priced between $450,000 and $600,000, depending on their down payment and debt levels.

Can I buy a house in Calgary with $80k income?

Yes. Buyers earning around $80,000 per year may qualify for homes around $375,000 to $425,000, assuming minimal debt and a typical down payment.

How much mortgage can I qualify for in Calgary?

Most lenders allow housing costs up to 39% of gross income and total debts up to 44% of income, subject to the mortgage stress test.

Get a Personalized Mortgage Estimate

Online examples are helpful, but every mortgage approval depends on:

-

income structure

-

employment history

-

credit score

-

debt levels

-

down payment

If you want a personalized estimate of how much house you could afford in Calgary, feel free to reach out.

I’m happy to review your situation and give you a realistic price range before you start house hunting.

Author

Mark Herman, MBA

Mortgage Broker – 22 Years of Experience

Mark helps Calgary home buyers navigate mortgage approvals, complex income situations, and lender options. His goal is to help clients secure the right mortgage strategy before they start shopping for a home.

Minimum Down Payment Canada: Rules, Examples & Options, 2026 Guide for Home Buyers

written by Mortgage Mark Herman; MBA with 22 years as a top mortgage broker

Minimum Down Payment in Canada: What Home Buyers Need to Know

One of the first questions people ask when they start thinking about buying a home is:

What is the minimum down payment in Canada?

The answer depends on the price of the home and how the mortgage is structured.

Understanding the rules early can help you figure out how much you need to save and what you qualify for.

Let’s walk through the basics.

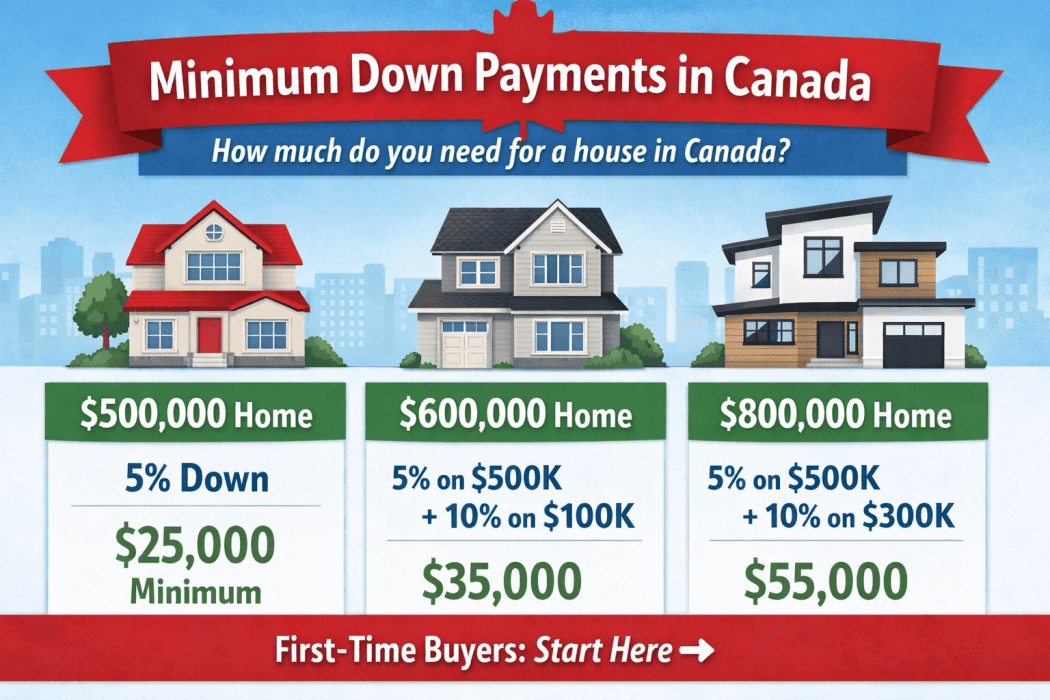

Minimum Down Payment Rules in Calgary, and all of Canada

In Canada, the minimum down payment depends on the purchase price of the home.

Current rules are:

-

5% down on the first $500,000

-

10% down on the portion between $500,000 and $999,999

-

20% down for homes $1,000,000 or more

For example:

If you buy a $600,000 home, the minimum down payment would be:

-

5% on the first $500,000 = $25,000

-

10% on the remaining $100,000 = $10,000

Total minimum down payment = $35,000

High-Ratio vs Conventional Mortgages

Your down payment also determines the type of mortgage you qualify for.

High-Ratio Mortgage (5% – 19% Down)

If your down payment is less than 20%, your mortgage is considered a high-ratio mortgage.

This means the mortgage is more than 80% of the home’s value, so lenders require mortgage default insurance through providers like:

-

CMHC

-

Sagen

-

Canada Guaranty

The insurance premium is added to your mortgage amount and paid over time.

The upside? High-ratio mortgages often qualify for lower interest rates.

Conventional Mortgage (20% Down or More)

If you put 20% down or more, the mortgage is considered conventional.

This means:

-

No mortgage insurance required

-

Lower borrowing costs overall

-

More flexibility with lenders

Down Payment Requirements for Calgary Buyers

The minimum down payment rules in Canada apply nationwide, including here in Calgary.

However, many Calgary buyers are surprised to learn how little down payment they actually need. For example, a $500,000 home in Calgary could require as little as $25,000 down, which is often less than people expect.

If you’re buying in Calgary or Alberta and want to see what your numbers look like, it’s worth running the calculations early so you know your options.

Where Your Down Payment Can Come From

Lenders also need to verify where the down payment funds come from.

Here are the most common sources.

Savings or Investments

If your down payment is coming from:

-

savings

-

chequing accounts

-

investments

Lenders will require 90 days of account history.

This verifies that the funds belong to you and were not recently borrowed.

Your statements must clearly show:

-

your name

-

the account number

-

the transaction history

Gifted Down Payment in Canada

A gift from family is one of the most common ways buyers fund their down payment.

The gift can come from a family member not only in Canada but from almost anywhere in the world. It does need to be transferred into any Canadian financial institution to be used though.

However, lenders require confirmation that the gift does not need to be repaid.

This is done with a gift letter signed by both parties confirming it is a non-repayable gift.

The gift must come from a direct family member; mother, father, brother, sister, grandparent, legal guardian.

Using RRSPs for Your Down Payment

Canada has a program called the Home Buyers’ Plan (HBP).

It allows first-time buyers to withdraw up to $35,000 from their RRSP tax-free for a down payment.

Key details:

-

You have 15 years to repay it

-

Repayment starts two years after withdrawal

-

If you don’t repay it, the amount becomes taxable income

To verify RRSP funds, lenders will need:

-

the RRSP withdrawal form

-

your RRSP statement

Using RRSPs if You’re Not a First-Time Buyer

You can still withdraw RRSP funds even if you’re not a first-time buyer, but it will be taxed as income.

The financial institution usually withholds about 30% for taxes.

This isn’t always ideal, but it can still work depending on the situation.

Borrowing Against Another Property

If you already own property, you may be able to use the equity in that property for your down payment.

This can be done through:

-

a refinance

-

a home equity line of credit (HELOC)

We just need to verify the available equity through your current mortgage statements.

Down Payment From the Sale of Your Current Home

Many buyers use equity from selling their existing home as their down payment.

In that case lenders require:

-

the firm sale contract

-

your current mortgage statement

-

confirmation of the sale proceeds

If your purchase closes before your sale, bridge financing can cover the gap.

This is a very common situation and usually easy to arrange.

Borrowing Your Down Payment

Some borrowers with strong income can qualify to borrow their down payment from an unsecured line of credit.

This strategy isn’t right for everyone, but it can work if your income supports the additional debt.

With rents rising and many buyers trying to enter the market, some people choose this route instead of continuing to rent.

Down Payment Examples in Canada

Here are some quick examples of minimum down payments based on purchase price:

$500,000 home

Minimum down payment:

5% = $25,000

$600,000 home

5% on first $500,000 = $25,000

10% on remaining $100,000 = $10,000

Minimum down payment = $35,000

$800,000 home

5% on first $500,000 = $25,000

10% on remaining $300,000 = $30,000

Minimum down payment = $55,000

FAQ: Down Payment Questions in Canada

What is the minimum down payment for a house in Canada?

The minimum down payment is 5% for homes under $500,000, with additional requirements for higher price ranges.

Can my down payment be a gift?

Yes. Many buyers use gifted down payments from family, but lenders require a signed gift letter confirming it is not repayable. Each bank has it’s own template so don’t try to do one yourself, we will send it to you to fill in and e-sign.

Can I borrow my down payment?

In some cases, yes. Borrowers with strong income may qualify to borrow their down payment from a line of credit.

Can I use my RRSP for a down payment?

Yes. The Home Buyers’ Plan allows withdrawals of up to $60,000 tax-free, with 15 years to repay the funds.

Final Thoughts

There are many ways to structure a down payment, and the right strategy depends on your finances and long-term plans.

If you’re thinking about buying, it’s worth running the numbers early so you know exactly what you qualify for and how much you need to save.

If you want help figuring out your options, you can start here:

https://markherman.ca/contact

About the Author

Mark Herman is a mortgage broker with 22 years of experience helping Canadians finance their homes. He holds an MBA in Finance and specializes in structuring mortgages for first-time buyers, self-employed borrowers, and real estate investors. He can be reached at 403-681-4376.