Prime rates should go up in July

This only affects variable rate mortgages and there are 2 increases to Prime expected for 2018, this one and one in December – depending on how the economy goes.

This only affects variable rate mortgages and there are 2 increases to Prime expected for 2018, this one and one in December – depending on how the economy goes.

- The Bank of Canada is expected to raise interest rates on July 11th.

- They normally increase Prime by 0.25% at a time, Prime is 3.45% now and should then go to 3.70%.

- The Central bank also emphasized that the increase will be needed to contain inflation.

This makes the 5-year fixed rates look much better as rates are slowly going back to 4% – the Theoretical Minimum

Mark Herman, Top Calgary Alberta Mortgage Broker

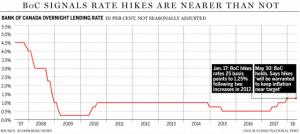

Some will wonder what stopped the Bank of Canada from raising interest rates today. It does seem likely that policy makers struggled with the decision, as they had little bad to say about the economy.

The reason for the delay is the same as it’s been since the start of the year: U.S. President Donald Trump. Canada’s central bank remains concerned that U.S. trade-and-tax policy will weigh on Canadian business investment, so much so that it is prepared to risk a little inflation by waiting for more clarity.

Few thought the central bank would raise interest rates on May 30. Poloz had been clear that he was comfortable with inflation running a little faster than the target rate of 2 per cent. He also said last month that hard evidence on investment would be a crucial variable and no such information has yet been published.

The central bank had been wary that its three interest-rate increases since last summer would choke domestic spending. But households seem to be coping just fine, which means the Bank of Canada can resume pushing interest rates higher.

Here is the link for the entire article: http://business.financialpost.com/news/economy/bank-of-canada-holds-interest-rate-at-1-25

The Details: What you need to know about “discount mortgages.”

Grandma always said, “The price is the price, but the details are the details!”

There are discounted and restricted mortgage rates out there but they do not share the details of their disadvantages up front with you.

- Restricted or Limited Products / Bait & Switch

People will not even sign a 3 year cell- phone contact any more but they will try to save $15 a month on a restricted mortgage; which could cost them $30,000 as a payout penalty – BUYER BEWARE is what the regulators say.

Brokers often advertise these products to get you to call them and then they switch you into a “regular product” if you are lucky – or you get a “restricted product” that you probably do not want if you know all the details.

Discount mortgages called “limited” or “restricted” and often have:

- No rate holds

- Only monthly payments

- Only 1 statement a year

- No on-line administration = call centre only

- Only 5/5 extra repayment option – most broker lenders are 15/15 + 2x or 20/20

- The 1st number is the % of the original mortgage amount you can repay every year without penalty

- The 2nd number is the increase in monthly payment in % you can do without penalty.

- The 2x = double the payment!

- And they use the bank payout penalty calculations – as below in the Dirty Trick – AND in addition to that penalty, a 3% fee of the entire mortgage balance added to the penalty!

- This could easily end up at $30,000.

The other main “Details” that are not often disclosed are:

2.Collateral Charge

To keep you from leaving the bank for a lower rate when you renew later, the banks register your mortgage as a collateral charge – which is the same as an “I owe you” / IOU for the home. Other banks will not take another banks IOU for a mortgage; which means:

- A lawyer will have to re-register your mortgage at land titles; $1000.

- An appraisal is needed as the registration is usually for more than the value of the home; $450

- http://blog.markherman.ca/?s=collateral

- This means on renewal you will not get the best rates because it will cost you about $1500 – $2500 to move banks – even after your term is over.

3. The “Dirty Trick” of how the banks calculate your payout penalty

- If you have to move or break your mortgage the payout calculation is usually way lower at a broker-only bank than any of the big banks. The big banks all calcualte the penatly the same way now – to their advantage, not yours.

- http://blog.markherman.ca/2015/08/26/payout-penalties-how-the-big-5-banks-get-you/

To avoid these products, or to disucss what your personal situation may be, call us any time at 403-681-4376.

Mark Herman, Top Calgary, Alberta, mortgage broker for renewals, first time home buyers and home purchases.

Graph shows why mortgage rates may go up soon

We watch all kinds of indicators for when mortgage rates may change.

This is the main one, the CMB – Canadian Mortgage Bond. As you can see it is on the way up and mortgage rates and the graph are directly related.

Rate Watch Program

When rates go up the banks call us and give us at least 2 hours – and sometimes 2 days – notice. This lets us send in all the files that we are working on for 120 day – or 4 month – rate holds. All the files that have enough data in them – at least an application and the disclosures and a payslip – get rate holds at today’s rates.

The banks do not do this for you! Another reason to use a broker that works the system to your advantage at no cost to you!

Mark Herman, top Calgary Alberta mortgage broker for new home purchases and mortgage renewals.

Calgary outpaces province

.")

Single-family home construction starts in Calgary and area hit 3,085 in the first six months of 2013

Photograph by: Files , Calgary Herald

Construction starts of single-family homes during the first half of 2013 in the Calgary area were the highest of all urban centres in Alberta — outpacing activity from a year earlier, says a federal agency.

Construction starts from Jan. 1 to the end of June reached 3,085, up nine per cent from 2,830 during the same time in 2012, says Canada Mortgage and Housing Corp.

The starts occurred in the Calgary census metropolitan area, which includes outlying communities such as Airdrie and Cochrane as well as the city.

The second-busiest centre from Jan. 1 to the end of June was the Edmonton census metropolitan area at 2,800, up eight per cent from 2,595 starts during the same period last year.

In terms of the Calgary area, “(single-family) home construction for the first half of 2013 has been fairly steady,” says senior market analyst Richard Cho of CMHC. “We’re seeing some economic factors that are supporting housing demand.”

Among those factors are employment opportunities, he says.

“In 2012, we had an impressive number of jobs created,” says Cho. “We had a record number of net migrants come to Calgary as well — and, of course, that will lead to a higher demand for housing.”

Net migration refers to the inflow of people to the Calgary area minus the outflow.

Last month, 554 single-family homes broke ground in the Calgary area, a 4.3 per cent improvement compared to 531 starts during the same month last year.

But for the month of June, construction starts of single-family homes in the Edmonton area were tops in Alberta at 589, up 13 per cent from 522 starts during the same month in 2012.

Total single-family housing starts for all urban centres in Alberta improved from Jan. 1 to the end of June 2013 compared to a year earlier.

In this span, 7,736 homes broke ground, up 11 per cent from 6,973 starts during the same period in 2012.

OVERALL TOTAL DECLINES

While construction starts of single-family homes in the Calgary area last month were up from the same time in 2012, total new home construction was down, says a federal agency.

Housing starts of all kinds — including multi-family development — eased to 912 in June, down 30 per cent from 1,184 during the same month in 2012, says Canada Mortgage and Housing Corp.

Visit cmhc-schl.gc.ca

Did the Flood Frustrate Your Real Estate Contract?

|

This is a repost from my good lawyer friend Jeff V. Kahane as he and I have had many questions about it. Did the Flood Frustrate Your Real Estate Contract? |

|

We’ve all seen the horrific images over the past weeks of those directly affected by record flood waters. What we haven’t seen reported in the mainstream media is those who have been directly impacted by virtue of having bought or sold a property, and settling on a possession date during or after the flood. |

Alberta almost at 4,000,000 people – they have to live somewhere

Paula Simons column in the Calgary Herald this weekend entitled “ Population Growth will Change Alberta forever” is, without a doubt, an interesting read.

The article states “Last year alone, Alberta welcomed almost 200,000 new arrivals (198,285 to be exact). Most fresh Albertans came from other parts of Canada more than 110,000.”

Paula continues the article “That breakneck pace isn’t slowing. In June, Statistics Canada reported an estimated 26,714 people moved to Alberta from other parts of Canada in the first quarter of 2013”

All of this will keep the Alberta housing market alive and rising as all these people have to live some where. The rental vacancy rate in Calgary is now less than 1%. Expect prices to rise due to the demand.

Population growth will change Alberta forever

No one is quite sure exactly when our provincial odometer will tick over, but some time in the next few weeks and months, there will be four million people living in this province.

Our current estimated total population is 3,965,339. That means we only need a population increase of 35,000 to reach four million. Of course, in a year, some people leave the province. Some die. Still, given Alberta’s annual growth rate of 3.2 per cent, by far the highest in Canada, we’re on track to hit 4.1 million residents by this time next year.

By way of comparison, British Columbia’s current population is 4.6 million.

“It’s a benchmark,” says Todd Hirsch, ATB Financial’s chief economist. “We’re going to require some time to think of ourselves as a province of four million people.

“This is no longer your grandfather’s Alberta. At these current growth rates, Alberta will surpass British Columbia by the year 2020.”

“The momentum is ours, because of the jobs and economic activity we have here,” says Alberta Finance Minister Doug Horner. “Frankly, four million is a big number. But we’re going to hit the five-million mark sooner than most people think — before 2020. No doubt there’s going to be a shift in the way Albertans think about their future.”

Frank Trovato is a professor of demography and population studies in the University of Alberta’s department of sociology.

“A milestone of four million is not insignificant for people, for their sense of self,” he says.

“Growth means more influence from a cultural, political and economic perspective,” Trovato says. “I think, as a province, we are developing a greater sense of who we are, a greater sense of our own importance.”

In truth, we’ve long thought of ourselves as a province of three million or so, fourth place in Confederation. But we may have reached both a demographic and a psychological tipping point.

Last year alone, Alberta welcomed almost 200,000 new arrivals — 198,285, to be precise. Who were they, exactly? The answer may surprise you.

In 2012, Alberta saw a record number of immigrants: 35,764, from some 200 different countries, with the largest number coming from the Philippines, India, China and the United Kingdom.

Alberta also produced a record number of babies last year — a bumper crop of 52,398.

But most “fresh” Albertans came from other parts of Canada. In 2012, more than 110,000 people migrated from other provinces to this one.

That breakneck pace isn’t slowing. In June, Statistics Canada reported an estimated 26,714 people moved to Alberta from other parts of Canada in the first quarter of 2013. In the same quarter, another 13,276 left Alberta — we’re a province in flux. Still, that gave us a net interprovincial gain of 13,438 — one of the highest quarterly gains Alberta has seen in the last 20 years.

The majority of new arrivals, whether from abroad or another province, are young — between 18 and 44, in their prime child-bearing years. Indeed, last year, Alberta actually “produced” almost 10,000 more babies than British Columbia.

IT consultant Karen Parker, 35, and her husband Dan Sameoto, 34, a professor of mechanical engineering, are a case in point. She’s from Hamilton, Ont. He grew up in Dartmouth, N.S. They moved to Edmonton three years ago from Vancouver, after Sameoto got a job at the U of A. Their son Robert was born here one month later. Three weeks ago, he was followed by a very fresh Albertan, baby sister Charlotte.

How is life in Alberta? “It was definitely a big adjustment for us,” says Parker. “I actually didn’t know how to drive when I moved to Edmonton! But we love the city. We love our neighbourhood. We love our quality of life. It’s also a super family-friendly city. There’s so much to do with kids here. We’re not going anywhere else, any time soon.”

The demographic shift Parker and Sameoto illustrate is reshaping our province in profound ways, changing our political and social culture, transforming what it means to be a “typical” Albertan.

“We are becoming more diverse, culturally and ethnically,” says Trovato, “and much more urban.”

Is this remarkable growth good news? Bad news? Something between? Certainly, our extraordinary demographic trend stands to gobble up agricultural land, tax our watersheds, strain our electrical grid, our freeways, our schools, our hospitals.

Keeping pace isn’t easy. Yet just as economic prosperity drives population growth, population growth itself helps to fuel the economy, creating more demands for goods, for services, for housing.

As we close in on the four-million mark, as we plan for five million, we must find ways to balance the demands of growth with the needs of our community and of our environment, ways to reform our political institutions to reflect more fairly our new demographic realities.

It’s time for us to lose our inferiority complex, that chip on our shoulders. Time for us to prepare for a new role, and new destiny.

Paula Simons is an Edmonton Journal columnist.

How low are interest rates? Really? Here is the big picture…

I just found this and thought it would be interesting for clients that call and tell me 3.49% for a 5 year fixed is way to high!

I’m not sure what you were expecting so here is a good barometer of the real picture.

- 6.5% = the 30 year average of the 5 year fixed closed, mortgage term

- 4.0% = the theoretical lowest the 5 year can go as banks need to borrow the funds, administer them and make a profit,

- 2.89% = the lowest the 5 year rate has ever been.

Now for the big picture…

Short version: rates are the lowest of all time … like a 496 year low. Is that low enough?

“in July 2012, 10-year yields in the US thus reached with 1.39% the lowest level since the beginning of records in the year 1790.

In the Netherlands – which provide the longest available time series for bond prices – interest rates fell to a 496 year low.

In the UK, ‘base rates’ are currently at the lowest level since the founding of the Bank of England in 1694.

In numerous countries (Germany, Switzerland), short term interest rates even fell into negative territory.”

SO … mortgage interest rates have never been lower and now the trend is up.

Why you should NOT renew your mortgage with the bank … The BANK has the BANK’S interests ahead of yours – ALWAYS!

Why you should NOT renew your mortgage with the bank … without checking with a broker (me) first, because the BANK has the BANK’S interests ahead of yours – ALWAYS!

Below is an article that shows the bank does not have your best interest in mind. Because they are paid to make money, not help you make the best decision for your finances. I get calls like this every day from incorrect mortgage payoffs to bad advice overall. Now you can see how clear it is with this example.

Paying off mortgage safer than investing the cash

Study after study suggests that Canadians are having a tough time paying off their mortgages, as debt levels continue to hit record levels year after year. Why?

Could it be that there are more opportunities to spend? Could it be that some people don’t want to pay off their mortgages faster?

Or are some professionals advising alternate investment strategies, suggesting that paying off the mortgage is not the best financial strategy?

BIG MORTGAGES AFFECT RETIREMENT

Rebecca and Darcy are in their mid-50s and are starting to think about retirement planning; they would like to retire in the next five years.

One of their biggest hurdles is a $225,000 mortgage. Currently, their $2,200 monthly payment would have the mortgage paid off in 10 years.

Rebecca and Darcy recently both received increases in pay at work, allowing them to increase their mortgage payments by $1,000 per month and pay off their mortgage in just under seven years.

Just as they were working with the banker to renew their mortgage, Darcy also got news that he is going to receive a significant inheritance, which he could use to pay off the mortgage all at once. When they asked the banker what they should do, the advice concerned them.

ADVICE FROM THE BANK

The banker suggested that in a low-interest-rate environment, paying off the mortgage might not be the best thing to do with the $225,000 inheritance.

Instead, they could invest it into a mutual fund that made over six per cent over the past year and over five per cent compounded over the last five years. With mortgage rates at 2.5 to three per cent, higher investment returns would mean more money in their pocket.

The banker put together a nice graph showing Rebecca and Darcy that investing the $225,000 would give them over $315,000 in seven years at five per cent, and that their $3,000 monthly payment would mean the mortgage would be paid off at the same time.

The bank’s conclusion? Keep the mortgage and invest the lump sum for a higher return.

WHAT WOULD YOU DO?

The banker is mathematically correct, but the big “if” lies in the rate of return, which cannot be controlled or predicted. The five-per-cent return is not guaranteed; what if the next five years aren’t as generous?

I ran some numbers at two per cent for the couple, and in that scenario, $225,000 would only grow to $258,000 after seven years. Alternatively, paying off the mortgage and investing the $3,000 per month mortgage payment at the same two per cent would give them $274,000 after the same period.

Basically, if the return on investment is greater than the interest cost on the mortgage, then the math would tip toward investing money. If the return on the investment is lower than the interest rate on the mortgage, then the math would tip toward paying off the mortgage.

We could complicate the calculation with after-tax returns, but we’ll keep things simple for this column.

The bottom line is paying down the debt is a more conservative option. It puts more control, flexibility and security in the hands of Rebecca and Darcy. Investing is always great when the returns come, but a good return is not guaranteed.

The banks make money when you keep a mortgage and they also make money when you invest in their mutual funds. Could that have any influence over the banker’s advice here?

There is no right or wrong solution here. Both investing and paying down a mortgage are financially responsible.

I tend to err on the conservative side, so if I were in Rebecca and Darcy’s shoes, I would pay off the mortgage, then invest the $3,000 per month for retirement. What would you do?

Jim Yih is a financial expert. Visit his award-winning blog, RetireHappyBlog.ca

© Copyright (c) The Edmonton Journal

Calgary housing market smashes records in May

The people that buy high end homes are often “job creators” and able to see what is happening in their business. They can see that things are going well now and are looking better in the future. All great for our continued economic prosperity in Calgary.

Prices and luxury home sales reach new lofty levels

CALGARY — Calgary’s resale housing market set a number of records in May.

According to preliminary, unofficial data on the Calgary Real Estate Board’s website, new levels were reached during the month for median and average MLS sale prices in the single-family market as well as for total residential sales in the city.

Also, the month had the highest level ever for luxury home sales of properties more than $1 million, according to Mike Fotiou, associate broker with First Place Realty in Calgary. There were 84 luxury home sales in May, besting the record for any month which was previously 80 in May 2012.

Kaitlyn Gottlieb, a realtor with Century 21 Bamber Realty in Calgary, said the upper-end market is seeing an increased demand for inner-city luxury homes with areas such as Hillhurst, Crescent Heights, Capitol Hill, Altadore and Parkdale some of the most coveted for homebuyers who are seeking the level of craftsmanship and detail you traditionally find in estate-style homes. It’s a development trend that shows no signs of slowing down.

“Today’s Calgary’s real estate market continues to show positive growth with steady price increases which are especially apparent in the starter to average single-family home sales, signalling a high level of confidence in both buyers and sellers,” said Gottlieb. “Inventory is increasing, although remaining lower than last year and properties particularly under $500,000 are selling very close to asking price in a shorter period of time, as buyers are prepared and ready to move on properties as they become available. We are also seeing an increase in competing offer situations as a result of the high demand and the lower inventory currently on the market.

“As we move into a more balanced market, buyers are also seeing great opportunities in Calgary’s market and as prices increase, the inventory increases, offering more choices for buyers. Calgary’s growing economy coupled with the tightening rental market and recent rental increases (contribute) to the market’s activity as renters move away from renting and into home ownership.”

The average sale price of a single-family home in May reached a record of $521,887, eclipsing the previous mark of $518,604 which was set in March of this. Average sale prices during the month were up 4.03 per cent from a year ago. The median price was also a record at $454,400, up 4.24 per cent from last year. The previous median price record was $450,000 in March of this year.

Record prices were also set in May for total MLS residential sales in the city with the average price at $462,161, up 3.85 per cent from last year, and the median price at $406,500, up 4.23 per cent from May 2012.

Previous record prices for total MLS residential sales were set in March of this year at $460,903 for the average and $403,000 for the median.

“With Calgary’s moderate but steady increases in the average home price and increasing number of sales, both buyers and sellers can expect a positive and opportunistic spring market. Overall these factors equate to a positive housing market and long term sustainability for Calgary,” added Gottlieb.

In May, total MLS sales in the city of 2,543 were up 6.80 per cent from last year while single-family sales of 1,766 increased by 3.46 per cent.

Meanwhile, a special housing market report released Monday by TD Economics, said resource-based economies, like Calgary, are facing better economic prospects over the next two years.

“Known for better job opportunities, more and more new immigrants and Canadians are choosing Calgary as their main destination,” said the report. “The inflow of people is expected to help support housing demand and help mop up some of the large amount of new homes currently under construction in the metro area.”

Calgary is also starting 2013 from a stronger position than some other markets. Calgary’s housing market peaked in late 2007, at which point the market looked to be overpriced and overbuilt, said TD Economics.

“But, the housing market went through its correction once the recession struck in 2009 and there has been less froth in the market since. Existing home sales are down 32 per cent from the peak experienced in 2007, while home prices have remained relatively flat since 2009 – helping to stabilize the home price-to-income ratio,” it said.

“Growth in Calgary home prices is likely to moderate from the current pace, but should remain slightly positive over the forecast horizon. Furthermore, home sales are likely to continue to grow moderately and housing construction ought to occur at the pace of household formation.”

Only Calgary and Edmonton have increasing real estate markets!

A better headline would be: Name the 2 biggest cities in the Province that has the most in-migration, oil & gas jobs and projects, youngest and highest educated work force making the highest per person weekly wage in the country.

Calgary and Edmonton buck national housing market trend of declining sales

Only two major markets to see growth in existing home sales

CALGARY — A soft landing is underway in the Canadian housing market and should continue but Calgary and Edmonton are bucking the trend with sales rising compared with a year ago, says a new report released Tuesday by BMO Capital Markets.

The report, by Sal Guatieri, senior economist for BMO, said the Canadian housing market is “calming not crashing.”

“In most regions, sales have fallen at double-digit rates this year from high levels last year,” said Guatieri. “But the rate of decline has slowed recently.

“By contrast, Alberta enjoys decent sales growth.”

As of April, the three month moving average of sales in the existing home market was down 10.9 per cent across the country. However, Calgary and Edmonton were the only two major markets to see growth at three per cent and 1.2 per cent, respectively.

Also, while the average sale price across Canada rose by only 1.0 per cent, Calgary led the nation with a 7.5 per cent hike. Edmonton was up 3.2 per cent.

Guatieri said Calgary’s resale prices are “supported by good valuations, following the 2008 correction, and strong job growth.”

“The upward trend should continue, as Alberta is expected to lead the nation’s economic performance in 2014,” he said.

According to the Calgary RealEstate Board, year-to-date until May 27, there have been 9,541 MLS sales in the city, up 3.89 per cent compared with the same period a year ago. The average sale price has risen by 6.6 per cent while the median price has increased by 5.51 per cent to $399,900.

At the national level. Guatieri said tighter mortgage ruls have slowed credit growth, helping to cool the housing market in an orderly fashion.

“Lack of pent-up demand, with homeownership rates near 70 per cent, and elevated household debt have abetted the slowing,” he said.

“Nationwide, sales are expected to stabilize this year amid steady job growth. Although long-term interest rates are likely to rise moderately next year, they should remain relatively low for some time.”

Twitter.com/MTone123

© Copyright (c) The Calgary Herald