USA Rental Mortgage for Canadians | U.S. Rental Property Financing

New U.S. Rental Property Financing for Canadians

By Mortgage Mark Herman, a broker with and MBA in Finance and 23 years of mortgage experience under his Stampede belt.

Canadian investors purchasing or refinancing rental properties in the United States often run into a major problem: traditional mortgage rules do not always fit the way investors actually earn, report, or structure their income.

That is especially true for self-employed Canadians, real estate investors with multiple properties, borrowers using corporations, or buyers who do not have U.S. credit history.

That is why the launch of USA Rental Mortgage for Canadians is such an important development.

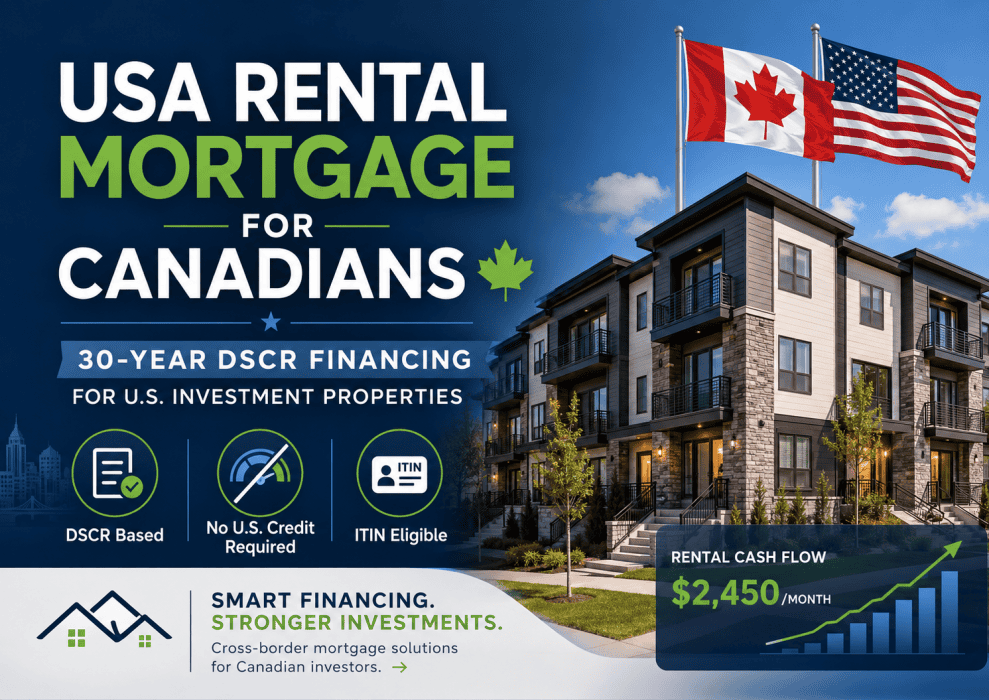

USA Rental Mortgage for Canadians is a new financing solution designed specifically for Canadian investors purchasing or refinancing U.S. investment properties. It is a 30-year DSCR first mortgage, meaning the mortgage is primarily qualified based on the property’s rental income, not the borrower’s personal income.

In simple terms: if the property cash flows, there may be a financing solution.

What Is a DSCR Mortgage?

DSCR stands for Debt Service Coverage Ratio.

Instead of focusing primarily on the borrower’s employment income, tax returns, paystubs, or traditional debt ratios, a DSCR mortgage looks at whether the rental income from the property can support the mortgage payment.

For Canadian investors buying in the U.S., this can make a major difference.

Many of the issues that traditionally derail investment-property financing may not apply in the same way, including:

- Complex personal income

- Self-employed income

- Limited income documentation

- No U.S. employment income

- No W-2 income

- No U.S. Social Security Number

- Limited or no U.S. credit history

This makes DSCR financing especially attractive for investors who are focused on the strength of the property itself.

Why USA Rental Mortgage for Canadians Stands Out

USA Rental Mortgage for Canadians is designed around the needs of Canadian real estate investors who want to buy or refinance U.S. rental properties.

The program offers expanded flexibility compared with many traditional U.S. mortgage options.

1. Qualified on the Property’s Cash Flow

One of the biggest advantages of this program is that qualification is based on the rental property’s cash flow.

That means:

- DSCR-based qualification

- No income documentation required

- No-Ratio options available

- Sub-1.0 DSCR options available

This can be especially useful when a strong investment property does not fit traditional personal-income lending rules.

2. No U.S. Credit Required in Some Cases

Many Canadian investors do not have deep U.S. credit profiles. That can be a barrier with traditional financing.

USA Rental Mortgage for Canadians helps reduce that barrier.

Program features may include:

- No minimum beacon score at 70% loan-to-value

- Foreign credit accepted

- ITIN borrowers eligible

- No SSN required

- No W-2 required

For Canadians investing across the border, this can be a major advantage.

3. Expanded ITIN Program

The expanded ITIN program opens financing to a large and underserved group of investors.

Eligible borrowers may be able to access:

- Up to 80% loan-to-value

- No Social Security Number required

- ITIN-based qualification options

This creates more flexibility for Canadian investors who want to own U.S. rental real estate but do not have traditional U.S. borrower documentation.

4. Broad Property Eligibility

USA Rental Mortgage for Canadians is not limited to one narrow type of rental property.

Eligible property types may include:

- 1–8 unit residential properties

- Condotels

- Short-term rental properties

- Purchase transactions

- Cash-out refinance transactions

- Properties owned through an LLC

This is especially useful for investors looking at vacation rentals, short-term rentals, multi-unit properties, or refinancing existing U.S. investment properties.

5. Competitive Financing Options

The program also offers competitive financing terms for qualifying properties.

Current program highlights include:

- Rates from approximately 6.99%

- 30-year term

- Loan amounts from $200,000 to $3,000,000

- Nationwide U.S. coverage, with limited state exclusions

- Purchase and cash-out refinance options

Exact terms will depend on the property, location, borrower profile, loan-to-value, DSCR, and overall file strength.

Who Could This Program Help?

This program may be a fit for Canadian investors who are:

- Buying a U.S. rental property

- Refinancing an existing U.S. investment property

- Pulling cash out of a U.S. rental

- Buying a short-term rental or vacation rental

- Purchasing through an LLC

- Self-employed

- Reporting income in a way that does not fit traditional mortgage rules

- Lacking U.S. credit history

- Using ITIN-based documentation

- Looking for a 30-year rental-property mortgage

For Calgary and Alberta investors looking beyond the Canadian market, U.S. rental-property financing can be complicated. The right program can make the difference between a strong investment opportunity moving forward or falling apart because of documentation rules.

A Simple Opportunity for Canadian Investors

The core idea behind USA Rental Mortgage for Canadians is simple:

If the property cash flows, there is likely a solution.

That does not mean every property or borrower will automatically qualify, but it does mean Canadian investors may have more options than they realize.

For investors who have been told they cannot qualify because of income documentation, U.S. credit history, W-2 income, SSN requirements, or traditional mortgage ratios, this program may be worth reviewing.

Talk to a Mortgage Broker Before You Buy

Before making an offer on a U.S. rental property, it is important to understand the financing rules upfront.

The property type, rental income, state, loan amount, down payment, ownership structure, and documentation all matter.

A proper review before writing an offer can help avoid problems later.

After 22 years in mortgages, Katie and I have seen how important it is to structure the financing properly from the beginning — especially with cross-border investment properties.

If you are a Canadian investor looking at a U.S. rental property, we can help review the numbers and determine whether this type of financing may work.

Mortgage Mark Herman

Calgary Mortgage Broker

403-681-4376

FAQ: USA Rental Mortgage for Canadians

Can Canadians get a mortgage for a U.S. rental property?

Yes. Canadian investors may be able to finance U.S. rental properties through specialized programs such as USA Rental Mortgage for Canadians, depending on the property, rental income, loan-to-value, documentation, and location.

What is a DSCR mortgage?

A DSCR mortgage qualifies the borrower based primarily on the property’s rental income and cash flow, rather than traditional personal income documentation.

Do I need U.S. credit to qualify?

Not always. This program may allow foreign credit, and in some cases there may be no minimum beacon score at 70% loan-to-value.

Do I need a U.S. Social Security Number?

No. ITIN borrowers may be eligible, and the program may not require a U.S. Social Security Number or W-2 income.

Can I use this for short-term rentals?

Yes. Short-term rental properties may be eligible, depending on the full details of the file.

Can I buy through an LLC?

Yes. Ownership through an LLC may be permitted.

What loan amounts are available?

Loan amounts may range from $200,000 to $3,000,000, depending on the file.

What rate is available?

Rates are currently from approximately 6.99%, depending on the property, borrower, loan-to-value, DSCR, and overall file details.