Using Return-To-Work Income while on Maternity Leave to buy a home IS possible in Canada.

Using Return-To-Work Income while on Maternity Leave to buy a home IS possible in Canada.

Are you on maternity leave and trying to buy a home, but the bank will not use your income? This is a common reason home buyers find us on the internet or their realtors send them to us.

We CAN use your FULL RETURN TO WORK SALARY as qualifying income, if you have a “return to work date” that is less than 12 months away from your home purchase possession date.

Big-6 banks do not do this and we have no idea why. It frustrates everyone, and broker lenders have no issue with it.

Mortgage Mark Herman, Top-Best Calgary mortgage broker near me.

And while we are it – our lenders also use CCB – Canadian Child tax Benefit – for all children aged UNDER 16, when the mortgage starts.

Big-6 banks don’t use this … not sure why that is.

What else about Broker Lenders?

Broker lenders are all secure, and many are publicly traded, and all are audited by the same staff the investigate all of the Big-6 banks.

Broker lenders also have payout penalties that are 500% to 800% LESS than the way Big-6 banks do it. Here are the links for that specific data on my blog:

- General explanation: http://markherman.ca/payout-penalties-how-the-big-5-banks-get-you/

- Details of all the lenders and their specific math: http://markherman.ca/fixed-rate-mortgage-penalties-larger-than-ever/

Broker lenders ALWAYS renew you are best rates, while Big-6 banks know that 86% of mortgages that renew will take the 1st offer so they “bump the rate” on you. Then you have to call in/ go in to chisel them down.

- At broker lenders, they expect you to call us to check the rates and we would jump at the chance to move you to a different lender and get paid again … so you get best rates with broker banks.

There is lots more to … call to find out.

Mortgage Mark Herman, licensed in Alberta since 2004.

403-681-4376

Bank of Canada increases its benchmark interest rate to 4.50%

Today, the Bank of Canada increased its overnight benchmark interest rate 25 basis point to 4.50% from 4.25% in December. This is the eighth time since March 2022 that the Bank has tightened money supply to address inflation.

While the headline increase will certainly make news, it is the Bank’s accompanying commentary on its future moves that will capture the most attention. We summarize the Bank’s observations below, including its forward-looking comments on the potential for future rate increases.

Canadian inflation

- Inflation has declined from 8.1% in June to 6.3% in December, reflecting lower gasoline prices and, more recently, moderating prices for durable goods

- Despite this progress, Canadians are still “feeling the hardship” of high inflation in their essential household expenses, with persistent price increases for food and shelter

- Short-term inflation expectations remain elevated and while year-over-year measures of core inflation are still around 5%, 3-month measures have come down, suggesting that core inflation has “peaked”

Canadian economic and housing market performance

- The Bank estimates Canada’s economy grew by 3.6% in 2022, slightly stronger than was projected in the Bank’s Monetary Policy Report in October, however it projects that growth is expected to “stall through the middle of 2023,” picking up later in the year

- Canadian GDP growth of about 1% is forecast for 2023 and rising to about 2% in 2024, little changed from the Bank’s October outlook

- The economy remains in “excess demand” and the labour market remains “tight” with unemployment near historic lows and businesses reporting ongoing difficulty finding workers

- However, there is “growing evidence” that restrictive monetary policy is slowing activity especially household spending

- Consumption growth has moderated from the first half of 2022 and “housing market activity has declined substantially”

- As the effects of interest rate increases continue to work through the economy, spending on consumer services and business investment is expected to slow

- Weaker foreign demand will likely weigh on Canadian exports

- This overall slowdown in activity will allow supply to “catch up” with demand

Global economic performance and outlook

- The Bank estimates the global economy grew by about 3.5% in 2022, and will slow to about 2% in 2023 and 2.50% in 2024 — a projection that is slightly higher than the Bank’s forecast in October

- Global economic growth is slowing, although it is proving more resilient than was expected at the time of the Bank’s October Monetary Policy Report

- Global inflation remains high and broad-based although inflation is coming down in many countries, largely reflecting lower energy prices as well as improvements in global supply chains

- In the United States and Europe, economies are slowing but proving more resilient than was expected at the time of the Bank’s October Monetary Policy Report

- China’s abrupt lifting of pandemic restrictions has prompted an upward revision to the Bank’s growth forecast for China and “poses an upside risk to commodity prices”

- Russia’s war on Ukraine remains a significant source of uncertainty

- Financial conditions remain restrictive but have eased since October, and the Canadian dollar has been relatively stable against the US dollar

Outlook

Taking all of these factors into account, the Bank decided today’s policy rate increase was necessary and justified.

However, the Bank also offered this important piece of news: “If economic developments evolve broadly in line with (its) outlook, Governing Council expects to hold the policy rate at its current level while it assesses the impact of the cumulative interest rate increases.”

That sounds positive, but as is customary, the Bank also noted that it is prepared to increase the policy rate further if needed to return inflation to its 2% target. It also added the usual language that it “remains resolute in its commitment to restoring price stability for Canadians.”

Although the Bank did not say it, the bottom line is Canadians will have to wait and see what comes next.

Next touch point

March 8, 2023 is the Bank’s next scheduled policy interest rate announcement and we will be on hand to provide an executive summary the same day.

Canadian Residential Mortgage Market: Inflation & Interest Rates: the Lead Characters for 2023

Summary:

- The Bank of Canada (BOC) increased interest rates 7 times in 2022. Exactly as expected 16 months ago.

- Inflation is at least 5.7%; and it needs to get down to 3%

- The BoC would rather over-tighten than under-tighten

- Normally it takes 18 to 24 months for interest rate increases to work their way into the economy and we are only about 10 months into this tightening cycle

These 4 painful data points mean Prime will increase from 6.45% to 6.70% on Jan 25th.

We now expect there to be at least 1 or 2 more o.25% increases to Prime before it is expected to hold for the rest of 2023, and then begin to decrease in 2024.

Mortgage Mark Herman, Top Calgary Alberta Mortgage Broker

DATA

A lot of the recent talk in financial and real estate circles has been centering on the possibility of a pause in the Bank of Canada’s aggressive interest rate increases. Some speculate that could happen at the next rate setting, later this month, on January 25th.

The Bank raised rates 7 times last year in an effort to rein-in galloping inflation. It does seem to be working, but there are some stubborn sticking points.

Headline inflation, known as the Consumer Price Index (CPI), has dropped. It was 8.1% in July and drifted down to 6.8% in November. However, the drop from October to November was a mere one-tenth of one percentage point and the Bank’s target rate remains significantly below that, at 2.0%.

As well, the BoC’s preferred inflation measure, Core Inflation (which strips out volatile components like food and fuel), actually increased. A simple averaging of the three components that the Bank uses to measure Core Inflation came in at nearly 5.7% in November, up from 5.3% in October.

Other factors that figure into the Bank’s plans include Gross Domestic Product and unemployment. Canada’s GDP continues to grow, albeit modestly, despite rising interest rates. It increased by 0.1%, month-over-month in November. Unemployment dipped 0.1% to 5.0% in December. Both of these tend to fuel higher wages which are a key driver of inflation.

The Bank of Canada, itself, remains firmly dedicated to battling back inflation. Governor Tiff Macklem has said he would rather over-tighten than under-tighten and run the risk of having high inflation linger and become entrenched.

The U.S. central bank has made it clear it plans more rate hikes. Given the integration of the Canadian and American economies, the Bank of Canada does have to pay attention to what its American counterpart does.

The BoC will have new economic data by the time it makes its January 25th announcement. The December numbers will provide a fresh look at how well the inflation fight is going.

Normally it takes 18 to 24 months for interest rate increases to work their way into the economy and we are only about 10 months into this tightening cycle. It is reasonable to expect another 25 basis-point increase on the 25th. Given the Bank’s apparent success so far it also seems reasonable to expect a pause sometime after that.

Looking ahead to a year from now some forecasters say we might start to hear talk of interest rate cuts, which would be welcome news. Cuts would allow the BoC to move toward its, long stated, goal of normalizing rates back into the neutral range of 2.5% to 3.5%. The Bank of Canada, and central banks around the world, have been trying to do that for more than a decade – since the ’08 – ’09 financial collapse.

Details of Canadian Economic & Housing Market Performance, as at Dec 7, 2022

Bank of Canada increased Consumer Prime to 6.45% – exactly as expected for the last 5 months. January 25th is the next BoC interest rate announcement & I hope it is a 0.25% increase and then holds there for all of 2023. We will see…

Mortgage Mark Herman, Best Calgary mortgage broker with a Master’s degree in Finance.

Today, the Bank of Canada increased its overnight benchmark interest rate 50 basis point to 4.25% from 3.75% in October. This is the 7th time this year that the Bank has addressed inflation and means the policy rate is now as high as it has been in 15 years.

We summarize the Bank’s observations below, including its forward-looking comments on the need/likelihood of future rate increases below:

Canadian inflation

- CPI inflation remained at 6.9% in October, with many of the goods and services Canadians regularly buy showing large price increases

- Measures of core inflation “remain around 5%”

- Three-month rates of change in core inflation have come down, “an early indicator that price pressures may be losing momentum”

Canadian Economic and housing market performance

- GDP growth in the third quarter was stronger than expected, and the economy continued to operate “in excess demand”

- The labor market remains “tight” with unemployment near historic lows

- While commodity exports have been strong, there is growing evidence that tighter monetary policy is restraining domestic demand: consumption moderated in the third quarter

- Housing market activity continues to decline

- Data since the October Monetary Policy Report supports the Bank’s outlook that growth will essentially stall” through the end of this year and the first half of 2023

Global inflation and economic performance

- Inflation around the world remains high and broadly based

- Global economic growth is slowing, although it is proving more resilient than was expected at the time of the Bank’s October Monetary Policy Report

- In the United States, the economy is weakening but consumption continues to be solid and the labor market remains “overheated”

- The gradual easing of global supply bottlenecks continues, although further progress could be disrupted by geopolitical events

Outlook

Although the Bank’s commentary noted that price pressures that are driving high inflation may be losing momentum, it went on to say that inflation is “still too high” and that short-term “inflation expectations remain elevated.” In the Bank’s view, the longer that Canadian consumers and businesses expect inflation to be above the Bank’s 2% target, “the greater the risk that elevated inflation becomes entrenched.”

Given these economic signals, the Bank’s Governing Council stated that it “will be considering whether the policy interest rate needs to rise further to bring supply and demand back into balance and return inflation to target.”

It concluded its statement with a familiar refrain: “We are resolute in our commitment to achieving the 2% inflation target and restoring price stability for Canadians.”

Analysts and commentators will seek to interpret those outlook comments for signs that the Bank has reached or believes it is close to reaching the terminal point in its current rate-hike cycle. For now, that remains a question of debate and speculation that will turn on future economic signals.

Next Touchpoint

January 25th is the next BoC interest rate announcement. I hope it is a 0.25% increase and then holds there for all of 2023. We will see…

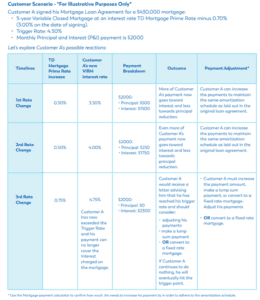

Trigger Point for Canadian Variable Rate Mortgages Explained, with Example

You have likely heard – or will soon be hearing – a lot of talk about “trigger rates” and “trigger points”. More importantly, you are probably hearing “trigger point” together along with more changes in the Bank of Canada rate and you need expert guidance.

Let’s start with a few definitions:

- Variable Rate Mortgage (VRM) – prime changes, rate changes. When interest rates change, typically, your mortgage payment will stay the same.

- Adjustable Rate Mortgage (ARM) – prime changes, rate changes. Unlike variable rate, your mortgage payment will change when interest rates change.

- Trigger Rate – When interest rates increase to the point that regular principal and interest payments no longer cover the interest charged, interest is deferred, and the principal balance (total cost) can increase until it hits the trigger point.

- Trigger Point – When the outstanding principal amount (including any deferred interest) exceeds the original principal amount. The lender will notify the customer and inform them of how much the principal amount exceeds the excess amount (Trigger Point). The client then typically has 30 days to make a lumpsum payment; increase the amount of the principal and interest payment; or convert to a fixed rate term.

NOW, WHICH MORTGAGES WILL BE AFFECTED FIRST?

Quick answer, VRMs from March 2020 to March 2022.

During the month of March 2020, the prime rate dropped three times in quick succession from 3.95% to 2.45%, and variable-rate mortgages arranged while prime was 2.45% have the lowest payments. The lower the interest rate was, the lower the trigger rate, and the faster your client may hit this negative amortization.

WHAT TO DO

When this happens, customers are contacted by the lender and generally have three ways they can proceed:

- Make a lump-sum payment against the loan amount

- Convert with a new loan at a fixed-rate term

- Increase their monthly payment amount to pay off their outstanding principal balance within their remaining original amortization period

Below is a customer scenario so you can see how this could play out.

WHY ARE DEBT SERVICING RATIOS IMPORTANT WHEN APPLYING FOR A MORTGAGE?

HOW ARE DEBT SERVICING RATIOS CALCULATED?

There are two ratios you need to worry about—gross debt servicing (GDS) and total debt servicing (TDS)

Gross debt servicing (GDS)

This is the maximum amount you can afford for shelter costs each month. It’s your monthly housing costs divided by your monthly income.

Total debt servicing (TDS)

This is the maximum amount you can afford for debt payments each month. It’s your monthly debt and housing costs divided by your monthly income.

If too much of your income is already going to housing costs and debt payments, according to your lender, you may not be able to afford to take on more debt.

WHAT DOES DEBT SERVICE RATIO MEAN AND WHY IS IT IMPORTANT?

Lenders use ratios to assess risk and understand if you will be able to make your payments on a mortgage. Generally, lenders like to see a GDS ratio around 32% and a TDS ratio that is no greater than 40%. If the ratios are higher, that does not mean you won’t qualify for a mortgage, but you may end up paying a higher interest rate.

In general, the better your debt servicing ratios and credit score, the lower your interest rate will be. This is because lenders view you as more reliable and it shows that you manage your money well and make your payments on time. Even if you need to refinance now, at a slightly higher rate, you can look at getting into a lower rate in a couple of years, when you mortgage term is up for renewal.

Your debt servicing ratio also lets you know how well you’re managing your budget. If your TDS ratio is over 44%, you are spending too much of your income on debt already and you may be unable to borrow without a co-signer. A co-signer’s credit history and income is factored in with yours. This gives the lender some reassurance that the payments will be made because the co-signer is as responsible for the mortgage as you are.

CALCULATING YOUR PERSONAL DEBT SERVICING RATIOS

Start by adding up your monthly debt payments. Include those fixed costs that you must pay every month:

| Housing costs | Debt costs |

● Rent or mortgage payments● Property taxes● Heat● 50% of condo fees |

● Loan payments, such as car, student, or personal loans● Credit cards (3% of the outstanding balance)● Outstanding bill payments not on a credit card (dental, medical, repairs)● Interest charges for line of credit payments● Spousal or child support payments |

Next add up your monthly income:

- Pay cheque (before taxes)

- Retirement or pension payments

- Benefits payments

- Spousal or child support

- Rental income

- Any other monthly income

Formulas:

Gross debt servicing ratio |

Total debt servicing ratio |

Housing Cost———————— x 100 Total income |

Housing Costs + Debt Costs————————————- x 100 Total income |

Examples:

Your income (before taxes) is $6,500 per month. You have a monthly mortgage payment of $1,400, property taxes of $ $300, and $ $100 for heat. Your GDS ratio is calculated as $1,800/$6,500 x 100 = 27.69%

Your income (before taxes) is $6,500 per month. You spend $300 for your car payment. You have $2,500 in credit card debt, and 3% of the outstanding balance is $75 for a total of $375 per month. Your TDS ratio is calculated as $2,175÷ $6,500 x 100 = 33.46%.

To learn more about specific mortgage approval ratios, check out this handy article.

Note: If you have a two-income household, include the debt payments and income for both of you. This is important because you have more income between you, and you share the cost for some of the debt.

TIPS FOR LOWERING YOUR DEBT SERVICING RATIOS

There are two basic ways to improve your debt servicing ratios—increase your income or reduce your debt.

Increasing your income is not always possible, although it could include a raise at work, finding a new job with better pay, or taking a second job. If you do find yourself with a little extra cash—maybe you received a year-end bonus—consider using it to pay down your debt.

Paying down your debt and not adding to it is the best way to improve your debt servicing ratio. Here are a few ideas to get you started:

- Avoid making new purchases, especially if you need to use your credit card to make the purchase.

- Create a budget and see where you can cut expenses. Apply those savings to your debt.

- Call your credit card company and try renegotiating a lower interest rate. With a lower rate, more of your payment will be applied to what you owe

- If you have money sitting in an account that is not earning much interest, consider applying it toward your debt, which tends to have a higher interest rate.

- Explore options to refinance equity from your home to pay off debt (work with your mortgage broker to form a plan).

DEBT SERVICING RATIOS AND YOUR CREDIT SCORE

Your debt servicing ratios do not directly affect your credit score but carrying a large amount of debt can negatively affect both. And lenders will look at both when assessing your mortgage application. The good news is that reducing your debt improves your credit score as well as your debt servicing ratios. Work with your mortgage broker to create a plan on how you will reduce your debt and improve your ratios. This informative credit video may be useful, straight from a seasoned underwriter.

Your debt servicing ratios give lenders information about your ability to repay the money you borrowed while your credit score provides information about the way you manage credit. Do you make payments on time? Do you have a history of borrowing and repaying money?

Now that you know how a lender is going to assess your mortgage application, you can take the necessary steps to lower your debt servicing ratios and get that mortgage approved!

Mortgage Mark Herman, Top Calgary Alberta mortgage broker

Mortgage Tips for Canadian Buyers

Buying a home should be exciting – not exhausting.

Mortgage Checklist

1. Determine your Budget

Determine what your monthly budget is for the following:

– Mortgage payment

– Property taxes and Condo fees (if applicable)

– Utilities, maintenance and repair

2. Pre- Qualification

You will be asked to provide information about yourself and whoever is going to be on the mortgage with you. All of the information that is relayed is strictly confidential. You will be provided with a Mortgage Disclosure and Consent document to review and sign. Next, your Mortgage Broker will pull your credit bureau and review your overall situation and start the document collection process so they can determine your maximum purchase price and min down payment. A rate hold can be obtained once documents have been reviewed.

3. Document Preparation

Income for Salary or Hourly Employees

– Most recent Pay Stub

– Letter of employment – must be on company letterhead and state your name, position, length of employment. Guaranteed min # of hours and rate of pay or annual salary. It also must have contact information for the lender to call to verify employment once an offer has been made.

– Last 2 years Notice of Assessments (NOAs), T1 Generals and T4 slips for any hourly overtime, commission or bonus income

Income for Self-Employed:

– Last two years Notice of Assessments and T1 generals + confirmation no CRA tax in arrears

– Last 2 years statement of business activities for Sole Proprietors

– Articles of incorporation and Last 2 years company financials for Corporations/Partnerships

Down Payment/Closing Costs

– Anti Money Laundering Laws require the lender to review your 90 day Bank or Investment account histories to verif funds in account for down payment. Any frequent or large deposits and transfers must be verified. Online statements are acceptable, but smartphone screenshots are not.

– Gift letter + gift funds deposited to account, proof of Line of Credit available or sale of existing home proceeds (if applicable)

– You are required to have 1% to 1.5% of the purchase price on top of your down payment for costs relating to the closing of your new home purchase such as home inspection, property tax adjustments, appraisal fees, title insurance, moving expenses, utility hook ups and home fire insurance.

4. Find a realtor and start looking at houses

If you do not already have one, we can highly recommended you to one of our realtor connections. You can the proceed to look for a home that is within your pre-determine price. When you have found a house that you want to purchase, make sure your realtor makes it conditional on obtaining satisfactory financing. It is best to specify 7 to 10 days. It is also recommended to include the condition of a satisfactory house inspection.

5. Mortgage Approval

Once you have a confirmed Offer to Purchase on a house, notify your Mortgage Broker right away so they can start to work on getting the mortgage approved. At this time you will need to give your Mortgage Broker the following documents:

– Updated paystub, job letter and down payment account histories if they are more than 30 days old

– Completed & signed Offer to Purchase

– MLS listing (fact sheet) of the property, if private sale – old MLS listing or appraisal to confirm details

– Lawyer Information (Including the firm and solicitor’s name, address, phone and fax)

– Copy of void cheque for mortgage payments

6. Commitment Signing

A mortgage commitment is provided to your Mortgage Broker by the lender after your deal is approved. Your Mortgage Broker will spend time to review your mortgage commitment with you and let you know about any other lender requirements that need to be fulfilled. You then need to submit those requirements in order to get a final mortgage approval.

7. House Appraisal and Inspection

If required, your Mortgage Broker will order and schedule an appraisal. The mortgage lender determines th requirement of this. This is also the time where you should arrange to have an inspection performed on the home by a certified house inspector. The main purpose of a home inspection is to determine if the home has any existing major defects or any major repairs coming up in the near future. A home inspector will determine structural and mechanical soundness, identify any problem areas, provide cost estimates for any work required and provide you with a report.

8. Condition Removal

Once the lender has confirmed they have all the required documents and the deal is approved you can contact your realtor and have the financing condition removed. At the same time, if the home inspector’s report came back satisfactory, that condition can be removed as well. Do not remove conditions until all amendments to your real estate contract have been reviewed and accepted by the lender as it could affect your financing.

9. Meet with Lawyer

Once all of the conditions for the mortgage are verified and approved, the lender will package your mortgage up and send it to your lawyer whereupon your lawyer will call you in for a meeting one to two weeks before your possession date to go over the legal matters of the mortgage. You will review and sign documents relating to the mortgage, the property you are buying, the ownership of the property and the conditions of the purchase. Your lawyer will also ask you to bring a certified cheque or bank draft to cover closing costs and any other outstanding costs. Avoid signing up for duplicate Mortgage Life/Disability insurance at lawyers.

10. Possession Day

Once the transfer of money has occurred between your lawyer and the seller’s lawyer, you will officially own your new home. Your realtor will arrange to meet with you at your new home and do a walk through to make sure everything is as it should be and also to give you the keys. Congratulations!

Creating happy homeowners by providing personal bespoke mortgages solutions with uncompromising service.

Mortgage Mark Herman

Mortgage Broker & Overall Happiness Creator

Mortgages Are Marvellous

Mark@MortgagesAreMarvellous.ca

Serving Clients In: Calgary, Okotoks, Airdrie, Strathmore, Cochrane, Lethbridge, Red Deer,= & Medicine Hat.

Also Serving: All areas of Alberta including: Edmonton, Sherwood Park, Fort Saskatchewan, Leduc, Nisku, Stony Plain, Spruce Grove, Beaumont and St. Albert. Wood Buffalo / Fort McMurray, Grande Prairie, Airdrie, Lloydminster AB, Okotoks, Cochrane, Camrose, Chestermere, Sylvan Lake, Brooks, Strathmore, High River, Wetaskiwin, Lacombe, Canmore, Morinville, Whitecourt, Hinton, Olds, Blackfalds, Taber, Coaldale, Edson, Banff, Grand Centre, Innisfail, Ponoka, Drayton Valley, Cold Lake, Devon, Drumheller, Rocky Mountain House, Slave Lake, Wainwright, Stettler, St. Paul, Vegreville, Didsbury, Bonnyville, Westlock, Barrhead.

Data on July 1, 2022 Prime Increase to 3.7%

Today, the Bank of Canada showed once again that it is seriously concerned about inflation by raising its overnight benchmark rate to 1.50% – making Consumer Prime 3.70%

This latest 50 basis point increase follows a similar-sized move in April and is considered the fastest rate hike cycle in over two decades.

Everyone STAY COOL!

Says Mortgage Mark Herman, top Calgary Alberta Mortgage Broker.

With it, the Bank brings its policy rate closer to its pre-pandemic level.

In rationalizing its 3rd increase of 2022, the Bank cited several factors, most especially that “the risk of elevated inflation becoming entrenched has risen.” As a result, the BoC will use its monetary policy tools to return inflation to target and keep inflation expectations well anchored.

These are the highlights of today’s announcement.

Inflation at home and abroad

- Largely driven by higher prices for food and energy, the Bank noted that CPI inflation reached 6.8% for the month of April, well above its forecast and “will likely move even higher in the near term before beginning to ease”

- As “pervasive” input pressures feed through into consumer prices, inflation continues to broaden, with core measures of inflation ranging between 3.2% and 5.1%

- Almost 70% of CPI categories now show inflation above 3%

- The increase in global inflation is occurring as the global economy slows

- The Russian invasion of Ukraine, China’s COVID-related lockdowns, and ongoing supply disruptions are all weighing on activity and boosting inflation

- The war has increased uncertainty, is putting further upward pressure on prices for energy and agricultural commodities and “dampening the outlook, particularly in Europe”

- U.S. labour market strength continues, with wage pressures intensifying, while private domestic U.S. demand remains robust despite the American economy “contracting in the first quarter of 2022”

- Global financial conditions have tightened and markets have been volatile

Canadian economy and the housing market

- Economic growth is strong and the economy is clearly “operating in excess demand,” a change in the language the Bank used in April when it said our economy was “moving into excess demand”

- National accounts data for the first quarter of 2022 showed GDP growth of 3.1%, in line with the Bank’s April Monetary Policy Report projection

- Job vacancies are elevated, companies are reporting widespread labour shortages, and wage growth has been “picking up and broadening across sectors”

- Housing market activity is moderating from exceptionally high levels

- With consumer spending in Canada remaining robust and exports anticipated to strengthen, growth in the second quarter is expected to be “solid”

Looking ahead

With inflation persisting well above target and “expected to move higher in the near term,” the Bank used today’s announcement to again forewarn that “interest rates will need to rise further.”

The pace of future increases in its policy rate will be guided by the Bank’s ongoing assessment of the economy and inflation.

In case there was any doubt, the Bank’s message today was clear: it is prepared to act more forcefully if needed to meet its commitment to achieve its 2% inflation target.

July 13, 2022 is the date of the BoC’s next scheduled policy announcement.

Rates Increasing: How Much? & How Fast?

With interest rates now on the rise, 2 Questions: How much? & How fast?

Summary:

- Rates are up by 1.45% on the Variable already (Prime was 1.75% and is now 3.2%)

- There HAS BEEN a 1 x .25% increase and 1 x .5% increase so far = .75% so far

- Expected increases are 1 x .5% or .75%, and 1 x .25% still to come.

- so expect Prime to get to 3.95% from 3.20% today, April 25th.

- Insured variable rates are at Prime – 0.95% = 3.2 – .95% = 2.25% today

- and they are expected to increase to 3.95% – .95% = 3.00% and then hold and decrease in the Fall of 2022.

- these rates are lower than the current 5-year fixed rates of about 4% and are expected to come down in the Fall, 2022.

DETAILS:

Traditionally the Bank of Canada has used 0.25% as the standard increment for any interest rate move up, or down. Occasionally the Bank will move its trendsetting Policy Rate by .50%, as it did at its last setting on April 13.

The last time the central bank boosted the, so-called, overnight rate by ½% was 20 years ago. Now the Bank seems to be laying the ground work for an even bigger increase of .75% at its next setting in June. There has not been a three-quarter point increase since the late 1990s.

Inflation remains the key concern for the BoC. In March the inflation rate hit 6.7%, a 30-year high. The central bank wants to see inflation at around 2.0%. But it does not expect that to happen until sometime late next year.

Bank of Canada Governor will “not rule anything out” when it comes to interest rates and taming inflation. “We’re prepared to be as forceful as needed and I’m really going to let those words speak for themselves.”

While higher inflation was not unexpected as the economy recovered from the pandemic, it is lingering longer than anticipated. The Bank says this is largely due to:

- on-going waves of COVID-19, particularly in China, that have disrupted manufacturing and the supply chain;

- the Russian invasion of Ukraine; and

- spending fuelled by those rock-bottom interest rates that were designed to keep the economy moving during the pandemic.

The Bank is thought to be aiming for a Policy Rate of between 2% and 3%. That is considered a “neutral” rate that neither stimulates nor restrains the economy.

At the current pace, that could be reached by the fall of 2022.

Investment Mortgages WILL Be Harder to Get in 2023!

Its true! This thing called Basel 3 will make it harder to get an investment mortgage in 2023!

Lots of junk below, the short version is:

Canadian banks will need to apply more risk to investor mortgages and to lower that risk they may:

- Increase the down payment needed from 20% to a higher amount … maybe 25% or 30%

- Lend to fewer investors – which already make up 25% to 30% of the Canadian market.

- New Zealand already started 40% down payment for investment properties!

“Avoid the new rules by buying your investment property in 2022!

Mortgage Mark Herman, top Calgary, Alberta mortgage broker.”

DETAILS: Canadian Bank Regulator Confirms Investor Mortgage Reduction Coming Next Year

Canadian real estate investors are about to face higher hurdles to enter the market. The Office of the Superintendent of Financial Institutions (OSFI), Canada’s bank regulator, confirmed new rules being rolled out in Q2 2023. The rules are a part of international Basel III guidelines, designed to reduce risk in the system. One critical change for real estate will be raising the risk weight for investor mortgages. This will reduce their leverage, which OSFI cites as a key response to housing risk. It’s still early, but here’s what we could dig up.

The Basel Trilogy and Global Financial Risk Reduction

The Basel reforms are a global set of measures for prudential bank regulation. They were developed by the Basel Committee On Banking Supervision (BCBS). The BCBS is a 45-country group hosted by the Bank of International Settlements (BIS). The BIS is often called, “the central bank for central banks.” It’s also jokingly called the “final boss” by Bitcoin investors.

We know, it’s a lot of banking jargon and acronyms, but what they do is straightforward. Their job is creating non-partisan risk reduction standards for the global financial system. Since the world’s financial system is now interdependent, problems spill across borders. They stepped up their game after a housing bubble in the US caused a global financial crisis (GFC).

The Basel Accords are a trilogy of policy where the common goals were set. The original happened before many of you were born (1988), but Basel II and III occur after the 2007-2008 GFC. No, circle back. GFC doesn’t stand for Gesus F*cking Christ, we just explained it’s the Global Financial Crisis. We’re also worried about your spelling skills.

The Second Accord primarily addressed minimum capital adequacy requirements. In other words, how much financial institutions had on hand compared to what they lend. Basel III was held in 2010, and mostly just improves the recognition of risk.

A good chunk of BASEL III reforms have already been implemented. Increasing Common Equity Tier 1 (CET) to 4.5% of risk-weighted assets (RWAs) from 2% in BASEL II, is one example. It happened in 2015 and almost no one heard a sound. The measures have been gradually introduced to create as little noise as possible. Though real estate investors might make some noise with the next update.

Basel III Will Land In Q2 2023, and It Will Lower Investor Mortgage Leverage

Basel III will increase the capital requirements for investor mortgages. “as part of the domestic implementation of Basel 3 reform package” in banks’ fiscal Q2-2023, we are increasing the risk weights, and thus capital required, for investor mortgages compared to the risk weights for owner-occupied properties,” said OSFI this morning.

That only tells us a reduction in leverage by Q2 2023 is coming, but not how much. OSFI said they’ll get back to us with what that means for down payments soon. We’ll update as soon as they do, but in the meantime we can get an idea of what we’re in for, from Basel III guidelines.

New standardized credit risk assigns a 30% risk weight to residential real estate. Next year income producing properties with a loan-to-value between 60% and 80% will have a risk weight of 45%. A bank will assume 50% more risk weight for an investor mortgage than an owner occupied home. i.e. owner-occupied mortgages with 20% down have similar risk to investor mortgages with 30% down.

There’s no direct translation of how that’s mitigated. They could want 10 points more for a mortgage, or they can offset risk in various other ways. Raising the risk premium on interest or lending less would be two methods to deal with it. None of those are particularly great for investors, now between 25% and 30% of home sales in Canada. It will slow demand though, which is probably needed.

Raising the down payment is already occurring in other countries like New Zealand. Last year the country increased the minimum downpayment for investors to 40% of the value. Mortgage Professionals Canada (MPC) recently suggested a similar arrangement for Canada. Yup! The organization that represents mortgage brokers suggested it as just a cooling measure. Not even a Basel III mitigation.

The Federal Government has yet to address the issue, probably since most don’t know it’s coming. That means we don’t know if they’ll help reduce the leverage for political points or it’ll come from the banks. One thing’s for sure though — it’s coming next year.