Buying a Home With Poly B Plumbing in Alberta (2026 Guide)

Buying a Home in Alberta With Poly B Plumbing (2026 Guide for Buyers & Sellers)

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

Buying a home with Poly B plumbing in Alberta can feel like a deal-breaker—but it doesn’t have to be. The reality is that thousands of homes in Calgary and across Alberta still have Poly B, and many are financed every year.

The key is understanding the risks, how lenders and insurers view it, and how to structure your purchase properly.

What Is Poly B Plumbing?

Poly B (polybutylene) is a grey plastic piping used in homes built roughly between 1978 and the mid-1990s.

It was popular because it was:

- Cheap

- Easy to install

- Flexible

Unfortunately, it turned out to have serious long-term reliability issues.

There are still hundreds of thousands of homes across Canada with Poly B, especially in Alberta.

Why Poly B Plumbing Is a Problem

Poly B isn’t just “older plumbing”—it’s considered high-risk plumbing.

Key issues:

- Internal deterioration from chlorine in water

- Brittle pipes that crack over time

- Leaks that start inside walls (hard to detect)

- Sudden pipe failures without warning

In Alberta, the problem can be worse due to:

- Temperature swings

- Water chemistry

- Aging housing stock

This combination leads to:

- Water damage

- Mold issues

- Expensive repairs

How to Tell If a Home Has Poly B

Look for:

- Grey (sometimes blue/black/white) plastic pipes

- Markings like “PB2110”

- Visible piping near:

- Hot water tank

- Basement ceiling

- Under sinks

If the home was built between 1980–1995, there’s a strong chance it has Poly B.

Can You Get a Mortgage on a Home With Poly B in Calgary Alberta?

Yes—but it depends on the lender and the overall deal.

Most lenders will:

- Still approve the mortgage

- Focus more on:

- Property value

- Down payment

- Borrower strength

However…

The real issue is insurance (not the mortgage)

The Insurance Problem (This Is What Actually Kills Deals)

Insurance companies are the biggest hurdle.

Many insurers:

- Refuse coverage entirely

- Require full replacement before closing

- Or charge higher premiums

Without insurance, your mortgage cannot fund. SURPRISE – we DO have access to insurance companies that will cover Poly B at normal rates!

This is the #1 reason Poly B deals fall apart.

Typical Solutions for Buyers

1. Replace Poly B Before Closing

- Seller completes replacement

- Cleanest solution for financing

- Helps protect property value

2. Negotiate a Price Reduction

- Buyer takes on replacement cost

- Common in Calgary market

- Requires lender + insurer alignment

3. Insurance Exception Strategy

- Some insurers still accept Poly B (case-by-case)

- Often requires:

- Inspection

- No existing leaks

How Much Does It Cost to Replace Poly B?

Typical cost range:

- $3,000 to $25,000+ depending on home size

Factors:

- Square footage

- Accessibility

- Whether walls need repair afterward

Most homeowners replace with:

- PEX

- Copper

Does Poly B Affect Home Value in Alberta?

Yes—but not always dramatically.

What happens in the market:

- Buyers use it as a negotiation tool

- Some walk away entirely

- Others expect a discount

In practice:

- Homes still sell

- But usually with pricing adjustments

Should You Buy a Home With Poly B?

It depends on your situation.

You should consider it if:

- The price reflects the risk

- You have a plan to replace it

- Insurance is confirmed upfront

You should avoid it if:

- Insurance is unclear

- Budget is tight

- You want a “turnkey” home

Mortgage Strategy Tips (This Is Where You Win or Lose the Deal)

As a mortgage broker, this is where I see deals succeed—or fail.

Key strategies:

- Confirm insurance FIRST (before removing conditions)

- Work with a broker who understands:

- Lender flexibility

- Insurance workarounds

- Budget replacement into your financing plan

Real Example (Calgary Scenario)

Purchase price: $500,000

Poly B replacement estimate: $12,000

Negotiation:

- Buyer reduces offer to $488,000

- Uses savings to replace plumbing after closing

Result:

- Deal goes through

- Property value protected long-term

Bottom Line

Poly B isn’t a deal killer—but it is a strategy issue.

Handled correctly:

- You can buy below market value

- Upgrade the home

- Build equity quickly

Handled poorly:

- The deal collapses due to insurance

FAQ (Featured Snippet Section)

Is Poly B plumbing illegal in Alberta?

No, but it is no longer used in new construction and is considered outdated and high-risk.

Can you insure a home with Poly B?

Sometimes—but many insurers restrict or refuse coverage.

Do lenders allow Poly B homes?

Yes. The bigger issue is insurance approval, not the mortgage.

Should I replace Poly B immediately?

Most experts recommend replacement due to unpredictable failure risk.

Final Advice

If you’re considering buying a home with Poly B, don’t guess.

This is one of those situations where:

- The right mortgage strategy saves the deal

- The wrong approach kills it

Author Bio

Mark Herman is a Calgary-based mortgage broker with 22 years of experience and an MBA in Finance. He specializes in helping home buyers navigate complex mortgage situations—including properties with Poly B plumbing, rental income, and non-traditional borrowers.

Divorce and Mortgage Options in Calgary: What to Know Before You Sign

Divorce and Mortgages in Canada: What You Need to Know Before Signing a Separation Agreement

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience, specializing in complicated and standard divorces in Alberta and BC.

Divorce is one of the most stressful financial events you’ll go through. Emotions are high, timelines are tight, and most people just want to get things settled and move on.

But here’s the mistake I see all the time:

People sign separation agreements that unintentionally destroy their ability to qualify for a mortgage afterward.

And by the time they find out—it’s too late. And that is why we have lawyers that send us their drafts of separation agreements so we can ensure that both parties can still buy a home after the agreement is signed.

Why Your Separation Agreement Matters More Than You Think

In Calgary, I regularly get calls from divorce lawyers before agreements are finalized.

Why?

Because experienced lawyers understand something critical:

Just because a separation agreement is legally “fair” doesn’t mean it works from a mortgage perspective.

They want to make sure:

-

Both parties can qualify for financing afterward

-

Support payments aren’t structured in a way that kills borrowing power

-

Debt division doesn’t create unintended consequences

That’s the right approach.

Unfortunately, many people don’t have that conversation until after everything is signed.

Your Mortgage Options During Divorce

Most situations fall into one of four scenarios.

Most people want to do #4, keep the home, increase the mortgage to buy out the ex-partner.

| Scenario | Scenario #1 | Scenario #2 | Scenario #3 | Scenario #4 |

|---|---|---|---|---|

| Overview | Sell your home, no new property | Sell your home, buy another home | Hold onto your home, keep mortgage same | Hold onto your home, increase mortgage |

| What will you do with the existing house? | Sell and not buy another property | Sell and buy another property | Keep | Keep |

| Do you need to take out home equity? | Not applicable | Not applicable | No, sufficient cash to buy out spouse | Yes, need to tap equity to buy out spouse |

| What will happen to your current mortgage? | Pay out existing mortgage | Pay out existing mortgage or port mortgage | Assume or transfer existing mortgage | Refinance existing mortgage |

| Do you need a new mortgage? | No | Yes (unless porting) | No | No (but mortgage increases) |

| Do you need to re-qualify for a mortgage? | Not applicable | Yes | Yes | Yes |

Breaking Down the 4 Common Scenarios

1. Sell the Home and Don’t Buy Again (Yet)

This is the cleanest option financially.

-

Mortgage gets paid out

-

No re-qualification needed

-

You walk away with your share of equity

This works well if you want a reset—but it delays re-entering the market.

2. Sell and Buy Another Home

This is what most people want to do.

But here’s the catch:

You have to fully re-qualify on your own.

That means:

-

Your income must support the new mortgage

-

Any support payments (paid or received) are factored in

-

Debts from the separation count against you

This is where a lot of deals fall apart.

3. Keep the Home and Take Over the Existing Mortgage

This sounds simple—but it’s not automatic.

Even if the lender allows a transfer:

-

You still need to qualify on your own

-

The other spouse must be fully removed from liability

If you can qualify, this is often the least disruptive option.

4. Keep the Home and Refinance (Buy Out Your Ex) – what you probably want to do.

This is very common in Calgary.

You:

-

Refinance the mortgage

-

Pull out equity

-

Use it to buy out your spouse and pay out debts that may also be involved.

But this increases your mortgage balance—and your payment.

So again, you must qualify at the higher amount.

The Biggest Mistake I See (And It’s Costly)

Here’s the real issue:

Someone agrees to:

-

High support payments

-

Taking on too much debt

-

Or an aggressive buyout structure

Then they come to me after the agreement is signed…

…and they can’t qualify for a mortgage anymore.

Not for the home they wanted.

Sometimes not for any home.

How Support Payments Affect Mortgage Approval

This is where things get technical.

If you pay support:

-

It reduces your borrowing power directly

If you receive support:

-

It may help—but only if it’s structured properly

-

Lenders often require consistency and documentation

Not all support income is treated equally.

Why Divorce Lawyers Call Me Before Agreements Are Signed

The better family lawyers in Calgary will loop in a mortgage broker early.

They want to avoid:

-

Structuring payments that make financing impossible

-

Creating agreements that look good on paper but fail in reality

-

Clients getting stuck renting long-term unintentionally

It’s a small step that prevents major problems later.

What You Should Do Before Signing Anything

If you’re going through a separation, do this before finalizing your agreement:

1. Get a Mortgage Feasibility Check

Find out:

-

What you can qualify for today

-

What different scenarios look like

2. Run Multiple Scenarios

Don’t assume one outcome.

Look at:

-

Keeping the home

-

Selling and buying

-

Different support structures

3. Coordinate With Your Lawyer

Your mortgage plan and legal agreement should work together—not against each other.

Calgary-Specific Considerations

In Calgary, this matters even more because:

-

Home prices are still relatively accessible compared to other major cities

-

Many people can buy again—if the structure is right

-

But small changes in income or obligations can make or break approval

Final Thoughts

Divorce is emotional—but your mortgage decisions are purely financial.

And once a separation agreement is signed, you don’t get a do-over.

If you’re in this situation, the best move you can make is simple:

Talk to a mortgage broker before you sign anything.

FAQ: Divorce and Mortgages in Canada

Can I get a mortgage after a divorce?

Yes—but you must qualify on your own, and your separation agreement plays a major role.

Can I keep the house after divorce?

Only if you can qualify for the mortgage independently or refinance to remove your ex.

Do support payments affect mortgage approval?

Yes. Paying support reduces borrowing power; receiving support may help depending on how it’s structured.

Do I need to refinance to remove my spouse?

Often yes, unless the lender allows a transfer and you qualify on your own.

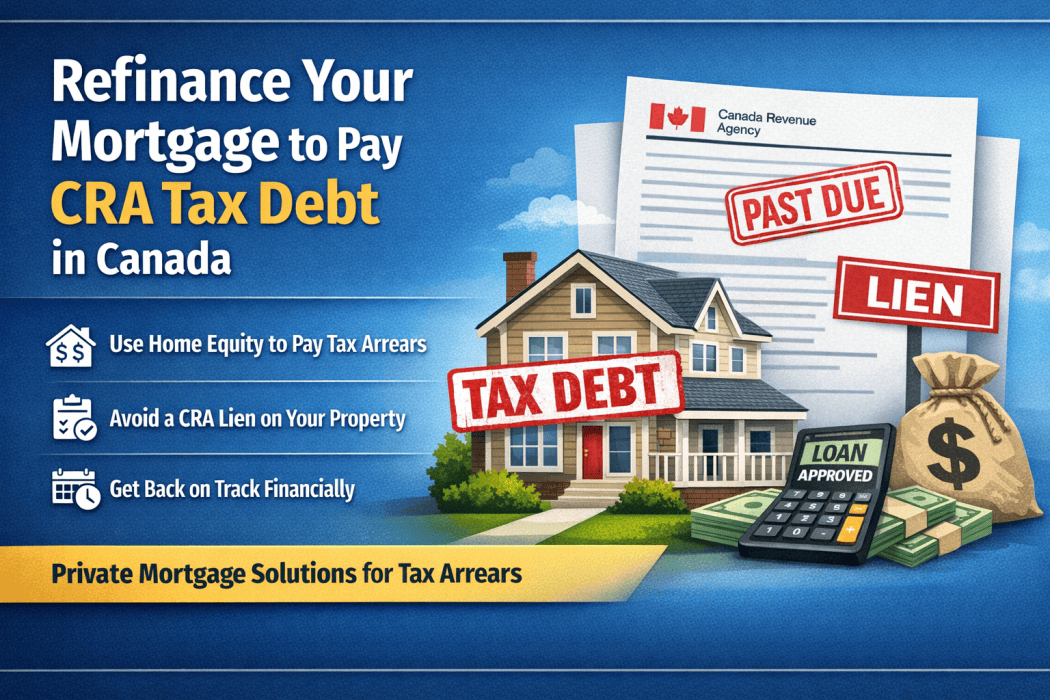

Can I Use a Mortgage to Pay CRA Tax Debt in Canada? (A Real Example of a Private Refinance)

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience specializing in new home buyers and tough deals.

Many Calgary and Canadian homeowners are surprised to learn that the CRA can place a lien on their home for unpaid taxes. Once that happens, refinancing becomes much harder.

The good news is that homeowners with equity often still have options. In many cases, a private mortgage refinance can be used to pay CRA tax debt, remove the lien risk, and give you time to get your finances back on track.

Below is a real example of how this works.

Real Example: Refinancing to Pay $29,000 in CRA Tax Debt

A self-employed homeowner recently contacted me about refinancing their mortgage to deal with back taxes owed to the Canada Revenue Agency (CRA).

Here was the situation:

Business tax situation

-

Business filings completed up to Oct 2022 – Sept 2023

-

Currently working with an accountant to file Oct 2023 – Sept 2024

-

Next filing period 2024–2025 still pending

-

GST paid up to end of 2024

-

GST may still be owing but amount unknown until filings are complete

Income structure

-

Owner pays themselves from the business when income comes in

-

No dividends issued

-

Most tax liability flows to personal taxes

Personal tax situation

-

Approximately $29,000 in personal tax debt to CRA

CRA had indicated they may place a lien on the property, which would make financing much more difficult.

The homeowner didn’t currently have the cash to pay the taxes, and they were also trying to pay their accountant to complete outstanding business filings.

Why CRA Debt Is a Problem for Mortgage Lenders

Most traditional lenders (banks and credit unions) require that CRA debt be fully paid before they approve a mortgage refinance.

They want to ensure:

-

There is no CRA lien registered

-

All tax filings are up to date

-

There are no outstanding collection issues

If these conditions are not met, the bank will usually decline the mortgage.

How a Private Mortgage Can Solve the Problem

In situations like this, a private lender refinance can be used to:

-

Pay off the CRA tax debt

-

Prevent or remove a CRA lien

-

Provide time to complete tax filings

-

Stabilize finances before returning to a traditional lender

Private lenders focus primarily on:

-

Equity in the property

-

Property value

-

Exit strategy (how the loan will be repaid or refinanced later)

They are often much more flexible when dealing with self-employed borrowers or tax arrears.

Typical Structure of a CRA Tax Debt Refinance

A refinance for tax debt usually works like this:

Step 1 – Property appraisal

The lender confirms the home’s value and available equity.

Step 2 – Mortgage approval

A private lender approves a mortgage based on the equity position.

Step 3 – CRA payout

Funds from the refinance are used to pay CRA directly.

Step 4 – Short-term mortgage

The homeowner keeps the private mortgage for 12–24 months while fixing their tax situation.

Why Acting Before a CRA Lien Matters

Timing is critical.

If CRA registers a tax lien on your property, refinancing becomes significantly more complicated because:

-

The lien must be paid during the refinance

-

Some lenders refuse to fund if the lien is already registered

-

Legal costs can increase

Getting financing before the lien is registered gives homeowners far more options.

Who This Strategy Works Best For

Using a private mortgage to pay CRA debt can work well if you:

-

Own a home with significant equity

-

Are self-employed

-

Have unfiled taxes that are being completed

-

Need time to catch up financially

This strategy is common for:

-

Business owners

-

Contractors

-

Real estate investors

-

Commission-based professionals

The Exit Plan: Moving Back to a Traditional Mortgage

Private mortgages are usually short-term solutions.

During the term, the goal is to:

-

Complete all tax filings

-

Pay CRA balances

-

Improve income documentation

-

Refinance into a lower-rate bank mortgage

Featured Snippet – Q&A Section

Frequently Asked Questions About CRA Tax Debt and Mortgages

Can you refinance your home to pay CRA tax debt in Canada?

Yes. Homeowners with sufficient equity can often refinance their mortgage to pay CRA tax debt. If traditional lenders will not approve the refinance, a private mortgage lender may still provide financing based on the home’s equity.

Can CRA put a lien on your house for unpaid taxes?

Yes. The Canada Revenue Agency can register a tax lien against your property if taxes remain unpaid. Once registered, the lien attaches to your home and must usually be paid before selling or refinancing.

How much equity do I need to refinance to pay tax debt?

Most private lenders will allow refinancing up to approximately 75–80% of the home’s value, depending on the situation and property location.

Will banks refinance if I owe CRA money?

Most banks require that CRA debts be paid first and tax filings be up to date. If taxes are still outstanding, homeowners often need to use a short-term private mortgage to pay CRA and then refinance with a bank later.

Mortgage Example Calculator Section

Example: Using a Mortgage Refinance to Pay CRA Tax Debt

Let’s look at a simplified example.

Home Value: $700,000

Current Mortgage: $420,000

Maximum Refinance at 80%: $560,000

Potential equity available:

$560,000 – $420,000 = $140,000 available

If the homeowner owes $29,000 in CRA taxes, they could refinance and:

-

Pay the CRA debt in full

-

Cover legal and appraisal costs

-

Possibly consolidate other high-interest debts

This type of refinance is commonly used as a temporary strategy, allowing the homeowner to clean up their tax situation before moving back to a traditional lender.

Frequently Asked Questions

Can CRA force the sale of my home?

Yes, in extreme cases CRA can pursue legal action that could eventually lead to the forced sale of property.

However, most homeowners resolve the issue by paying the tax debt through refinancing.

Can I get a mortgage if my taxes aren’t filed?

Traditional lenders usually require all tax filings to be current.

Private lenders may still consider the mortgage if:

-

You are actively working with an accountant

-

The property has enough equity.

How much equity do I need to refinance CRA debt?

Most private lenders require the mortgage to stay below about 75–80% of the home’s value, although this varies.

Final Thoughts

Tax debt with CRA is stressful, especially for self-employed homeowners. But if you own property with equity, a private mortgage refinance can provide a solution to clear the debt and buy time to get your finances organized.

The key is acting early — before CRA registers a lien on your home.

Author Bio

Mark Herman, MBA is a mortgage broker with 22 years of experience helping homeowners across Canada solve complex financing situations, including tax debt, private mortgages, and self-employed income challenges.

Thinking twice when handing your mortgage over to a bank adviser

Great story below of a recent Scotiabank advisor messing up a deal so bad that it ended up disqualifying a buyer from getting a special at 3.69% insured mortgage when market rates are 4.45%.

Bank advisors mess up all the time and I hear about it all the time. Maybe 15% of our deals get to us from bank mess ups.

In the story cut and paste below these buyers just would have ended up with a a higher rate but their deal wold still work… this one caused a 1 year delay.

Let me tell you a mortgage story…

We had a customer that we helped sheppard past 3 or 4 fiery hoops getting his mortgage ready for approval with a bumpy past we were smoothing over. Then 1 day he calls and says a met a bank mortgage rep at a gas station, that bank rep “guaranteed” him getting approved so our customer applied and … surprise – worse than a decline, CMHC declined him.

CMHC was the only lender that would do his specific deal, for the mess he was in, and/ but CMHC NEVER forgets – anything. All the insurers retain all data for ever. So he now had to wait another 12 months to get insurer approval. The delay in the end was 12 additional months that he had to wait before he could buy.

So … Think twice before handing over your mortgage to a bank adviser

Mark Herman, Best mortgage broker in Calgary Alberta for new home buyers.

Opinion: Think twice before handing your mortgage to a bank adviser – CMT News

Written by Ross Taylor, Mortgage Strategies, Opinion,

Let me tell you a story.

Recently, a major chartered bank ran a very competitive promotion: 3-year fixed rates at 3.69% for insured files and 3.99% for conventional files. Needless to say, these rates were popular, business was booming, both for the bank and for brokers working with them.

We had pre-approved a young couple earlier in the year, but when it came time to seek approval on a home they had made a successful offer on, they first went directly to their local branch to withdraw funds from their First Home Savings Account (FHSA).

When a branch adviser steps in

During that visit, the branch financial adviser offered to handle their mortgage as well. He convinced them there was no need to come back to our team, he had it all under control.

They also explored options at another bank, but the rates they were offered were mediocre. Our promo was still the best rate in town.

The deal gets declined, and there’s no second chance

But here’s the twist. After the financial adviser submitted their deal, it was declined. He escalated the deal to senior management, but again was given a firm no.

When they came back to us and told me the news, I was shocked. I couldn’t understand why they were declined. On paper, this was a strong file. Solid income, great credit, and their debt service ratios were within reasonable bounds.

Misinterpreting income cost them the deal

I asked if they were told why they were turned down, and they said, “because our debt service ratios were over the 39/44 limit.”

Now, their pay stubs were a bit complicated, I’ll give you that. But we had their T4s, and I could easily make a case for either using a two-year average or taking their current full-time salary. Both would have worked. You just had to know how to interpret the documentation properly.

I contacted our Business Relationship Manager at the bank and asked if I could re-submit the file. After all, it had been declined, and I felt confident we could get it approved with the correct interpretation of income. But the answer was a firm no.

Why bank policy closed the door

The bank’s position was that I wouldn’t want another broker or branch employee taking one of our approved files and trying to submit it again. And while I understand the sentiment, this wasn’t the same thing. This wasn’t poaching a win, it was salvaging a decline.

But rules are rules, and because the file had already been escalated and declined by the branch, there was no path forward for me to resubmit it — even if I knew how to fix it.

What’s the lesson here? Be careful who you trust with your mortgage

This story isn’t about one bank being better than another. It’s about understanding that not all mortgage advisers are created equal. When you walk into a branch, you’re often speaking to a generalist. They might have good intentions, but they don’t always have the same level of mortgage-specific training or experience as a full-time mortgage broker.

And the consequences of that can be enormous. In this case, the clients lost out on a great rate and had to start over, simply because it seems their adviser didn’t fully understand how to package their income. And once the file was declined, there was likely no second chance.

The bottom line

Mortgages are complex, especially if your income is even slightly non-standard. Getting declined not only wastes time, it can actually prevent you from accessing the best deals, even if you’re fully qualified. Before you hand over your file to someone behind a desk at your local branch, ask yourself: do they really specialize in mortgages?

Because once a file is escalated and declined at the bank level, it may close off options you didn’t even know you had.

Make sure you’re putting the biggest financial transaction of your life in the right hands.

Canadian Mortgage with American Income, 2025

Yes, that headline is true!!

August 15, 2025

We finally have an “A lender” in the Canadian mortgage broker space that will allow a buyer’s USA/ American income to be used.

Quick summary of the details.

- 30% down

- 80% of USA salary to be used, income based on USA tax docs

- Almost any standard residential property in Canada

- “A lender,” at A rates, no lender fee, no broker fee, underwritten the same as all Canadian mortgages

- No funny business here. This is a normal mortgage, that you would want. The same as what expect from any of the Big-6 banks in Canada.

For more data or to ask about a deal, contact Mortgage Mark Herman, on his cell phone. He usually answers his own phone; from 9 am to 9 pm MST daily.

Data points below summarize key criteria and parameters for an “A-lender” in the Canadian mortgage broker channel that accepts US income.

Borrower Eligibility

- Citizenship: any (US, Canadian, or other)

- Canadian residency: no minimum length of stay required

- Tax history: two consecutive years of US tax filings (no CRA filings needed – its true!)

Income Documentation

- W-2 forms (equivalent to Canadian T4 slips)

- IRS Form 1040 (equivalent to Canadian T1 returns)

- US Tax Return Transcripts or Notices of Assessment (NOA – Notice of Assessment)

- All documents must cover the most recent two-year period

Income & Loan Parameters

- Income recognized: up to 80% of gross US salary

- Income types accepted: salary only (sorry, the bank can’t use fee-for-service, or self-employed/ BFS income)

- Maximum loan-to-value ratio (LTV): 70%, means 30% down payment

- Credit underwriting conforms to Canadian mortgage regulations

Property Types

- Primary residence

- 2nd home / Secondary or vacation home and even…

- Rental or investment property

Notes

- No requirement for employer size, industry, or Canadian work history

- Simplified process: bypass CRA income filings entirely

- Ideal for US-based clients relocating, investing, or holding dual residences

We used to run into a few of these deals ever year, and now we see one every month so we found a lender that can do this business for our realtor partners.

The buyers only need 30% down, and the bank will use 80% of their USA salary as the income.

Mark Herman, top Calgary Alberta and Vancouver Island mortgage broker

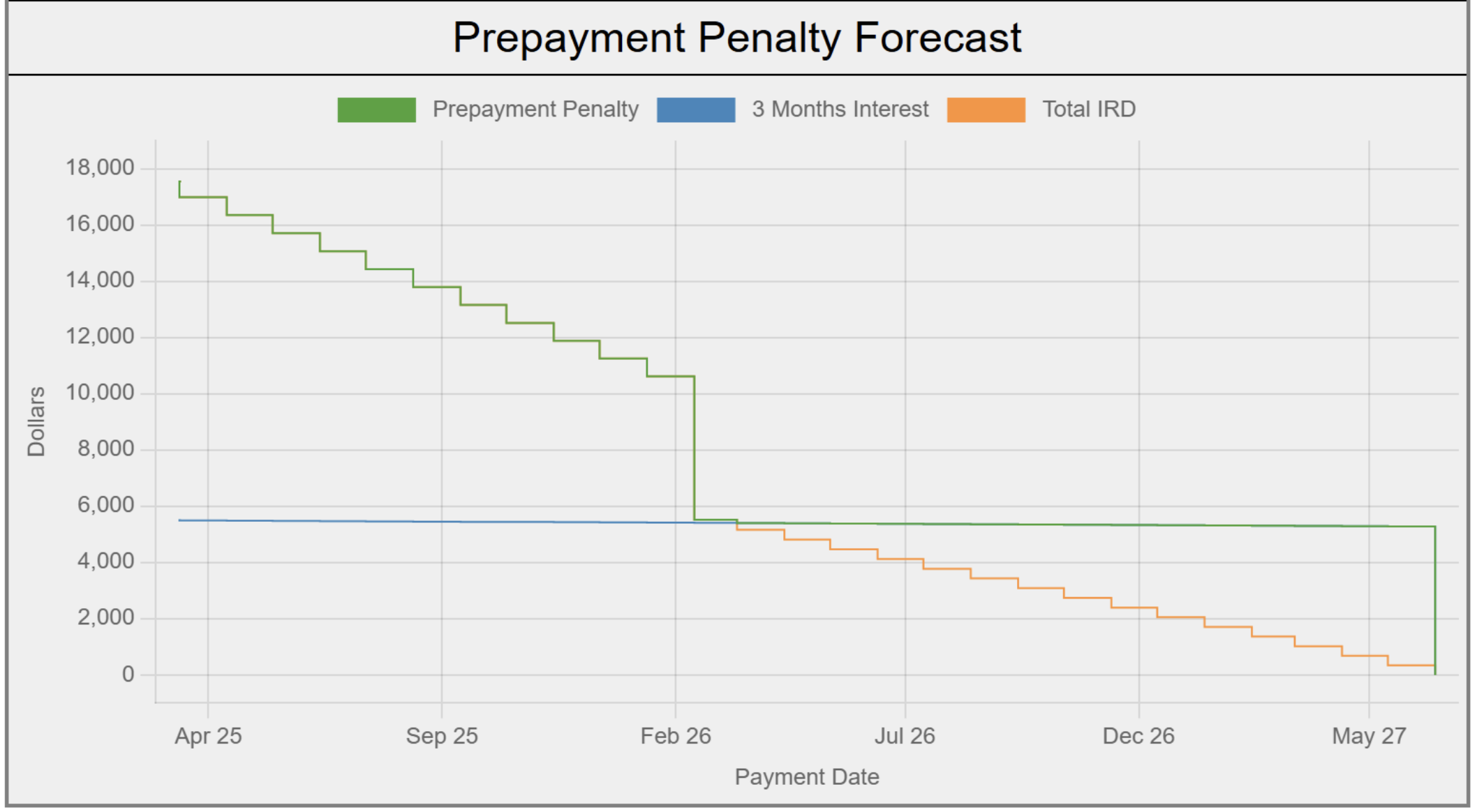

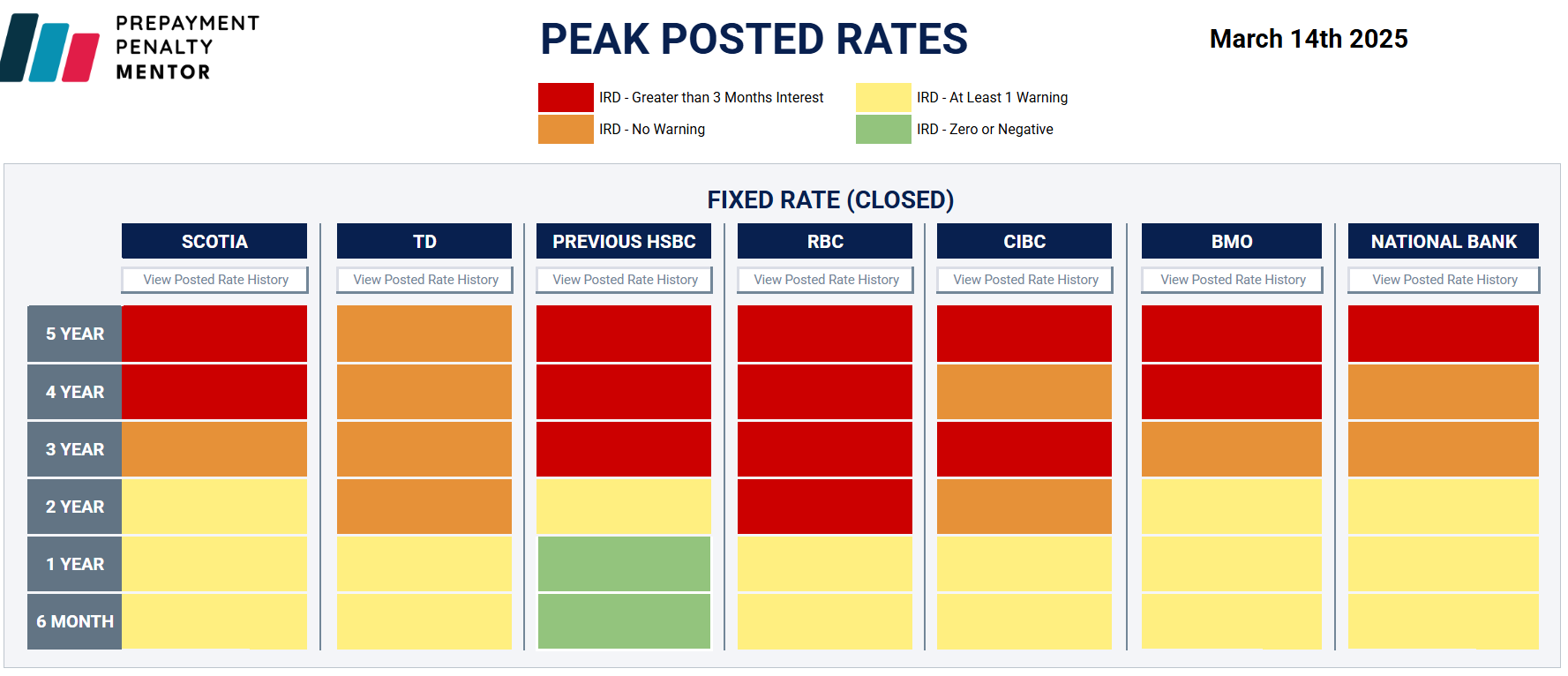

RBC Mortgage Payout Penalties Skyrocket in 2025

Details of the recent actions RBC has taken to INCREASE THE PAYOUT PENALTY for their own customers.It shows that Big-6 Banks are not your best -mortgage- friend. Brokers Are!Mortgage Mark Herman, Top Calgary Alberta mortgage broker

If you’re seeking a textbook case of banks giving consumers the short end of the stick, look no further.

The nation’s biggest mortgage lender, RBC, just slashed its posted rates.

“RBC’s move is the biggest move to increase penalties (IRDs) since its posted rates peaked on September 20, 2023,” says Matt Imhoff, founder of Prepayment Penalty Mentor.

For those fluent in the dark arts of interest rate differential (IRD) charges, this spells disaster for anyone daring to escape their RBC mortgage shackles early. Here’s precisely how grim it gets…

This is what RBC did to its posted rates today (Friday):

- 5 Year: -30 bps

- 4 Year: -25 bps

- 3 Year: -35 bps

- 2 Year: -85 bps

- 1 Year: -55 bps

- 6 Month: -55 bps

Anyone attempting to break a 2, 5, 7, or 10-year RBC mortgage now is potentially in for a world of penalty hurt due to these changes.

By way of example, if you’re an originator poaching a $500,000 RBC 4.4% 3-year fixed originated in July 2024, that client would be staring down a penalty of approximately $17,500, Imhoff says.

That’s up almost $10,000 in one day—simply because RBC slashed the comparison rate (its 2-year posted rate in this case).

In other words, the 255 bps “discount” from posted that this customer got in 2024 is now like a financial boomerang, coming back to hit them hard Imhoff says.

“This IRD is significantly higher than it should be, and that’s the risk of going with a bank where posted rates are elevated.”

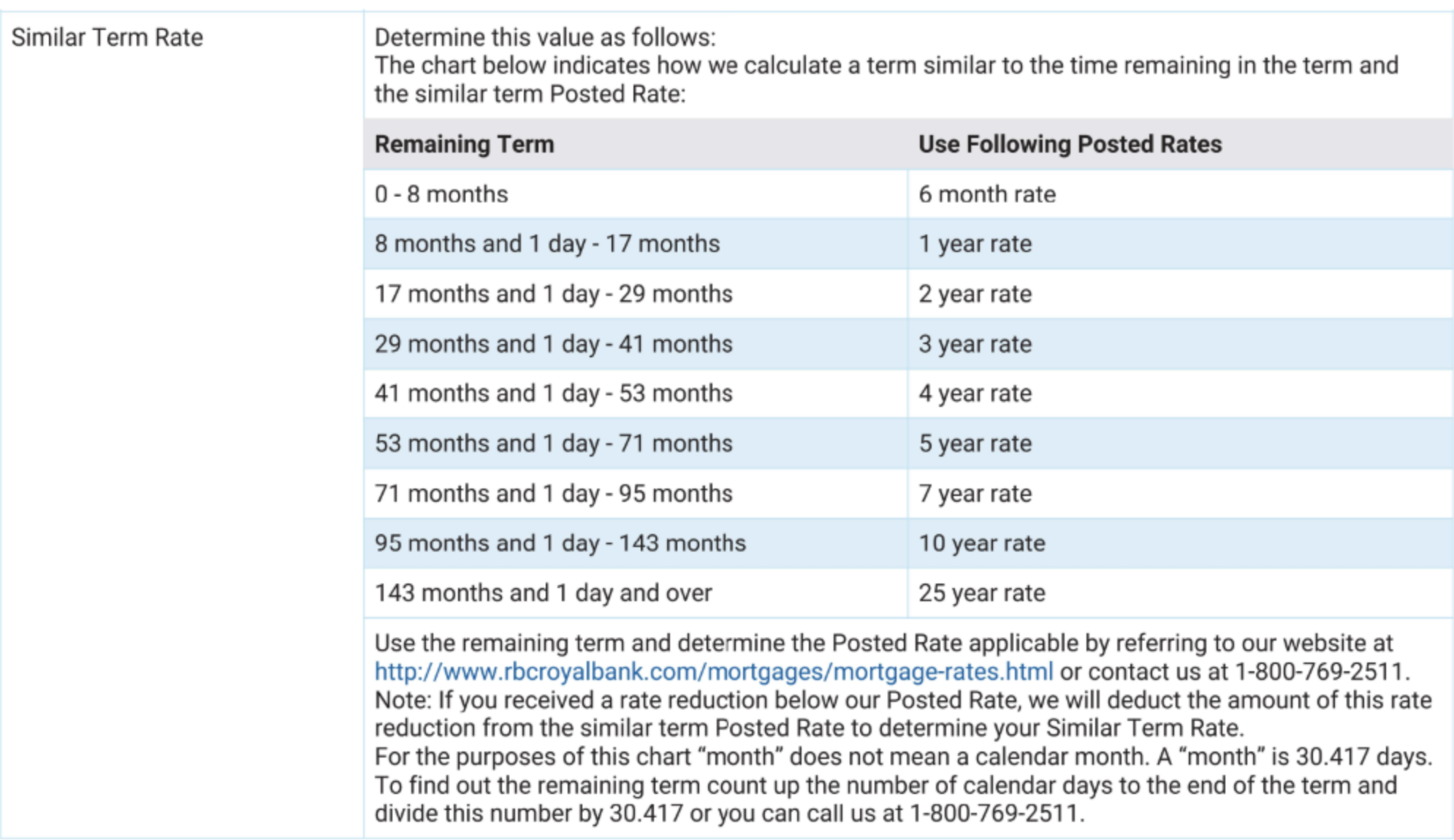

In the above example, the client’s only option to avoid more than a three-month interest penalty would be to ride out their RBC term until they have just 1.41 years remaining (per the chart below).

To virtually ensure a three-month interest penalty, a customer needs to be just eight months shy of their mortgage’s maturity, as illustrated in the RBC table below.

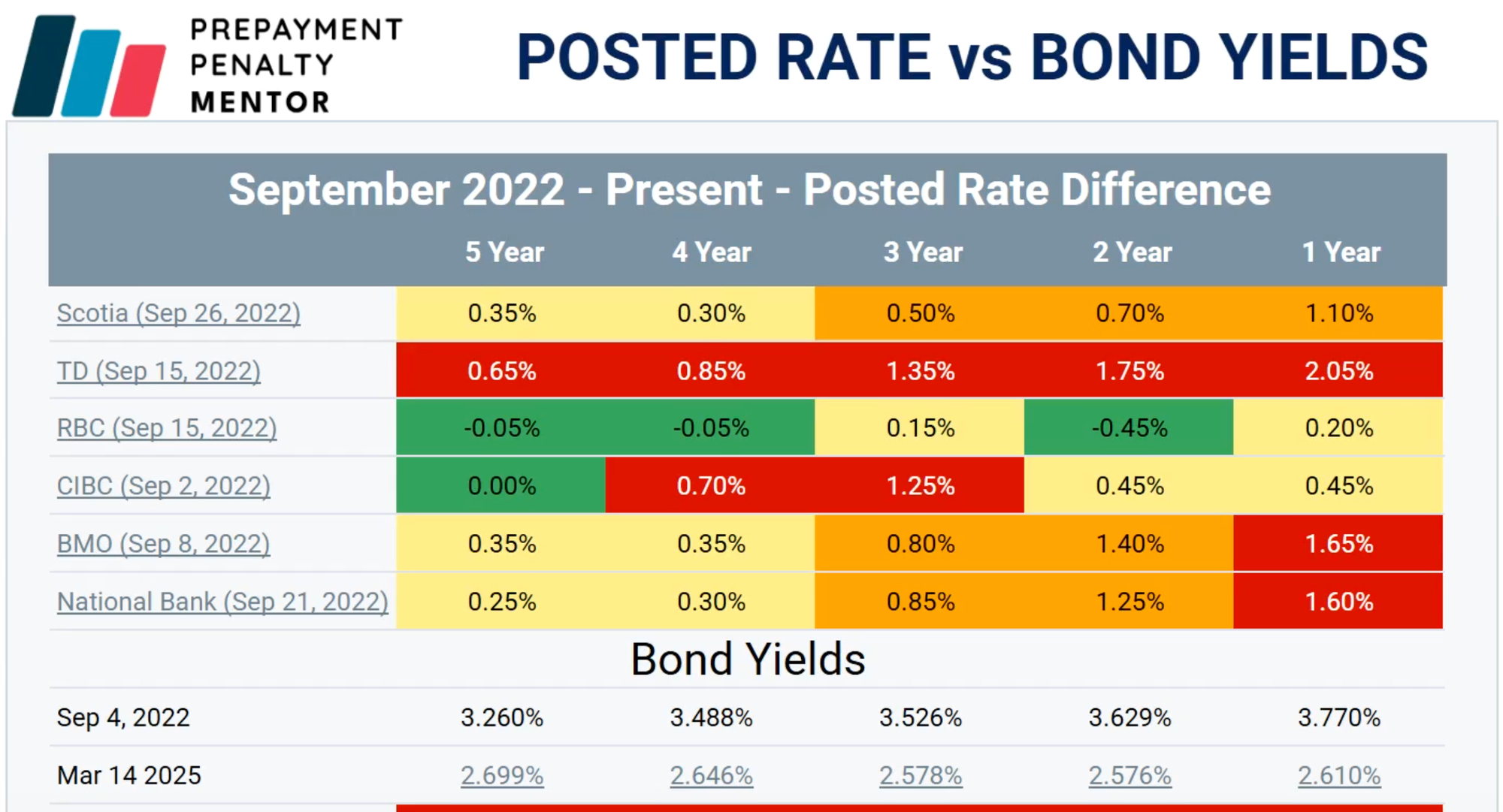

Watch out for TD customers

As Matt’s table below shows, TD’s posted rates are well above where they typically reside relative to bond yields. As a result, “I believe this sets the stage for what TD will inevitably do,” he says.

In cases where a client needs to refi, he adds that the risk of imminent posted rate changes at TD makes it too risky for brokers to get the deal approved elsewhere and then request discharge from TD. Time is money in this case.

“If a broker tries to get a payout order from TD today, TD can wait up to five business days,” Imhoff notes, adding that during that time, the penalty can go up.

In the event that early discharge makes clear sense, he says, “I am advising brokers to have their TD clients go to the branch, break the mortgage, pay the penalty while it is still on sale, and switch into an open.”

PPM has a great table (below) that also shows which terms at which banks are most prone to IRD penalties. Terms in red face IRD charges now, based on the assumptions the user enters. Terms in orange are at risk of being charged IRDs on the next posted rate drop.

It pays to know in advance when penalties make a refinance uneconomical. “There are brokers working on deals today that will never fund—all that wasted time, effort, money, just to get a payout that kills the deal.”

Bank of Canada Lowers Consumer Prime to 4.95%

The Bank of Canada lowers its benchmark interest rate to 2.75%

In the face of significant geopolitical tensions, the Bank of Canada announced today that it has lowered its policy interest rate by 25 basis points. This marks the seventh reduction since June of 2024.

Below, we summarize the Bank’s commentary.

Canadian Economic Performance and Housing

- Canada’s economy grew by 2.6% in the fourth quarter of 2024 following upwardly revised growth of 2.2% in the third quarter

- This “growth path” is stronger than was expected when the Bank last reported in January 2025

- Past cuts to interest rates have boosted economic activity, particularly consumption and housing

- However, economic growth in the first quarter of 2025 will likely slow as the intensifying trade conflict weighs on sentiment and activity

- Recent surveys suggest a sharp drop in consumer confidence and a slowdown in business spending as companies postpone or cancel investments

- The negative impact of slowing domestic demand has been partially offset by a surge in exports in advance of tariffs being imposed

- The Canadian dollar is broadly unchanged against the US dollar but weaker against other currencies

Canadian Inflation and Outlook

- Inflation remains close to the Bank’s 2% target

- The temporary suspension of the GST/HST lowered some consumer prices, but January’s Consumer Price Index was “slightly firmer” than expected at 1.9%

- Inflation is expected to increase to about 2.5% in March with the end of the tax break

- The Bank’s preferred measures of core inflation remain above 2%, mainly because of the persistence of shelter price inflation

- Short-term inflation expectations have risen in light of fears about the impact of tariffs on prices

Canadian Labour Market

- Employment growth strengthened in November through January and the unemployment rate declined to 6.6%

- In February, job growth stalled

- While past interest rate cuts have boosted demand for labour in recent months, there are warning signs that heightened trade tensions could disrupt the recovery in the jobs market

- Meanwhile, wage growth has shown signs of moderation

Global Economic Performance, Bond Yields and the Canadian Dollar

- After a period of solid growth, the US economy looks to have slowed in recent months, but US inflation remains slightly above target

- Economic growth in the euro zone was modest in late 2024

- China’s economy has posted strong gains, supported by government policies

- Equity prices have fallen and bond yields have eased on market expectations of weaker North American growth

- Oil prices have been volatile and are trading below the assumptions in the Bank’s January Monetary Policy Report

Rationale for a rate cut

While the Bank offered that economic growth came in stronger than it expected, the pervasive uncertainty created by continuously changing US tariff threats is restraining consumers’ spending intentions and businesses’ plans to hire and invest. Against this background, and with inflation close to the 2% target, the Bank decided to reduce its policy rate by 25 basis points.

Outlook

The Bank notes that the Canadian economy entered 2025 “in a solid position,” with inflation close to its 2% target and “robust” GDP growth. However, heightened trade tensions and tariffs imposed by the United States will likely slow the pace of economic activity and increase inflationary pressures in Canada. The economic outlook continues to be subject to more-than-usual uncertainty because of the rapidly evolving policy landscape.

Final comments

The Bank noted that monetary policy “cannot offset the impacts of a trade war.” What monetary policy “can and must do” is ensure that higher prices do not lead to ongoing inflation.

The Bank said it will carefully assess: i) the timing and strength of both the downward pressures on inflation from a weaker economy and ii) the upward pressures on inflation from higher costs. It will also closely monitor inflation expectations.

It ended its statement by saying it is committed to maintaining price stability for Canadians.

More scheduled BoC news

The Bank is scheduled to make its third policy interest rate decision of 2025 on April 16th.

Bank of Canada lowers benchmark interest rate to 3%

The Bank of Canada opened its monetary policy playbook for 2025 with a 0.25% reduction in its overnight rate. The 6th since June of last year.

In issuing its January Monetary Policy Report, the Bank also noted that its projections are subject to “more-than-usual uncertainty” because of the rapidly evolving policy landscape, particularly the threat of trade tariffs by the new administration in the United States.

Variable rates win, but can you handle some possibly sleepless nights if Trump’s tariffs increase fixed rates as much as 3%?

(Click to see the link to the report showing this.)

If Canada does a full retaliation to Trump’s 25% tariffs our Canadian interest rates could go up by 3%; and if there is no retaliation at all, Canadian interest rates could go down by up to 3% as well!

Mortgage Mark Herman, 20+ years of mortgage experience with an MBA from a top school & Top Calgary Alberta Mortgage Broker

Below, we summarize the Bank’s commentary.

Canadian economic performance and housing

- Past interest rate reductions have started to boost the Canadian economy

- Recent strengthening in both consumption and housing activity is expected to continue

- Business investment, however, remains weak

- The outlook for exports is supported by new export capacity for oil and gas

Canadian inflation and outlook

- Inflation measured by the Consumer Price Index (CPI) remains close to 2%, with some volatility due to the temporary suspension of the GST/HST on some consumer products

- Shelter price inflation is still elevated but it is easing gradually, as expected

- A broad range of indicators, including surveys of inflation expectations and the distribution of price changes among components of the CPI, suggest that underlying inflation is close to 2%

- The Bank forecasts CPI inflation will be around the 2% target over the next two years

Canadian labour market

- Canada’s labour market remains soft, with the unemployment rate at 6.7% in December

- Job growth, however, has strengthened in recent months, after lagging growth in the labour force for more than a year

- Wage pressures, which have proven sticky, are showing some signs of easing

Global economic performance, bond yields and the Canadian dollar

- The global economy is expected to continue growing by about 3% over the next two years

- Growth in the United States has been revised upward, mainly due to stronger consumption

- Growth in the euro area is likely to be subdued as the region copes with competitiveness pressures

- In China, recent policy actions are boosting demand and supporting near-term growth, although structural challenges remain

- Since October, financial conditions have diverged across countries with bond yields rising in the US, supported by strong growth and more persistent inflation, and bond yields in Canada down slightly

- The Canadian dollar has depreciated materially against the US dollar, largely reflecting trade uncertainty and broader strength in the US currency

- Oil prices have been volatile and in recent weeks have been about $5 higher than was assumed in the Bank’s October Monetary Policy Report

Other comments

The Bank also announced its plan to complete the normalization of its balance sheet, which puts an end to quantitative tightening. The Bank said it will restart asset purchases in early March 2025, beginning gradually so that its balance sheet stabilizes and then grows modestly, in line with growth in the economy.

It also offered further rationale for today’s decisions by saying that with inflation around 2% and the economy in excess supply, the Bank’s Governing Council decided to reduce its policy rate. It also noted that cumulative reduction in the policy rate since last June is “substantial.” Lower interest rates are boosting household spending and, in the outlook it published (see below), the economy is expected to strengthen gradually and inflation to stay close to target.

Outlook

In today’s announcement, the Bank laid out its forecast for Canadian GDP growth to strengthen in 2025. However, it was quick to also point out that with slower population growth because of reduced immigration targets, both GDP and potential growth will be “more moderate” than what the Bank previously forecast in October 2024.

To put numbers on that forecast, the Bank now projects GDP will grow by 1.8% in both 2025 and 2026. As a result, excess supply in the Canadian economy is expected to be “gradually absorbed” over the Bank’s projection horizon.

Setting aside threatened US tariffs, the Bank reasons that the upside and downside risks in its outlook are “reasonably balanced.” However, it also acknowledged that a protracted trade conflict would most likely lead to weaker GDP and higher prices in Canada and test the resilience of Canada’s economy.

The Bank ended its statement with its usual refrain: it is committed to maintaining price stability for Canadians.

2025 will bring more BoC news

The Bank is scheduled to make its second policy interest rate decision of 2025 on March 12th. I will provide an executive summary immediately following that announcement.

Summary of Mortgage Rule Changes

Key Mortgage Rule Updates

30-year amortization for insured mortgages

Starting December 15, 2024, 30-year amortizations will be available for insured mortgages. This option is open to first-time homebuyers and those purchasing newly built homes, including condos.

Higher insured mortgage limits

Applications for insured mortgages will now be accepted for properties valued under $1.5 million, giving more buyers access to high-value homes with lower down payment requirements.

Stress test simplification

In line with OSFI’s guidance, current stress test requirements will continue for insurable, uninsurable, and uninsured applications. Eligible insured transfers and switches will remain qualified at the contract rate.

How these changes benefit you

✔️ Reduced monthly payments

Extending amortizations to 30 years will lower monthly payments, helping clients manage affordability amidst rising living costs and fluctuating interest rates.

It usually works out to reduce your payment by 9% or lets yo buy 9% more home (increases the mortgage amount but about 9%.)

✔️ Expanded opportunities for buyers

Higher insured mortgage limits make it possible for more Canadians to purchase homes in competitive urban markets like Toronto and Vancouver for up to $1,500,000 with 5% down on the 1st 500k and 10% down payment on the balance.

This set of mortgage rule changes should make it easier for buyers to get into a home now.

More importantly, it lets buyers purchase up to $1.5M with $125k down, where before they would have topped out at $1m with $75k down payment.

- Mortgage Mark Herman, top best Calgary mortgage broker,

- 403,681-4376

Current Risks to the Canadian Mortgage Market? May 15th, 2024

Summary:

May 21, 2024 is when the inflation a report comes out and it should be the determining factor if the Canadian PRIME RATE of INTEREST is reduced from 7.2% in June or not. Maybe July. Maybe later.

Nobody is buying anything big right now, which is the idea … to reduce inflation.

Which means now is the best time to buy a home before everyone waiting for rates to drop jumps in on the 1st Prime rate reduction.

Says Mortgage Mark Herman, Calgary Alberta best/ top/ mortgage broker for first time home buyers

DATA:

Mortgage holders have been anxiously waiting for the Bank of Canada to cut interest rates. The increase of 90,400 jobs in April – 5 times what analysts expected – has heightened concerns that the Bank will continue to wait before lowering rates. 🙁

While the economy has not slowed as much as expected, there’s growing economic slack, with the jobless rate up 1 percentage point over the past year and a 24% year-over-year increase in the number of unemployed individuals, which is slowing down wage growth. The crucial factor in determining whether a rate cut will occur in June or be postponed to later this year hinges on the April CPI release scheduled for May 21st.

In the background of these deliberations, the Bank of Canada also assesses various potential risks to the economy. Last week, the Bank released its Financial Stability Report, highlighting two key risks: debt serviceability and asset valuations.

The report notes that the share of mortgage holders who are behind on their credit cards and auto loan payments, which had hit historic lows during the pandemic, has now returned to more normal levels. It also notes that smaller mortgage lenders are seeing an uptick in credit arrears. This increase isn’t surprising, given the run up in rates and the market segment that these lenders cater to. While the arrears rate is up, it remains relatively low compared to historical levels.

This overall positive portfolio performance is due to two key factors: 1) financial flexibility and 2) employment.

Canadian mortgage defaults tend to spike up during periods of rising unemployment. While the unemployment rate has risen, it remains relatively low. Additionally, mortgagors are holding higher levels of liquid assets. Before the pandemic, homeowners with a mortgage held 1.2 months of liquid reserves, which increased to 2.2 months during the pandemic and has since fallen to 1.8 months. These increased reserves provide a solid buffer for mortgagors to meet unexpected increases in expenses.

The Bank remains concerned that nearly half of all outstanding mortgages have yet to be renewed, leaving these borrowers at risk of payment shock due to the increase in interest rates. Scotiabank is an interesting case because, unlike other banks, it offers adjustable-rate mortgages (ARM) with variable payments instead of variable rate mortgages with fixed payments. Scotia has seen its 90+ days past due rate increase from 0.09% to 0.16%. During their fourth-quarter earnings call, Scotia noted that ARM borrowers have been cutting back on discretionary spending by 11% year-over-year, compared to a 5% reduction among fixed-rate clients.

The mortgage maturity profile in the Financial Stability Report suggests that we could see significant slowing in consumer discretionary spending over the next two years. While the rise in debt-servicing costs will be partially offset by income growth, we should expect to see belt tightening by mortgage holders. This poses less of a risk to the banking sector mortgage market than to the overall outlook for the economy.