Calgary Bridge Financing | Buy Before You Sell in Alberta

Buying a new home before your current home sells can feel impossible.

You find the right property. The closing date is coming fast. Your existing home is listed, but it has not sold yet. Your down payment is tied up in equity. The bank may not be able to move quickly enough. And now you are stuck between two houses, two timelines, and a lot of pressure.

This is where bridge financing can be a powerful solution.

A recent private-lender case study showed how one homeowner purchased a $3.2 million primary residence before their existing home sold. They had $500,000 available for a down payment, but needed interim financing to close on the new home while waiting for the current property to sell. The solution was a $2.5 million bridge mortgage, structured as a short-term, open mortgage with interest-only payments.

That type of solution is not for every borrower, but it shows what is possible when the file is structured properly.

What Is Bridge Financing?

Bridge financing is short-term mortgage financing designed to “bridge the gap” between buying a new property and selling your current one.

In plain English:

You want to buy now.

Your current home has not sold yet.

You need temporary financing to close the purchase.

The bridge mortgage is paid out when your existing home sells.

For many Calgary and Alberta homeowners, this can prevent a rushed sale, reduce stress, and give them time to complete the move properly.

When Bridge Financing Makes Sense

Bridge financing may be useful when:

- You have found the right home but your current home has not sold yet.

- You need to close quickly.

- Your equity is strong, but not yet available in cash.

- Your existing home is listed or expected to sell.

- You want to avoid accepting a low offer just because you are under pressure.

- The purchase is time-sensitive.

- A bank solution is too slow or too rigid.

In the case study, timing was a major issue. The borrower needed to close in under two weeks, and there was even a long weekend in the middle of the timeline. The lender still moved from inquiry to commitment in five business days.

That is exactly why planning and structure matter.

How the Case Study Worked

Here is the simplified version of the bridge-financing structure:

- New home purchase price: $3.2 million

- Available down payment: $500,000

- Bridge mortgage amount: $2.5 million

- Term: 6 mont

- Prepayment: Fully open, with no payout penalty

- Payment type: Interest only

- Loan-to-value: 41.67%

- Exit plan: Sale of the existing home within 6–12 months

The borrower’s existing home was also pledged as additional security. This helped reduce the overall risk and allowed the lender to structure the file in a way that worked.

This is important because bridge financing is not only about the new property. Lenders often look at the full picture, including the property being purchased, the property being sold, equity position, location, marketability, and the borrower’s exit strategy.

Why the Exit Strategy Matters

The biggest question in bridge financing is simple:

How does the lender get paid back?

Usually, the answer is the sale of the existing home.

That means the lender will want to understand:

- Is the current home listed?

- What is the realistic value?

- How marketable is the property?

- Is there an accepted offer?

- Are there conditions on the sale?

- How much equity is available?

- What happens if the sale takes longer than expected?

The stronger the exit plan, the better the file usually looks.

In the case study, the borrower planned to sell the existing property within 6–12 months, and the sale proceeds would repay the bridge mortgage.

Why Bridge Financing Is Different From a Regular Mortgage

A regular mortgage is usually built around long-term affordability.

Bridge financing is different. It is usually built around:

- Speed

- Equity

- Security

- Exit strategy

- Short-term repayment

- Flexibility

This is why bridge mortgages often come with higher rates and fees than traditional bank mortgages. They are solving a different problem.

The goal is not usually to keep the bridge mortgage for years. The goal is to use it as a short-term tool to complete the purchase, then pay it out once the existing home sells.

The Benefit of a Fully Open Mortgage

One of the most important features in the case study was that the mortgage was fully open.

That means the borrower could pay it out without a payout penalty.

For bridge financing, that flexibility matters. If your existing home sells in 30, 60, or 90 days, you do not want to be locked into a large penalty just to exit the temporary financing.

A fully open bridge mortgage can give you breathing room while still allowing you to repay the loan as soon as the sale closes.

Bridge Financing in Calgary and Alberta

In Calgary’s real estate market, timing can create real problems.

A buyer may find the right home before their current home sells. A seller may not accept a long financing condition. A possession date may not line up perfectly. A bank may require more time, more documents, or a firm sale before they are comfortable.

This is where a mortgage broker can be valuable.

Not every lender does bridge financing. Not every lender can handle larger loan amounts, acreage properties, private financing, or complex timing. And not every file fits neatly into a bank’s policy box.

A good mortgage broker can look at the whole picture and determine whether there is a workable solution.

Important Things to Know Before Using Bridge Financing

Bridge financing can be very useful, but it needs to be handled carefully.

Before moving ahead, you should understand:

- The interest rate

- The lender fee

- The broker fee

- Legal costs

- Appraisal requirements

- Whether payments are interest-only

- Whether the mortgage is open or closed

- How long the term is

- What happens if the current home does not sell on time

- Whether both properties are being used as security

The wrong structure can become expensive. The right structure can help you close with confidence.

The Bottom Line

Bridge financing is not about borrowing recklessly.

It is about solving a timing problem.

When the equity is there, the exit strategy is clear, and the file is structured properly, bridge financing can allow a homeowner to buy their next property before their current home sells.

For Calgary and Alberta homeowners, this can mean avoiding panic, protecting negotiating power, and moving forward without being forced into a rushed sale.

If you are buying before selling, or if your possession dates do not line up, it is worth reviewing your options before you make a firm offer.

Call to Action

Thinking about buying before your current home sells?

Let’s review the numbers before you make a move. Bridge financing is not right for everyone, but when it fits, it can be the difference between losing the home and closing with confidence.

Mortgage Mark Herman

Calgary & Alberta Mortgage Broker

403-681-4376

FAQ: Bridge Financing in Calgary and Alberta

What is bridge financing?

Bridge financing is short-term mortgage financing that helps you buy a new property before your current home sells. It is usually paid out when the existing home is sold.

Can I buy a home before selling my current home?

Yes, it may be possible if you have enough equity, a strong exit strategy, and a lender willing to provide short-term bridge financing.

Is bridge financing the same as a regular mortgage?

No. A regular mortgage is usually long-term financing. Bridge financing is short-term and is designed to solve a timing gap between buying and selling.

Is bridge financing expensive?

It can be more expensive than a traditional bank mortgage because it is short-term, faster, and often more complex. The rate, fees, and total cost should always be reviewed before proceeding.

Do I need my current home to be sold first?

Not always. Some bridge-financing options may be available before your current home sells, depending on equity, property value, lender policy, and the exit plan.

Can bridge financing help if my closing date is coming quickly?

Possibly. Some private lenders can move faster than traditional banks, but the file still needs proper documentation, valuation, legal review, and underwriting.

한국 신용기록으로 캐나다 모기지 가능할까? | 캘거리 한인 모기지 전문가

한국 신용기록으로 캐나다에서 주택담보대출(모기지)을 받을 수 있을까요? | 앨버타 한인 커뮤니티를 위한 모기지 가이드

작성자: Mark Herman, MBA – 22년 경력의 모기지 전문가

앨버타 한인들을 위한 특별한 모기지 솔루션

캘거리(Calgary), 에드먼턴(Edmonton), 그리고 앨버타 전역에 거주하는 많은 한인들은 집을 구매할 때 같은 문제를 경험합니다.

한국에서는 안정적인 직장과 좋은 신용기록, 충분한 자산을 보유하고 있지만 캐나다에 온 지 얼마 되지 않아 캐나다 신용기록(Credit History)이 부족한 경우가 많습니다.

대부분의 캐나다 금융기관은 캐나다 신용점수, 캐나다 소득 기록, 캐나다 은행 거래 내역을 중심으로 심사를 진행합니다.

하지만 많은 분들이 모르는 사실이 있습니다.

일부 경우에는 한국에서의 금융거래 내역과 은행 관계를 고려할 수 있는 모기지 프로그램이 존재합니다.

저는 앨버타에서 활동하는 모기지 브로커로서 Hana Bank Canada를 포함한 특별한 금융기관들과 협력하여 일반적인 캐나다 은행에서 제공하지 않는 모기지 옵션을 소개해 드리고 있습니다.

왜 한인들에게 중요한 프로그램일까요?

많은 한국인 신규 이민자와 유학생 출신 영주권자, 그리고 한국 기업 주재원들은 다음과 같은 장점을 가지고 있습니다.

- 한국에서의 우수한 신용기록

- 안정적인 직장 경력

- 충분한 예금 및 투자자산

- 한국 은행과의 오랜 거래 관계

- 높은 소득 수준

하지만 캐나다에서는 이러한 강점이 제대로 평가받지 못하는 경우가 있습니다.

따라서 한국 금융 시스템을 이해하는 금융기관과의 협력이 중요한 차이를 만들 수 있습니다.

Hana Bank Canada가 특별한 이유

Hana Bank는 대한민국을 대표하는 글로벌 금융기관 중 하나입니다.

캐나다 내에서도 한국 고객을 위한 금융 서비스를 제공하고 있으며, 한국과 캐나다를 연결하는 금융 네트워크를 갖추고 있습니다.

특정 조건을 충족하는 고객의 경우 다음과 같은 가능성을 검토할 수 있습니다.

한국 금융정보 활용 가능성

일부 프로그램에서는 한국 내 금융거래 이력과 자산 상황을 함께 고려할 수 있습니다.

한국 은행 거래관계 활용

오랫동안 유지해 온 한국 은행 거래 내역이 도움이 될 수 있습니다.

신규 이민자 프로그램

캐나다에 온 지 얼마 되지 않은 고객들을 위한 다양한 대출 옵션을 검토할 수 있습니다.

한국 고객 맞춤형 서비스

한국 금융 서류 및 재정 상황에 대한 이해도가 높은 금융기관과 협력할 수 있습니다.

어떤 분들에게 도움이 될 수 있을까요?

신규 이민자(Newcomers)

캐나다 신용기록이 부족하지만 한국에서 좋은 금융 기록을 보유한 분

전문직 종사자

의사, 간호사, 엔지니어, 회계사, IT 전문가 등

사업가 및 자영업자

한국 또는 캐나다에서 사업체를 운영 중인 분

첫 주택 구매자

캘거리, 에드먼턴, 에어드리(Airdrie), 코크레인(Cochrane), 오코톡스(Okotoks), 레드디어(Red Deer) 등에서 첫 집을 구매하려는 가족

왜 대부분의 모기지 브로커는 이 프로그램을 소개하지 않을까요?

대부분의 모기지 브로커는 캐나다 주요 은행과 일반적인 모기지 금융기관만 취급합니다.

하지만 한국 고객을 위한 전문 금융 프로그램에 접근할 수 있는 브로커는 매우 적습니다.

따라서 많은 한인들이 자신에게 더 적합한 금융 옵션이 있다는 사실조차 알지 못하는 경우가 많습니다.

제가 상담할 때 가장 먼저 확인하는 내용 중 하나는 다음과 같습니다.

- 한국 은행 거래 내역

- 한국 자산 보유 현황

- 한국 신용기록

- 한국 소득 기록

이러한 정보가 모기지 승인 가능성을 높이는 데 도움이 될 수 있기 때문입니다.

캘거리 및 에드먼턴 한인 모기지 전문가

저는 22년 이상 모기지 업계에서 활동하며 다양한 고객들의 주택 구입을 도와왔습니다.

모든 고객이 동일한 금융 솔루션을 필요로 하지는 않습니다.

중요한 것은 단순히 캐나다 신용점수만 보는 것이 아니라 고객의 전체 금융 상황을 종합적으로 검토하는 것입니다.

한인 커뮤니티에 속해 있으며 다음 중 하나에 해당한다면 상담을 받아보시기 바랍니다.

- 주택 구입 계획

- 재융자(Refinancing)

- 투자용 부동산 구매

- 신규 이민자 모기지

- 한국 금융기록 활용 가능성 검토

짧은 상담만으로도 다른 금융기관에서는 찾지 못했던 대출 옵션을 발견할 수 있습니다.

자주 묻는 질문 (FAQ)

한국 신용기록만으로 캐나다 모기지를 받을 수 있나요?

개인의 상황에 따라 다르며, 일부 금융기관에서는 한국 금융정보를 함께 검토할 수 있습니다.

영주권이 없어도 가능한가요?

비자 종류, 소득, 다운페이먼트 및 금융기관 기준에 따라 달라질 수 있습니다.

캘거리와 에드먼턴 모두 가능한가요?

네. 앨버타 전역의 고객들이 상담 가능합니다.

모든 모기지 브로커가 이 프로그램을 취급하나요?

아닙니다. 일부 브로커만 접근 가능한 전문 금융 프로그램입니다.

Mark Herman, MBA에게 문의하세요

앨버타에서 집을 구매하려는 한인 고객이라면 지금 상담을 받아보세요.

한국에서의 금융 이력과 자산이 캐나다 모기지 승인에 도움이 될 수 있는지 확인해 드리겠습니다.

캘거리, 에드먼턴 및 앨버타 전역 상담 가능

403-681-4376

MarkHerman.ca

Mark Herman 소개

Mark Herman, MBA는 22년 이상의 경력을 보유한 캘거리 모기지 브로커입니다. 신규 이민자, 전문직 종사자, 사업가 및 다양한 고객층을 위한 맞춤형 모기지 솔루션을 제공하고 있습니다.

Korean Mortgage Program in Alberta: Use Your Korean Credit History to Buy a Home in Canada

Korean Mortgage Program in Alberta: Can Your Korean Credit History Help You Buy a Home in Canada?

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

A Unique Mortgage Solution for Alberta’s Korean Community

Many Korean families moving to Calgary, Edmonton, and other Alberta communities face the same challenge when buying a home in Canada:

They have strong financial histories in Korea but limited Canadian credit history.

Traditional Canadian lenders often focus primarily on Canadian credit reports, Canadian income history, and Canadian banking relationships. This can create challenges for newcomers, recent arrivals, business owners, and families who have substantial financial assets and credit history in Korea.

What many people don’t know is that there may be mortgage solutions available through Hana Bank Canada that can consider Korean banking relationships and financial information as part of the qualification process. Hana Bank Canada is part of one of South Korea’s largest financial institutions and has a long history of serving Korean clients both in Korea and internationally.

As a mortgage broker in Alberta with access to this lender, I help eligible Korean clients explore financing options that many mortgage brokers simply cannot offer.

Why This Matters for Korean Home Buyers in Alberta

The Korean community in Alberta continues to grow, particularly in Calgary and Edmonton.

Many buyers arrive with:

- Strong employment histories in Korea

- Established Korean banking relationships

- Significant savings and investments

- Excellent Korean credit profiles

- Plans to purchase a home shortly after arriving in Canada

Unfortunately, these strengths do not always translate easily into approval through traditional Canadian mortgage programs.

This is where a lender familiar with Korean financial systems may provide additional options for qualified borrowers.

What Makes Hana Bank Canada Different?

Hana Bank is one of South Korea’s largest financial institutions and operates internationally, including in Canada. The organization has extensive experience serving Korean clients globally and maintains banking operations that connect Korean and Canadian financial services.

For eligible borrowers, this can create opportunities to:

- Explore mortgage options using Korean financial information

- Leverage existing Korean banking relationships

- Obtain financing solutions tailored to Korean newcomers

- Work with a lender familiar with Korean documentation and financial practices

Not every borrower will qualify, and lender guidelines change over time, but many Korean families are surprised to learn these options even exist.

Who May Benefit from This Program?

This program may be worth exploring if you are:

New to Canada

Many newcomers have excellent financial backgrounds but limited Canadian credit.

Korean Professionals

Engineers, healthcare professionals, accountants, executives, and other professionals relocating to Alberta may have strong income histories that deserve consideration.

Korean Business Owners

Entrepreneurs who own businesses in Korea or Canada often face unique mortgage qualification challenges.

Korean Families Purchasing Their First Canadian Home

Families planning to settle in Calgary, Edmonton, Airdrie, Cochrane, Okotoks, Red Deer, Lethbridge, or elsewhere in Alberta may find additional options available.

Why Most Mortgage Brokers Don’t Offer This

Most mortgage brokers work primarily with major Canadian banks, monoline lenders, and credit unions.

Very few brokers in Alberta have access to specialized international lending programs that serve the Korean community.

As a result, many Korean buyers never learn about these opportunities.

When clients contact me, one of the first questions I ask is whether they have Korean banking relationships, Korean assets, or Korean credit history that may help strengthen their mortgage application.

Calgary and Edmonton Korean Mortgage Specialist

Over my 22 years in mortgage lending, I’ve worked with clients from many backgrounds and understand that traditional mortgage solutions do not fit every borrower.

My goal is simple:

Find the best mortgage strategy available based on your complete financial picture—not just your Canadian credit file.

If you’re part of Alberta’s Korean community and are considering buying a home, refinancing, or exploring mortgage options, let’s have a conversation.

A short consultation may uncover financing opportunities that other lenders have overlooked.

Frequently Asked Questions

Can I get a mortgage in Canada with Korean credit history?

Possibly. Certain lenders may consider Korean financial information and banking relationships as part of the overall application process. Qualification requirements vary by lender.

Do I need permanent residency to qualify?

Not necessarily. Mortgage options can vary depending on your residency status, employment situation, down payment, and lender guidelines.

Is this available in Calgary and Edmonton?

Yes. Eligible borrowers throughout Alberta can potentially access these mortgage solutions.

Do all mortgage brokers have access to Hana Bank Canada?

No. Access to specialized lender programs is not available through every mortgage brokerage.

Contact Mark Herman, MBA

If you’re part of Alberta’s Korean community and want to explore your mortgage options, I’d be happy to help.

Whether you’re buying your first home in Canada, relocating from Korea, or looking for a lender that understands your financial background, let’s discuss your situation.

Call Mark Herman today for a confidential mortgage consultation.

About Mark Herman

Mark Herman, MBA, is a Calgary mortgage broker with 22 years of experience helping home buyers, newcomers, professionals, and business owners secure mortgage financing throughout Alberta. He specializes in finding creative lending solutions through both traditional and specialized mortgage lenders.

Down Payment Verification Requirements in Canada | Calgary Mortgage Broker

Down Payment Verification Requirements in Canada: How to Avoid Mortgage Approval Delays

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience in getting down payments to work in sticky situations and tight spots.

One of the most common reasons mortgage approvals are delayed is incomplete down payment documentation. With Calgary’s summer real estate market remaining active and purchase activity staying strong across Alberta, lenders are paying close attention to verifying the source and availability of down payment funds.

Whether you’re buying your first home, moving up to a larger property, or purchasing an investment property, understanding down payment verification requirements can help prevent frustrating delays during the mortgage approval process.

This guide explains what lenders require for different down payment sources and how you can prepare your documentation in advance.

Why Do Lenders Verify Your Down Payment?

Before approving a mortgage, lenders must confirm that:

- Your down payment comes from an acceptable source

- The funds are available for closing

- The money is not borrowed from an undisclosed source

- The transaction complies with lender and regulatory requirements

Providing complete documentation upfront allows underwriting to proceed smoothly and can significantly reduce requests for additional information.

Personal Savings as a Down Payment

Personal savings remain the most common source of down payment funds.

Documentation Required

Most lenders require:

- A minimum of 90 days (3 months) of account statements

- Statements showing:

- Account ownership

- Current balance

- Full transaction history

- Documentation explaining any large deposits

Common Issue: Unexplained Deposits

One of the biggest causes of delays occurs when a large deposit appears in an account during the 90-day review period.

For example, if $15,000 suddenly appears in your account, the lender may request documentation showing where the money originated.

Acceptable documentation may include:

- Sale receipts

- Investment redemption statements

- Bonus or commission pay stubs

- Gift documentation

- Transfer records between accounts

Mortgage Broker Tip

If multiple accounts are contributing to your down payment, provide statements for every account involved. Missing account documentation often leads to underwriting delays.

Using Sale Proceeds From an Existing Home

Many Calgary homeowners use equity from the sale of their current property as the down payment on their next home.

Documentation Required

Lenders typically require:

- A fully signed and firm (unconditional) purchase contract for the sale

- All addendums and condition waivers

- A current mortgage payout or balance statement

Why This Matters

The lender needs to confirm that sufficient net proceeds will remain after:

- Realtor commissions

- Legal fees

- Mortgage payout

- Other closing costs

The remaining equity must be enough to support the down payment being used on the new purchase.

Gifted Down Payments

Gifted down payments are common among first-time home buyers in Alberta.

Who Can Provide a Gift?

Most lenders permit gifts from immediate family members, including:

- Parents

- Grandparents

- Siblings

- Children

The gift must be non-repayable and documented appropriately.

Required Documentation

In addition to a completed Gift Letter, lenders generally require proof of the source of funds through one of the following:

- 90-day history of the donor’s account showing the funds

- 90-day history of the borrower’s account showing the gifted funds

- Signed attestation from the donor’s financial institution representative

Timing Requirements

Gifted funds should typically be deposited at least 15 days before mortgage funding.

Funds may be verified through:

- The borrower’s bank account

- A lawyer’s trust account

- A realtor’s trust account holding deposits in trust

Important Gift Rule

No portion of a gifted down payment can come from someone who has a direct or indirect financial interest in the sale of the property.

For example, a seller cannot provide funds that are disguised as a gift to help the buyer qualify.

Using RRSP Funds for Your Down Payment

Many first-time home buyers use Canada’s Home Buyers’ Plan (HBP) to access RRSP funds.

Required Documentation

Lenders generally require:

- Proof you are eligible for withdrawal under the Home Buyers’ Plan

- Recent 90-day account statements

- Documentation confirming the withdrawal

Benefits of Using RRSP Funds

The Home Buyers’ Plan allows eligible buyers to withdraw funds from their RRSP without immediate tax consequences, making it one of the most effective ways to increase a down payment.

Using a First Home Savings Account (FHSA)

The First Home Savings Account (FHSA) has become a popular down payment savings tool for first-time buyers.

Documentation Required

Lenders may request:

- Recent 90-day statements

- Evidence of FHSA ownership

- Withdrawal documentation

- Confirmation of eligibility

Because the FHSA is relatively new, lenders may request additional supporting documents depending on the financial institution holding the account.

Most Common Causes of Down Payment Verification Delays

After reviewing thousands of mortgage files over the years, these are the most common issues that slow down approvals:

Missing 90-Day History

Submitting only the most recent statement often results in an immediate follow-up request.

Statements Without Account Ownership

Screenshots or partial statements may not show who owns the account.

Large Unexplained Deposits

Any significant deposits should be documented before submission.

Incomplete Gift Documentation

Missing gift letters or missing proof of the donor’s funds frequently create delays.

Missing Sale Documents

Lenders require the full sale agreement and supporting documentation when using sale proceeds.

Missing RRSP or FHSA Statements

Withdrawal confirmations alone are often insufficient.

Down Payment Documentation Checklist

Before submitting your mortgage application, ensure you have:

☑ 90 days of statements for all down payment accounts

☑ Documentation for any large deposits

☑ Gift letter and supporting gift documentation (if applicable)

☑ Firm sale agreement and mortgage payout statement (if using sale proceeds)

☑ RRSP or FHSA statements and withdrawal documentation

☑ Statements clearly showing account ownership

Having these documents ready can significantly reduce underwriting delays and help your mortgage approval move forward more efficiently.

Frequently Asked Questions About Down Payment Verification

How many months of bank statements do lenders require?

Most lenders require a minimum of 90 days (three months) of account history showing the down payment funds.

Can I use gifted money for a down payment in Canada?

Yes. Most lenders allow gifted down payments from immediate family members when properly documented.

What happens if I have a large deposit in my account?

The lender will usually request documentation showing the source of the funds before approving the mortgage.

Can I use RRSP funds for my down payment?

Yes. Eligible buyers can use the Home Buyers’ Plan to withdraw RRSP funds for a home purchase.

Can FHSA funds be used for a down payment?

Yes. First Home Savings Account funds can be used toward a down payment, provided eligibility and withdrawal requirements are met.

Final Thoughts

Down payment verification may seem like a small part of the mortgage process, but it’s one of the most common causes of underwriting delays. Providing complete documentation upfront can save days—or even weeks—during the approval process.

If you’re planning to purchase a home in Calgary or anywhere in Alberta, preparing your down payment documentation early can help ensure a smoother mortgage approval experience.

About Mark Herman

Mark Herman, MBA, is a Calgary mortgage broker with 22 years of experience helping home buyers, homeowners, and real estate investors secure financing throughout Alberta. His finance background and extensive lending experience help clients navigate complex mortgage requirements with confidence.

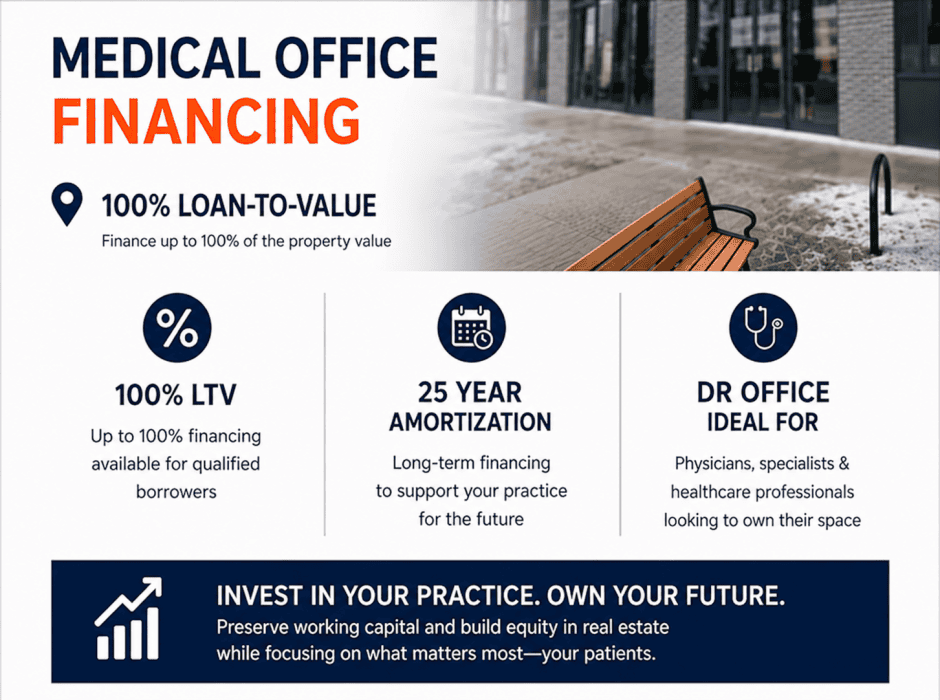

100% Medical Office Financing in Canada: How Physicians Can Buy a Clinic with No Down Payment

100% Medical Office Financing in Canada: How Physicians Can Buy a Clinic with No Down Payment

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience and an MBA in Finance, who still answers his own phone from 9 – 9 x 365.

Many physicians dream of owning their medical office instead of paying rent to a landlord. Yet one of the biggest obstacles is coming up with the down payment needed to purchase commercial real estate.

The good news is that some lenders offer 100% loan-to-value (LTV) financing for medical office purchases, allowing qualified healthcare professionals to acquire clinic space with little or no down payment.

If you’re a physician, specialist, dentist, veterinarian, optometrist, physiotherapist, or other healthcare professional, this financing option may allow you to preserve working capital while building long-term wealth through real estate ownership.

What Is 100% Medical Office Financing?

A 100% loan-to-value mortgage means the lender finances the entire purchase price of the property.

For example:

- Medical office purchase price: $1,000,000

- Down payment: $0

- Mortgage amount: $1,000,000

This differs from traditional commercial financing, which often requires a 20% to 35% down payment.

Medical professionals are viewed favorably by lenders because of their strong earning potential, stable professions, and historically low default rates.

Why Lenders Offer Special Programs for Physicians

Healthcare professionals represent a unique borrower category.

Many lenders recognize that physicians:

- Have stable and predictable income

- Operate businesses with recurring patient demand

- Typically maintain strong credit profiles

- Often require specialized medical facilities

- Benefit from long-term professional licensing

As a result, lenders may offer:

- Up to 100% financing

- Reduced down payment requirements

- Longer amortization periods

- Competitive commercial mortgage rates

- Flexible qualification criteria

Benefits of Owning Your Medical Office

Build Equity Instead of Paying Rent

Every mortgage payment helps increase your ownership stake in the property.

Over time, you may build significant equity through:

- Principal repayment

- Property appreciation

- Clinic growth

Preserve Working Capital

Many physicians prefer to keep cash available for:

- Equipment purchases

- Staff expansion

- Technology upgrades

- Marketing initiatives

- Practice acquisitions

100% financing can help preserve liquidity while still allowing property ownership.

Gain Control Over Your Space

Owning your building provides greater control over:

- Lease costs

- Renovations

- Expansion plans

- Signage

- Long-term occupancy expenses

Potential Retirement Asset

Commercial real estate often becomes an important component of a physician’s retirement and wealth-building strategy.

Some owners eventually:

- Lease space to other healthcare professionals

- Sell the practice while retaining the building

- Generate retirement income from rental revenue

Who Can Qualify for Medical Office Financing?

Programs vary by lender, but common eligible borrowers include:

Physicians

- Family physicians

- General practitioners

- Specialists

- Surgeons

Dental Professionals

- Dentists

- Orthodontists

- Oral surgeons

Other Healthcare Professionals

- Veterinarians

- Optometrists

- Chiropractors

- Physiotherapists

- Psychologists

- Pharmacists

- Nurse practitioners

Qualification depends on factors such as:

- Professional designation

- Credit history

- Practice financials

- Property type

- Debt service coverage

- Personal net worth

Medical Office Properties That May Qualify

Eligible properties often include:

- Medical clinics

- Professional medical buildings

- Dental offices

- Veterinary clinics

- Optometry clinics

- Mixed-use professional buildings

- Healthcare plazas

The property must generally be suitable for professional healthcare use.

Example: Purchasing a Medical Office

Assume a physician wishes to purchase a clinic valued at $1.5 million.

Traditional Commercial Financing

- Purchase Price: $1,500,000

- Down Payment (25%): $375,000

- Mortgage: $1,125,000

100% Medical Office Financing

- Purchase Price: $1,500,000

- Down Payment: $0

- Mortgage: $1,500,000

The physician preserves $375,000 that can remain invested in the practice or other opportunities.

Why a 25-Year Amortization Matters

Many medical office financing programs offer amortizations up to 25 years.

Benefits include:

- Lower monthly payments

- Improved cash flow

- Greater financial flexibility

- Increased funds available for practice growth

For healthcare professionals focused on expanding their practice, cash flow often matters more than rapid mortgage repayment.

Frequently Asked Questions

Can physicians really buy a medical office with no down payment?

Yes. Some lenders offer up to 100% financing for qualified healthcare professionals purchasing eligible medical office properties.

Are interest rates higher on 100% financing?

Not necessarily. Rates depend on the borrower, property, lender, and overall risk profile.

Can I purchase a building with multiple tenants?

Often yes. Many lenders will finance mixed-use professional buildings if a significant portion is occupied by healthcare-related tenants.

Is this available across Canada?

Programs are available in many provinces, including Alberta, British Columbia, Saskatchewan, Manitoba, Ontario, and other major markets, subject to lender guidelines.

Medical Office Financing Calculator Example

| Item | Amount |

|---|---|

| Purchase Price | $1,500,000 |

| Down Payment | $0 |

| Mortgage Amount | $1,500,000 |

| Amortization | 25 Years |

| Ownership Equity Built Through Principal Repayment | Yes |

| Capital Preserved for Practice Growth | $375,000+ |

Actual payments and qualification depend on lender guidelines and interest rates.

Why Work With a Commercial Mortgage Broker?

Medical office financing programs are often offered through specialized commercial lenders and healthcare-focused banking divisions.

Working with a commercial mortgage broker allows you to:

- Compare multiple lenders

- Access physician-specific programs

- Structure financing efficiently

- Preserve working capital

- Negotiate competitive terms

The right financing strategy can help you own your clinic sooner while keeping more cash available for your practice.

Ready to Explore 100% Medical Office Financing?

If you’re a physician or healthcare professional considering the purchase of a clinic, medical office, or professional healthcare building, there may be financing options available with little or no down payment.

Contact Mark Herman, MBA to discuss your goals and explore commercial mortgage solutions tailored to healthcare professionals.

Author Bio

Mark Herman, MBA is a mortgage broker with 22 years of experience helping professionals, business owners, and real estate investors secure financing across Canada. With an MBA in Finance, Mark specializes in complex mortgage solutions, commercial financing, and strategic lending for healthcare professionals.

Korean Mortgage in Canada Using Korean Income & Credit History | Calgary Mortgage Broker

Korean Home Buyers in Canada: Get a Mortgage Using Korean Income, Korean Tax Documents, and Korean Credit History

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience specializing in unique and difficult to do deals.

Buying a home in Canada can be challenging if you recently arrived from Korea or still earn most of your income there. Many (as in ALL) of the traditional Canadian lenders (Big6- banks) require extensive Canadian employment history, Canadian tax returns, and established Canadian credit.

The good news is that there are specialty lenders in Canada that understand the needs of Korean home buyers and can approve mortgages using Korean income, Korean employment documents, and even Korean credit reports.

If you’re a Korean citizen, permanent resident, or newcomer to Canada, this specialized mortgage program may help you qualify sooner than you think.

Can I Get a Canadian Mortgage Using Korean Income?

Yes!!

Certain specialty lenders in Canada work specifically with Korean borrowers and can evaluate income earned in Korea. Instead of relying solely on Canadian tax returns and Canadian employment history, these lenders can review:

- Korean tax documents

- Korean employment verification

- Korean pay records

- Korean credit reports

- Korean property ownership documents

This can be especially valuable for:

- New immigrants from Korea

- Permanent residents who recently moved to Canada

- Families with income earned in Korea

- Professionals working for Korean companies

- Individuals relocating to Calgary or other Canadian cities

“Our Korean customers were just as surprised as I was when we found that we can do a mortgage for them, in Canada, using their existing documents from Korea!”

Mortgage Mark Herman, MBA mortgage broker in Calgary specializing in new buyers from Korea

What Documents Are Required?

For Husband and Wife Applicants

The lender typically requires:

Income Verification

2024 and 2025 Certificate of Income from the National Tax Service of Korea (국세청)

These documents help verify historical income earned in Korea.

Employment Verification

Letter of Employment (재직증명서)

The employment letter confirms position, employment status, and employer information.

Income Evidence

- Most recent three pay stubs (급여명세서)

- Three months of direct deposit history

These documents help confirm current earnings and consistency of income.

Existing Property Information

If the applicants own property in Korea:

- Current mortgage statement

- Property tax statement

These documents allow the lender to calculate any existing debt obligations.

For Adult Children Who May Be Co-Signing or On the Mortgage

If an adult child is participating in the application, lenders may require:

- Letter of employment

- Recent pay stubs

- Three months of direct deposit history

- Most recent Notice of Assessment (NOA)

- Proof of no tax owing

Identification Requirements

- Passport

- Driver’s license

- Korean Passport

- Canadian Permanent Resident Card

- Korean Resident Registration Card (주민등록증)

Korean Credit Report

One unique feature of this program is that the lender can often obtain and review a Korean credit report directly.

Applicants will generally be required to sign a credit consent form authorizing the Korean credit search.

How Does the Lender Calculate Foreign Income?

The lender uses a specific formula to determine qualifying income:

Foreign Income = (Gross Foreign Income – Foreign Debt Service) × Recognition Ratio (80%) × Exchange Rate

This means:

- Gross Korean income is reviewed.

- Existing debt obligations are deducted.

- The lender recognizes 80% of the remaining income.

- The income is converted to Canadian dollars using the applicable exchange rate.

Example of Foreign Income Qualification

Let’s assume:

- Annual Korean income: CAD equivalent of $150,000

- Existing Korean debt payments: $20,000 annually

Calculation:

- $150,000 − $20,000 = $130,000

- $130,000 × 80% = $104,000 qualifying income

In this example, the lender would use approximately $104,000 of qualifying income for mortgage approval purposes.

104k income gets about a $425,000 mortgage amount (+ down payment = purchase price)

Important Translation Requirements

All Korean documents must be accompanied by English translations.

Applicants should submit:

- Original Korean documents

- Certified English translations

Providing complete translations early in the process can help avoid delays and speed up approval.

Conditions of Financing Needs to be 14 Days.

This mortgage program requires additional underwriting compared to a standard Canadian mortgage.

Borrowers should allow approximately two weeks for the lender to review the Certificate of Income documents and complete the approval process.

If you are planning to purchase a home, it is important to start the mortgage application early so financing is ready before you remove conditions.

Why Work With a Mortgage Broker Familiar With Korean Mortgage Programs?

Not every mortgage broker understands foreign-income lending or Korean documentation requirements.

An experienced broker can help:

- Review Korean income documents

- Coordinate English translations

- Calculate qualifying income accurately

- Structure the application properly

- Navigate specialty lender requirements

- Avoid unnecessary delays

For Korean families buying property in Calgary and throughout Canada, working with a broker who understands these programs can significantly improve the approval process.

Frequently Asked Questions

Can I qualify for a mortgage in Canada without Canadian income?

Yes. Some specialty lenders can use Korean income and Korean employment documents to qualify borrowers.

Can a lender use my Korean credit report?

Yes. Certain lenders can obtain and review Korean credit reports with your written authorization.

Do my Korean documents need to be translated?

Yes. All Korean documents must be submitted with English translations.

How long does approval take?

Borrowers should generally allow at least two weeks for the lender to review foreign income documentation and issue approval.

Can permanent residents use this program?

Yes. Permanent residents with Korean income may qualify, depending on the lender’s guidelines.

Final Thoughts

Many Korean families assume they must wait years to build Canadian credit and employment history before buying a home.

In reality, some Canadian lenders can use Korean tax documents, Korean employment records, Korean income, and Korean credit history to help qualified borrowers purchase a home much sooner.

If you’re a Korean citizen, newcomer, or permanent resident looking to buy property in Calgary or anywhere in Canada, exploring these specialized mortgage programs could open the door to homeownership sooner than expected.

Author Bio

Mark Herman, MBA is a Calgary mortgage broker with 22 years of experience helping Canadians, newcomers, business owners, and foreign-income borrowers secure mortgage financing. With an MBA in Finance, Mark specializes in finding mortgage solutions that traditional lenders often overlook, including programs for international buyers and families with foreign income.