Mortgage Penalty Calculator Canada: How Fixed-Rate Penalties Are Calculated (2026 Guide)

Written by Mark Herman; MBA in Finance – Mortgage Broker with 22 Years of Experience

Quick Answer: Mortgage Penalty in Canada

If you break a fixed-rate mortgage in Canada, your penalty is usually:

- 3 months’ interest, or

- Interest Rate Differential (IRD)

You pay whichever is higher.

Most fixed-rate penalties in 2026 fall between:

- $5,000 to $30,000+

The exact amount depends heavily on how your lender calculates IRD.

Mortgage Penalty Calculator (Quick Estimate)

Use this simple method to estimate your penalty:

Step 1: 3 Months’ Interest

Formula:

Mortgage balance × interest rate × 3 ÷ 12

Example:

- $400,000 mortgage

- 5.00% rate

Penalty ≈ $5,000

Step 2: Estimate IRD – Interest Rate Differential

Formula:

(Your rate − current comparable rate) × balance × remaining months ÷ 12

Example:

- Balance: $400,000

- Your rate: 5.00%

- Current rate: 3.50%

- 24 months remaining

IRD ≈ $12,000

Your real penalty = the higher of the two

What Is a Mortgage Penalty?

A mortgage penalty is a fee you pay if you break your mortgage early by:

- selling your home

- refinancing

- switching lenders

- paying off your mortgage before the term ends

Fixed-rate mortgages almost always have higher penalties than variable-rate mortgages.

Why Fixed Mortgage Penalties Are So High

1. IRD replaces simple interest

Variable mortgages:

- 3 months’ interest is the max payout penalty

Fixed mortgages:

- The GREATER of 3-months interest or the IRD calculation (which ever is higher)

2. Rate changes increase penalties

If rates drop after you lock in:

- Your rate = higher

- Current rate = lower

Bigger gap = bigger penalty.

The bank says they were making all that interest before and now that you pay them back they will lend the money out at a lower rate so they need to “re-capture the interest that they expected to get before.”

During Covid when Calgary home owners mortgage rates were about 4% and the rates dropped to 2%, the IRD payout penalties were in the range of $20,000 to $45,000 on 5-year fixed mortgages!! What?

3. Each bank uses a different formula

This is the most important point.

Two identical mortgages can have very different penalties depending on the lender.

How Banks Calculate Mortgage Penalties (Canada)

RBC

- Uses IRD based on:

- posted rate for similar term

- minus your original discount

More complex than a simple “current rate” comparison

TD

- Uses posted rate for similar term

- subtracts your original discount

Often results in higher penalties than expected

BMO

- Similar to TD and RBC

- Uses posted rates and discount adjustments

Scotiabank

- Uses posted rate for closest remaining term

- adjusted for your original discount

- includes present-value calculation

CIBC

- Uses a comparison mortgage method

- compares:

- your rate (plus discount)

- vs current posted rate

Can produce significantly higher penalties

National Bank

- Uses a standard rate / posted rate approach

- adds capped 1 month interest component

Different structure than other banks

Why This Matters (Real Calgary Examples)

Example 1: Move-Up Buyer in Calgary

- Bought in 2023

- Needs bigger home in 2026

- Mortgage: $520,000

- Fixed rate: 4.79%

- 3 years remaining

Penalty could be $15,000–$25,000

Example 2: Refinancing to Pay Off Debt

- Calgary condo owner

- Wants to consolidate debt

- Mortgage: $300,000

- Fixed rate: 5.19%

Penalty: $8,000–$12,000

Still worth it in some cases—but must be calculated properly

Example 3: Rental Property Sale

- Investor selling in Calgary

Difference between lenders:

- Bank A: $9,000 penalty

- Bank B: $14,000 penalty

Same borrower, different lender = big difference

Fixed vs Variable Mortgage Penalties

| Mortgage Type | Typical Penalty |

|---|---|

| Variable | 3 months interest |

| Fixed | IRD or 3 months (whichever is higher) |

Fixed penalties are often 2–5x higher

How to Reduce or Avoid a Mortgage Penalty

1. Use prepayment privileges

Most lenders allow:

- 15% lump sum annually

- 15% payment increases, and doubling the payment

2. Consider portability

You may be able to transfer your mortgage to a new property and not pay the penalty as you are not closing down your mortgage. You are porting it to another address.

3. Time your refinance

Waiting until renewal = no penalty

4. Choose the right lender upfront

This is the biggest factor.

Rate matters—but penalty structure matters more long-term

Internal Resources (Recommended Reading)

- Minimum Down Payment Canada: Rules, Examples & Options

- How Much Income Do You Need to Buy a House in Calgary

- Fixed vs Variable Mortgage Rates in Canada

- OnlyFans Mortgage in Canada

- Mortgage Renewals Guide

FAQ: Mortgage Penalties in Canada

How is a mortgage penalty calculated?

It is the greater of:

- 3 months’ interest

- IRD (interest rate differential)

Why are fixed mortgage penalties so high?

Because IRD estimates the lender’s lost interest over time—not just a simple fee.

Can two banks charge different penalties?

Yes—and the difference can be thousands of dollars.

Can I avoid a mortgage penalty?

Sometimes, by:

- porting your mortgage

- waiting until renewal

- restructuring your mortgage

Is there a standard penalty formula in Canada?

No. Each lender uses its own variation of IRD.

Bottom Line

Most borrowers focus on:

getting the lowest rate

But ignore:

how expensive it is to break the mortgage

In many cases:

The penalty matters more than the rate. Depending on your situation – like moving out of the country in 1 or 2 years.

If you’re planning to:

- refinance

- sell early

- restructure your mortgage

I can help you:

- estimate your real penalty

- compare lender formulas

- avoid costly mistakes

Reach out for a personalized strategy.

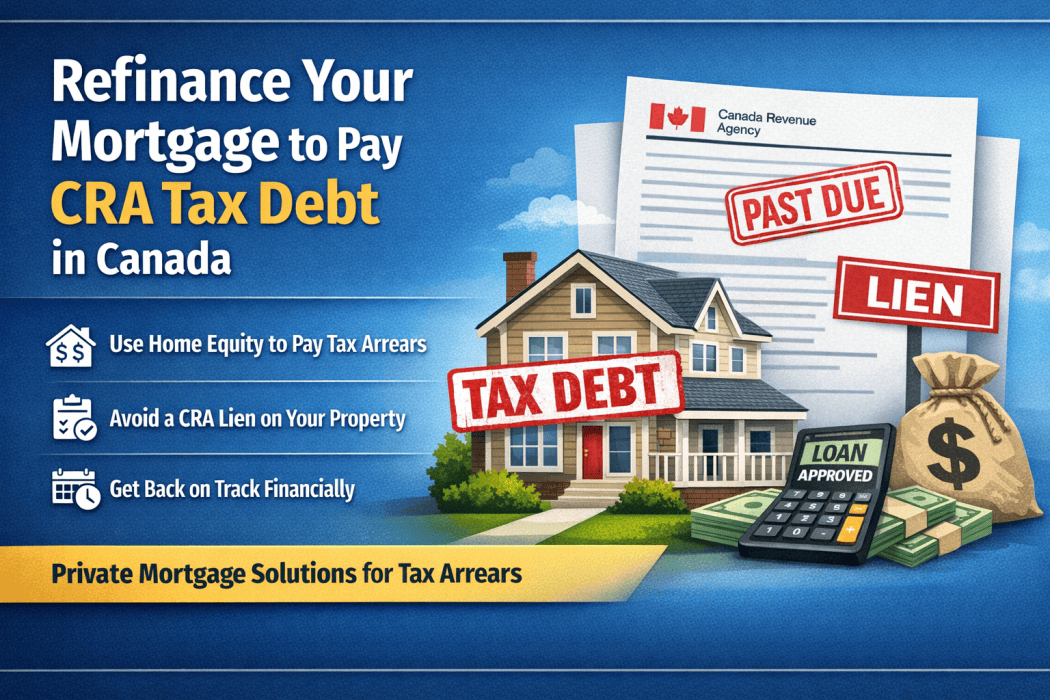

Can I Use a Mortgage to Pay CRA Tax Debt in Canada? (A Real Example of a Private Refinance)

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience specializing in new home buyers and tough deals.

Many Calgary and Canadian homeowners are surprised to learn that the CRA can place a lien on their home for unpaid taxes. Once that happens, refinancing becomes much harder.

The good news is that homeowners with equity often still have options. In many cases, a private mortgage refinance can be used to pay CRA tax debt, remove the lien risk, and give you time to get your finances back on track.

Below is a real example of how this works.

Real Example: Refinancing to Pay $29,000 in CRA Tax Debt

A self-employed homeowner recently contacted me about refinancing their mortgage to deal with back taxes owed to the Canada Revenue Agency (CRA).

Here was the situation:

Business tax situation

-

Business filings completed up to Oct 2022 – Sept 2023

-

Currently working with an accountant to file Oct 2023 – Sept 2024

-

Next filing period 2024–2025 still pending

-

GST paid up to end of 2024

-

GST may still be owing but amount unknown until filings are complete

Income structure

-

Owner pays themselves from the business when income comes in

-

No dividends issued

-

Most tax liability flows to personal taxes

Personal tax situation

-

Approximately $29,000 in personal tax debt to CRA

CRA had indicated they may place a lien on the property, which would make financing much more difficult.

The homeowner didn’t currently have the cash to pay the taxes, and they were also trying to pay their accountant to complete outstanding business filings.

Why CRA Debt Is a Problem for Mortgage Lenders

Most traditional lenders (banks and credit unions) require that CRA debt be fully paid before they approve a mortgage refinance.

They want to ensure:

-

There is no CRA lien registered

-

All tax filings are up to date

-

There are no outstanding collection issues

If these conditions are not met, the bank will usually decline the mortgage.

How a Private Mortgage Can Solve the Problem

In situations like this, a private lender refinance can be used to:

-

Pay off the CRA tax debt

-

Prevent or remove a CRA lien

-

Provide time to complete tax filings

-

Stabilize finances before returning to a traditional lender

Private lenders focus primarily on:

-

Equity in the property

-

Property value

-

Exit strategy (how the loan will be repaid or refinanced later)

They are often much more flexible when dealing with self-employed borrowers or tax arrears.

Typical Structure of a CRA Tax Debt Refinance

A refinance for tax debt usually works like this:

Step 1 – Property appraisal

The lender confirms the home’s value and available equity.

Step 2 – Mortgage approval

A private lender approves a mortgage based on the equity position.

Step 3 – CRA payout

Funds from the refinance are used to pay CRA directly.

Step 4 – Short-term mortgage

The homeowner keeps the private mortgage for 12–24 months while fixing their tax situation.

Why Acting Before a CRA Lien Matters

Timing is critical.

If CRA registers a tax lien on your property, refinancing becomes significantly more complicated because:

-

The lien must be paid during the refinance

-

Some lenders refuse to fund if the lien is already registered

-

Legal costs can increase

Getting financing before the lien is registered gives homeowners far more options.

Who This Strategy Works Best For

Using a private mortgage to pay CRA debt can work well if you:

-

Own a home with significant equity

-

Are self-employed

-

Have unfiled taxes that are being completed

-

Need time to catch up financially

This strategy is common for:

-

Business owners

-

Contractors

-

Real estate investors

-

Commission-based professionals

The Exit Plan: Moving Back to a Traditional Mortgage

Private mortgages are usually short-term solutions.

During the term, the goal is to:

-

Complete all tax filings

-

Pay CRA balances

-

Improve income documentation

-

Refinance into a lower-rate bank mortgage

Featured Snippet – Q&A Section

Frequently Asked Questions About CRA Tax Debt and Mortgages

Can you refinance your home to pay CRA tax debt in Canada?

Yes. Homeowners with sufficient equity can often refinance their mortgage to pay CRA tax debt. If traditional lenders will not approve the refinance, a private mortgage lender may still provide financing based on the home’s equity.

Can CRA put a lien on your house for unpaid taxes?

Yes. The Canada Revenue Agency can register a tax lien against your property if taxes remain unpaid. Once registered, the lien attaches to your home and must usually be paid before selling or refinancing.

How much equity do I need to refinance to pay tax debt?

Most private lenders will allow refinancing up to approximately 75–80% of the home’s value, depending on the situation and property location.

Will banks refinance if I owe CRA money?

Most banks require that CRA debts be paid first and tax filings be up to date. If taxes are still outstanding, homeowners often need to use a short-term private mortgage to pay CRA and then refinance with a bank later.

Mortgage Example Calculator Section

Example: Using a Mortgage Refinance to Pay CRA Tax Debt

Let’s look at a simplified example.

Home Value: $700,000

Current Mortgage: $420,000

Maximum Refinance at 80%: $560,000

Potential equity available:

$560,000 – $420,000 = $140,000 available

If the homeowner owes $29,000 in CRA taxes, they could refinance and:

-

Pay the CRA debt in full

-

Cover legal and appraisal costs

-

Possibly consolidate other high-interest debts

This type of refinance is commonly used as a temporary strategy, allowing the homeowner to clean up their tax situation before moving back to a traditional lender.

Frequently Asked Questions

Can CRA force the sale of my home?

Yes, in extreme cases CRA can pursue legal action that could eventually lead to the forced sale of property.

However, most homeowners resolve the issue by paying the tax debt through refinancing.

Can I get a mortgage if my taxes aren’t filed?

Traditional lenders usually require all tax filings to be current.

Private lenders may still consider the mortgage if:

-

You are actively working with an accountant

-

The property has enough equity.

How much equity do I need to refinance CRA debt?

Most private lenders require the mortgage to stay below about 75–80% of the home’s value, although this varies.

Final Thoughts

Tax debt with CRA is stressful, especially for self-employed homeowners. But if you own property with equity, a private mortgage refinance can provide a solution to clear the debt and buy time to get your finances organized.

The key is acting early — before CRA registers a lien on your home.

Author Bio

Mark Herman, MBA is a mortgage broker with 22 years of experience helping homeowners across Canada solve complex financing situations, including tax debt, private mortgages, and self-employed income challenges.

Thinking twice when handing your mortgage over to a bank adviser

Great story below of a recent Scotiabank advisor messing up a deal so bad that it ended up disqualifying a buyer from getting a special at 3.69% insured mortgage when market rates are 4.45%.

Bank advisors mess up all the time and I hear about it all the time. Maybe 15% of our deals get to us from bank mess ups.

In the story cut and paste below these buyers just would have ended up with a a higher rate but their deal wold still work… this one caused a 1 year delay.

Let me tell you a mortgage story…

We had a customer that we helped sheppard past 3 or 4 fiery hoops getting his mortgage ready for approval with a bumpy past we were smoothing over. Then 1 day he calls and says a met a bank mortgage rep at a gas station, that bank rep “guaranteed” him getting approved so our customer applied and … surprise – worse than a decline, CMHC declined him.

CMHC was the only lender that would do his specific deal, for the mess he was in, and/ but CMHC NEVER forgets – anything. All the insurers retain all data for ever. So he now had to wait another 12 months to get insurer approval. The delay in the end was 12 additional months that he had to wait before he could buy.

So … Think twice before handing over your mortgage to a bank adviser

Mark Herman, Best mortgage broker in Calgary Alberta for new home buyers.

Opinion: Think twice before handing your mortgage to a bank adviser – CMT News

Written by Ross Taylor, Mortgage Strategies, Opinion,

Let me tell you a story.

Recently, a major chartered bank ran a very competitive promotion: 3-year fixed rates at 3.69% for insured files and 3.99% for conventional files. Needless to say, these rates were popular, business was booming, both for the bank and for brokers working with them.

We had pre-approved a young couple earlier in the year, but when it came time to seek approval on a home they had made a successful offer on, they first went directly to their local branch to withdraw funds from their First Home Savings Account (FHSA).

When a branch adviser steps in

During that visit, the branch financial adviser offered to handle their mortgage as well. He convinced them there was no need to come back to our team, he had it all under control.

They also explored options at another bank, but the rates they were offered were mediocre. Our promo was still the best rate in town.

The deal gets declined, and there’s no second chance

But here’s the twist. After the financial adviser submitted their deal, it was declined. He escalated the deal to senior management, but again was given a firm no.

When they came back to us and told me the news, I was shocked. I couldn’t understand why they were declined. On paper, this was a strong file. Solid income, great credit, and their debt service ratios were within reasonable bounds.

Misinterpreting income cost them the deal

I asked if they were told why they were turned down, and they said, “because our debt service ratios were over the 39/44 limit.”

Now, their pay stubs were a bit complicated, I’ll give you that. But we had their T4s, and I could easily make a case for either using a two-year average or taking their current full-time salary. Both would have worked. You just had to know how to interpret the documentation properly.

I contacted our Business Relationship Manager at the bank and asked if I could re-submit the file. After all, it had been declined, and I felt confident we could get it approved with the correct interpretation of income. But the answer was a firm no.

Why bank policy closed the door

The bank’s position was that I wouldn’t want another broker or branch employee taking one of our approved files and trying to submit it again. And while I understand the sentiment, this wasn’t the same thing. This wasn’t poaching a win, it was salvaging a decline.

But rules are rules, and because the file had already been escalated and declined by the branch, there was no path forward for me to resubmit it — even if I knew how to fix it.

What’s the lesson here? Be careful who you trust with your mortgage

This story isn’t about one bank being better than another. It’s about understanding that not all mortgage advisers are created equal. When you walk into a branch, you’re often speaking to a generalist. They might have good intentions, but they don’t always have the same level of mortgage-specific training or experience as a full-time mortgage broker.

And the consequences of that can be enormous. In this case, the clients lost out on a great rate and had to start over, simply because it seems their adviser didn’t fully understand how to package their income. And once the file was declined, there was likely no second chance.

The bottom line

Mortgages are complex, especially if your income is even slightly non-standard. Getting declined not only wastes time, it can actually prevent you from accessing the best deals, even if you’re fully qualified. Before you hand over your file to someone behind a desk at your local branch, ask yourself: do they really specialize in mortgages?

Because once a file is escalated and declined at the bank level, it may close off options you didn’t even know you had.

Make sure you’re putting the biggest financial transaction of your life in the right hands.

Summary: RE/MAX Canada Fall 2025 Housing Market Outlook

“54% of Canadians believe this fall is a good time to strike a deal on a home.”

Here’s a summary of the RE/MAX Canada Fall 2025 Housing Market Outlook piece, released Sept 21st:

- Pricing Trends: Residential price trends varied regionally, rising across Atlantic Canada and the Prairies, while declining in major urban centres in Ontario and British Columbia.

- National average home prices are expected to decrease by about 6.5% this fall.

- 68% of Canadians say a five- to 10-per-cent drop in property prices would make a meaningful difference in their ability to enter the market.

- Sales Activity: Home sales declined year-over-year in 62% of markets analyzed between January 1 and July 31, 2025.

- Buyer Optimism:

- 38.2% of housing markets are sitting firmly in buyer’s territory this Fall.

- 7% of Canadians say they intend to buy their first home within the next 12 months.

- 28% of Canadians planning to buy their first home in the next 12 months say they have saved at least 20 per cent for their down payment.

- 64% of Canadians say they’d feel ready if interest rates fell by 0.5 to one per cent.

- Seller Market:

- 26.4% of housing markets are expected to favour sellers this Fall.

- 8% of Canadians say they plan to sell their home in the next year, and among them, confidence is strong.

- 63% of those planning to sell believe they’ll be able to secure their asking price.

- Homeowner Sentiments:

- 92% of Canadian homeowners see their homes as a solid long-term investment.

Click here to read the full report!

Now is the perfect time to buy a home in Alberta as it is a solid BUYERS MARKET!

Mortgage Mark Herman, best first time home buying mortgage broker in Calgary Alberta

Or call me for a chat at your convenience.

Mortgage Mark Herman

Insured Refinance when funds are used to build a legal suite!

What if your home could help pay for itself?

We have an exclusive lending program that allows homeowners to refinance their mortgage and add a legal rental suite—all in one step.

Here’s why this is a game-changer:

- ✅ Borrow against your home’s future value (“as improved value”)

- ✅ Finance up to 90% of the as-improved value (maximum $2M)

- ✅ Rental income from the new suite can be used to help qualify

- ✅ Options for up to a 30-year amortization to keep payments affordable

- ✅ Consolidate existing debt into your new insured mortgage

This program is designed specifically to help Canadians:

- Convert underutilized space into a legal rental suite

- Boost property value while creating a new income stream

- Contribute to housing availability in the community

Because this is a specialized product, it’s not available everywhere—only through select mortgage professionals like me.

If you’ve been considering adding a suite to your home, this could be the perfect time.

Call to learn how this program can work for you.

Its true, you can GET BEST RATES when you refinance / remortgage and use the funds to build a suite

This is the best way to put your home to work for you.

Mortgage Mark Herman, Best Calgary mortgage broker specializing in refi+renos