Korean Mortgage in Canada Using Korean Income & Credit History | Calgary Mortgage Broker

Korean Home Buyers in Canada: Get a Mortgage Using Korean Income, Korean Tax Documents, and Korean Credit History

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience specializing in unique and difficult to do deals.

Buying a home in Canada can be challenging if you recently arrived from Korea or still earn most of your income there. Many (as in ALL) of the traditional Canadian lenders (Big6- banks) require extensive Canadian employment history, Canadian tax returns, and established Canadian credit.

The good news is that there are specialty lenders in Canada that understand the needs of Korean home buyers and can approve mortgages using Korean income, Korean employment documents, and even Korean credit reports.

If you’re a Korean citizen, permanent resident, or newcomer to Canada, this specialized mortgage program may help you qualify sooner than you think.

Can I Get a Canadian Mortgage Using Korean Income?

Yes!!

Certain specialty lenders in Canada work specifically with Korean borrowers and can evaluate income earned in Korea. Instead of relying solely on Canadian tax returns and Canadian employment history, these lenders can review:

- Korean tax documents

- Korean employment verification

- Korean pay records

- Korean credit reports

- Korean property ownership documents

This can be especially valuable for:

- New immigrants from Korea

- Permanent residents who recently moved to Canada

- Families with income earned in Korea

- Professionals working for Korean companies

- Individuals relocating to Calgary or other Canadian cities

“Our Korean customers were just as surprised as I was when we found that we can do a mortgage for them, in Canada, using their existing documents from Korea!”

Mortgage Mark Herman, MBA mortgage broker in Calgary specializing in new buyers from Korea

What Documents Are Required?

For Husband and Wife Applicants

The lender typically requires:

Income Verification

2024 and 2025 Certificate of Income from the National Tax Service of Korea (국세청)

These documents help verify historical income earned in Korea.

Employment Verification

Letter of Employment (재직증명서)

The employment letter confirms position, employment status, and employer information.

Income Evidence

- Most recent three pay stubs (급여명세서)

- Three months of direct deposit history

These documents help confirm current earnings and consistency of income.

Existing Property Information

If the applicants own property in Korea:

- Current mortgage statement

- Property tax statement

These documents allow the lender to calculate any existing debt obligations.

For Adult Children Who May Be Co-Signing or On the Mortgage

If an adult child is participating in the application, lenders may require:

- Letter of employment

- Recent pay stubs

- Three months of direct deposit history

- Most recent Notice of Assessment (NOA)

- Proof of no tax owing

Identification Requirements

- Passport

- Driver’s license

- Korean Passport

- Canadian Permanent Resident Card

- Korean Resident Registration Card (주민등록증)

Korean Credit Report

One unique feature of this program is that the lender can often obtain and review a Korean credit report directly.

Applicants will generally be required to sign a credit consent form authorizing the Korean credit search.

How Does the Lender Calculate Foreign Income?

The lender uses a specific formula to determine qualifying income:

Foreign Income = (Gross Foreign Income – Foreign Debt Service) × Recognition Ratio (80%) × Exchange Rate

This means:

- Gross Korean income is reviewed.

- Existing debt obligations are deducted.

- The lender recognizes 80% of the remaining income.

- The income is converted to Canadian dollars using the applicable exchange rate.

Example of Foreign Income Qualification

Let’s assume:

- Annual Korean income: CAD equivalent of $150,000

- Existing Korean debt payments: $20,000 annually

Calculation:

- $150,000 − $20,000 = $130,000

- $130,000 × 80% = $104,000 qualifying income

In this example, the lender would use approximately $104,000 of qualifying income for mortgage approval purposes.

104k income gets about a $425,000 mortgage amount (+ down payment = purchase price)

Important Translation Requirements

All Korean documents must be accompanied by English translations.

Applicants should submit:

- Original Korean documents

- Certified English translations

Providing complete translations early in the process can help avoid delays and speed up approval.

Conditions of Financing Needs to be 14 Days.

This mortgage program requires additional underwriting compared to a standard Canadian mortgage.

Borrowers should allow approximately two weeks for the lender to review the Certificate of Income documents and complete the approval process.

If you are planning to purchase a home, it is important to start the mortgage application early so financing is ready before you remove conditions.

Why Work With a Mortgage Broker Familiar With Korean Mortgage Programs?

Not every mortgage broker understands foreign-income lending or Korean documentation requirements.

An experienced broker can help:

- Review Korean income documents

- Coordinate English translations

- Calculate qualifying income accurately

- Structure the application properly

- Navigate specialty lender requirements

- Avoid unnecessary delays

For Korean families buying property in Calgary and throughout Canada, working with a broker who understands these programs can significantly improve the approval process.

Frequently Asked Questions

Can I qualify for a mortgage in Canada without Canadian income?

Yes. Some specialty lenders can use Korean income and Korean employment documents to qualify borrowers.

Can a lender use my Korean credit report?

Yes. Certain lenders can obtain and review Korean credit reports with your written authorization.

Do my Korean documents need to be translated?

Yes. All Korean documents must be submitted with English translations.

How long does approval take?

Borrowers should generally allow at least two weeks for the lender to review foreign income documentation and issue approval.

Can permanent residents use this program?

Yes. Permanent residents with Korean income may qualify, depending on the lender’s guidelines.

Final Thoughts

Many Korean families assume they must wait years to build Canadian credit and employment history before buying a home.

In reality, some Canadian lenders can use Korean tax documents, Korean employment records, Korean income, and Korean credit history to help qualified borrowers purchase a home much sooner.

If you’re a Korean citizen, newcomer, or permanent resident looking to buy property in Calgary or anywhere in Canada, exploring these specialized mortgage programs could open the door to homeownership sooner than expected.

Author Bio

Mark Herman, MBA is a Calgary mortgage broker with 22 years of experience helping Canadians, newcomers, business owners, and foreign-income borrowers secure mortgage financing. With an MBA in Finance, Mark specializes in finding mortgage solutions that traditional lenders often overlook, including programs for international buyers and families with foreign income.

Should You Replace Poly B Before Selling in Alberta?

Should You Replace Poly B Plumbing Before Selling Your Home in Alberta?

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

If you’re selling a home with Poly B plumbing in Alberta, you’re facing a key decision:

Replace it now—or let buyers deal with it?

The answer can significantly impact your sale price, time on market, and deal success rate.

How Poly B Affects Selling Your Home

Poly B creates:

- Buyer hesitation

- Financing complications

- Insurance concerns

Full buyer-side breakdown:

→ https://markherman.ca/how-to-buy-a-home-in-alberta-with-poly-b-plumbing/

Option 1: Replace Poly B Before Listing

Pros:

- Higher sale price

- More buyer interest

- Fewer deal conditions

Cons:

- Upfront cost

- Renovation hassle

Option 2: Sell As-Is With Poly B

Pros:

- No upfront cost

- Faster listing

Cons:

- Lower offers

- More failed deals

- Smaller buyer pool

What the Calgary Market Typically Does

Most sellers:

- Do NOT replace upfront

- Accept a negotiated discount

How Much Value Does Replacement Add?

Typical:

- Replacement cost: $8K–$20K

- Value increase: often similar or slightly higher

But the real benefit is:

Deal certainty

When You SHOULD Replace Poly B

- Competitive market

- Higher-end home

- You want top dollar

When You SHOULDN’T Replace It

- Entry-level home

- Investor buyers

- Fast sale priority

Negotiation Strategy for Sellers

If not replacing:

- Price slightly below market

- Be transparent upfront

- Expect inspection-based negotiation

Pricing strategy guide:

→ https://markherman.ca/home-appraisal-alberta/

FAQ

Do buyers always ask for a discount?

Almost always.

Does Poly B stop homes from selling?

No—but it narrows the buyer pool.

Bottom Line

Replacing Poly B doesn’t always increase profit—but it often increases certainty and speed.

Author Bio

Mark Herman is a Calgary mortgage broker with 22 years of experience helping sellers and buyers navigate complex property issues.

What Income Do You Need to Buy a House in Calgary? Real Examples

How Much Income Do You Need to Buy a House in Calgary?

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

One of the first questions many home buyers ask is:

“How much income do I need to buy a house in Calgary?”

Quick Answer (Snippet Call-Out)

In Calgary, a household earning about $100,000 per year can typically afford a home between $450,000 and $500,000, assuming a 5–10% down payment, good credit, minimal debt, and current Canadian mortgage stress test rules.

The exact number depends on several factors including your down payment, existing debts, and the mortgage rate used in the stress test.

Below are realistic examples based on typical Calgary home buying scenarios.

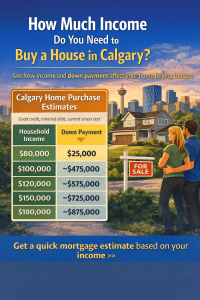

Example chart showing estimated home prices in Calgary based on household income and typical mortgage approval guidelines.

Example: Income vs Home Price in Calgary

These examples assume:

-

Good credit

-

Minimal debt

-

25-year amortization

-

Current Canadian mortgage stress test rules

-

Average Calgary property taxes

| Household Income | Down Payment | Estimated Purchase Price |

|---|---|---|

| $80,000 | $25,000 | ~$400,000 |

| $100,000 | $30,000 | ~$475,000 |

| $120,000 | $40,000 | ~$575,000 |

| $150,000 | $60,000 | ~$725,000 |

| $180,000 | $80,000 | ~$875,000 |

Calgary remains one of the more affordable major cities in Canada, which is why many first-time buyers are surprised by how much home they may qualify for.

How Mortgage Lenders Calculate Affordability in Canada

Canadian lenders use two main ratios to determine mortgage affordability.

Gross Debt Service (GDS)

Gross Debt Service measures the percentage of your income that goes toward housing costs.

Housing costs include:

-

mortgage payment

-

property taxes

-

heating costs

-

condo fees (if applicable)

Most lenders require GDS to stay below 39% of gross income.

Total Debt Service (TDS)

Total Debt Service includes all other monthly debts such as:

-

car loans

-

student loans

-

credit cards

-

lines of credit

Most lenders require TDS below 44% of income.

If your debts are higher, your mortgage approval amount may decrease.

The Mortgage Stress Test Explained

All insured mortgages in Canada must pass the mortgage stress test.

This means buyers must qualify at:

-

the contract mortgage rate or

-

the government qualifying rate

whichever is higher.

The stress test ensures borrowers can still afford payments if interest rates rise.

How Your Down Payment Changes Your Buying Power

Your down payment affects both your approval amount and whether mortgage insurance is required.

Minimum down payment rules in Canada:

-

5% on the first $500,000

-

10% on the portion between $500,000 and $999,999

-

20% for homes $1 million or higher

Many Calgary first-time buyers purchase homes using 5% down payment programs.

How Debt Affects Mortgage Approval

Existing debt can significantly reduce borrowing power.

Example:

| Monthly Debt | Approximate Mortgage Reduction |

|---|---|

| $300 car payment | ~$60,000 less borrowing power |

| $600 debt payments | ~$120,000 less borrowing power |

Paying down consumer debt before applying for a mortgage can dramatically increase your approval amount.

Calgary First-Time Buyers Often Qualify Sooner Than Expected

Many buyers assume they need a very high income before purchasing their first home.

However, programs such as:

-

insured mortgages

-

5% down payments

-

extended amortizations

allow buyers to enter the Calgary housing market earlier than they expect.

Calgary Mortgage FAQ

What salary do you need to buy a house in Calgary?

Most buyers need a household income between $90,000 and $120,000 to comfortably afford homes priced between $450,000 and $600,000, depending on their down payment and debt levels.

Can I buy a house in Calgary with $80k income?

Yes. Buyers earning around $80,000 per year may qualify for homes around $375,000 to $425,000, assuming minimal debt and a typical down payment.

How much mortgage can I qualify for in Calgary?

Most lenders allow housing costs up to 39% of gross income and total debts up to 44% of income, subject to the mortgage stress test.

Get a Personalized Mortgage Estimate

Online examples are helpful, but every mortgage approval depends on:

-

income structure

-

employment history

-

credit score

-

debt levels

-

down payment

If you want a personalized estimate of how much house you could afford in Calgary, feel free to reach out.

I’m happy to review your situation and give you a realistic price range before you start house hunting.

Author

Mark Herman, MBA

Mortgage Broker – 22 Years of Experience

Mark helps Calgary home buyers navigate mortgage approvals, complex income situations, and lender options. His goal is to help clients secure the right mortgage strategy before they start shopping for a home.

Stress Test Continues; Was Almost Abolished

Yes, the Stress Test was almost done away with but it continues.

It seems to be a good thing that all the mortgages since 2018 have been “stress tested” at 5.25%. Now that we are in the middle of 3.6 million mortgages renewing over an 18 month period we find that most everyone is able to make their new mortgage payments after renewal.

Mortgage Mark Herman, MBA in Finance and 22 years experience as a mortgage broker in Western Canada

Nerd alert here!!

OSFI has also determined that loan-to-income (LTI) limits on each institution’s mortgage portfolio will remain in place, alongside the existing stress test.

LTI limits have been in place since each institution’s 2025 fiscal year start and are reported on a quarterly basis.

This is a limit on the volume of newly originated uninsured mortgage loans, at that financial institution, that exceed a 4.5x loan-to-income multiple. This is not a limit on each individual loan.

This measure was introduced in an effort to lessen the build-up of highly leveraged residential mortgage borrowers.

Background

Canada’s federal mortgage stress test began on January 1, 2018, when the Office of the Superintendent of Financial Institutions (OSFI) introduced it for uninsured mortgages.

Key Details of the Stress Test

- Introduced: January 1, 2018

- Regulator: OSFI (Office of the Superintendent of Financial Institutions)

- Applies to: Uninsured mortgages (20%+ down payment) at federally regulated lenders

- Purpose: Ensure borrowers can afford payments at a higher qualifying rate than their contract rate

Mortgage Renewals – 2.75 million Canadian Mortgage Renewals Before 2028!!

Mortgage Stress Test: Why It’s Protecting Homeowners Ahead of the 2026 Renewal Wave

If you locked in your mortgage around 2% five years ago, you probably remember grumbling about the federal “stress test.” At the time, qualifying at 5.25% felt unnecessary — almost punitive. Fast forward to today, and that very safeguard is proving to be one of the smartest policies in Canadian housing finance.

The Renewal Wave Is Coming

According to the latest CMHC report, Canada is heading into a busy period of mortgage renewals:

- 750,000 mortgages will renew in the second half of 2025

- Over 1 million more in 2026

- 940,000 in 2027

Even though the Bank of Canada has cut rates nine times since its peak tightening cycle, borrowing costs remain much higher than they were during the pandemic lows. In fact, the average five-year fixed uninsured mortgage rate in July 2025 was still 67% higher than five years earlier.

“Banks are ready for the almost 3 million mortgage renewals before 2028. Lets get you a strategy on how to get the best rates on your renewal. Its a quick 10 minute phone call and we usually send you back to your own bank with the data you need to get a better rate from them OR we can move you to a bank that does get you better rates.”

Mortgage Mark Herman, Top Calgary Mortgage Broker for renewal advice

Stress Test Success

Here’s the good news: borrowers who qualified at 5.25% back in 2020 are now proving resilient. The stress test ensured they could handle payments at rates much higher than what they actually received. That foresight is paying off:

- National mortgage delinquency rates fell in Q2 2025 — the first decline since 2022.

- While Ontario and BC saw arrears climb (reflecting higher property values and loan sizes), the overall system is holding steady.

- Fears of a “renewal cliff” have eased, thanks to both the stress test and recent rate cuts.

What This Means for You

If your mortgage is coming up for renewal in 2026, now is the time to plan. Options like refinancing, adjusting amortization, or exploring different products can help smooth the transition. The stress test gave you a buffer — but proactive planning will maximize your financial flexibility.

Call to Action: If your mortgage is set to renew in the next 12–18 months, let’s talk strategy. As a mortgage broker, I specialize in helping clients navigate renewals, refinances, and complex lending scenarios. Call me today to review your options and make sure you’re ready for what’s ahead.

Using cryptocurrency to buy a home in Canada: 2025

We have been getting lots of customers asking this question with the recent rise of crypto values.

Below are ALL the details I have collected: from tax implications to AML compliance, what buyers need to know before turning digital gold into a home.

I have bitcoins for my down payment on my home!

Many Canadians now have significant Bitcoin, Ethereum or other crypto and want to use that for the down payment in a home purchase.

However, turning crypto into a viable down payment, or leveraging it as collateral, isn’t nearly as simple as it sounds.

Mortgage Mark Herman, Best Calgary Alberta mortgage broker for crypto mortgage brokers and first time home buyers

First, what is a crypto mortgage?

Crypto mortgages typically fall into one of two categories:

- Crypto-funded mortgage – the way that actually works: You sell your crypto, convert it to Canadian dollars, and use those funds as your down payment. This way also comes with some with tax consequences on the sale – but hey, your crypto may be up 15000%, and the capital gains tax is only on the amount you cash in, and it is 50% of the profit. SEE THE MATH ON THIS at the bottom.

- Crypto-backed mortgage – what everyone is asking for: You pledge your crypto as collateral without selling it. This probably helps avoid triggering capital gains tax, but requires a lender capable of assessing and managing that risk. We have not found this route to work due to enormous anti-money-laundering laws that realtors, banks, and brokers have to follow.

Version 1: Using your crypto as a mortgage down payment

This is the way that works, and the easiest way to use your crypto is to cash it in/ convert to cash, and move the funds into a Canadian bank account to “seed” or “season” for 90 days.

- This is not really needed with most other assets and we have tried so many ways to get the lenders to accept the funds held in a crypto trading platform (like Binance, NDAX or similar, but they always sound the alarm right here, send the file to “the risk desk” and then it is a battle the entire rest of the way.

Why do I need to cash it in and leave it in the bank for 90 days? It’s AML!

The “kink in the system” is that we have to show a 90 day history for the source of all down payment funds for AML – anti money laundering law compliance. Normally banks are fine with funds sitting in Wealth simple or any trading account but NOT for crypto. After getting “all the NO’s” we found this is the way to go.

What about – buying with cash and refinancing/ getting a mortgage on it later?

- When you do this in the 1st year, the banks still need to re-verify the original down payment for the original purchase so this will still be tough to do.

- And refinance rates are higher than purchase rates, and you would then also be re-registering the mortgage and registration has shot up to about $2000, from $200 over the last year in Alberta.

Version 2: which we have NOT found to work – is leveraging your crypto and pledging it without a sale.

If you want to access liquidity without selling your crypto, a crypto-backed loan is another option and here is how it is supposed to work to avoid the capital gains event.

- If this has too many moving parts, then selling your crypto and putting it into the bank for 90 days is the way to go.

- Deposit crypto as collateral

You transfer your crypto to a platform, where it is held in a secure wallet or smart contract. Platforms such as YouHodler and Ledn support this model.

- Loan-to-value (LTV) ratio

You can typically borrow between 30% and 70% of your crypto’s value. For example, pledging $10,000 worth of Bitcoin may get you a $5,000 loan.

- Disbursement

Loans are issued in fiat (e.g., CAD, USD) or stablecoins. Most do not require a credit check and can be approved quickly.

- Repayment and interest

Terms vary. Some platforms offer flexible repayment options; others require fixed schedules. Once the loan and interest are repaid, your crypto is returned.

- Liquidation risk

If the value of your crypto drops and your LTV exceeds a certain threshold, you may be required to add collateral. Otherwise, your crypto may be liquidated.

- No taxable event

Since you are borrowing, not selling, there is no capital gains tax event. This can be beneficial from a tax-planning perspective.

WHAT ALSO WORKS …

A simpler, safer alternative: using crypto ETFs for mortgage planning

For a more straightforward path, consider using crypto ETFs instead of direct crypto holdings. ETFs allow you to gain exposure to digital assets without managing wallets, keys, or exchange accounts.

Held through mainstream brokerages, including in TFSAs and RRSPs, crypto ETFs are easier for lenders to understand and verify, avoiding the friction that often comes with direct crypto assets.

Leading crypto ETFs in Canada

These are some of the top crypto ETFs available to Canadian investors:

- BTCC (Purpose Bitcoin ETF): The first Canadian Bitcoin ETF, with CAD and USD options and a carbon-neutral version

- BTCQ (3iQ CoinShares Bitcoin ETF): Physically-backed BTC, held in cold storage

- FBTC (Fidelity Advantage Bitcoin ETF): Designed for registered accounts

- ETHH and ETHX (Purpose and CI Galaxy Ethereum ETFs): Offer direct ETH exposure, with or without staking

- IBIT (iShares Bitcoin ETF): Managed by BlackRock, a major global asset manager

Several ETFs now include additional exposure to AI stocks or newer crypto assets like Solana, expanding diversification options within this space.

Naturally, this is our experience and this should NOT be taken as investment advice. Ask your licensed financial adviser for their opinion before proceeding please.

SUMMARY

Can I use crypto as a down payment?

Yes, but there are strict conditions:

- You must convert the crypto to Canadian dollars

- Maintain a documented paper trail of the sale and deposit

- Be prepared to explain the origin of your funds for AML compliance

Many lenders will still be hesitant. Working with a mortgage broker familiar with these requirements and a lender that understands crypto is essential.

Is it legal and safe in Canada?

Yes, but regulatory guidance is evolving.

Lenders must comply with OSFI and FINTRAC standards, which include thorough AML and source-of-funds verification.

OSFI is expected to implement new digital asset rules in 2025, which may influence how Canadian financial institutions handle crypto-collateralized products.

Key risks to consider

- Price volatility: A drop in crypto value can lead to margin calls or liquidation

- Lender restrictions: Many banks still reject crypto-related funds

- Platform risk: Some crypto lenders have gone bankrupt

- No deposit insurance: Crypto held as collateral is not insured by CDIC

- Compliance complexity: Documentation, tax reporting, and regulatory scrutiny can be significant

How does CRA treat crypto in mortgage scenarios?

Under CRA guidelines, cryptocurrency is treated as a commodity.

Selling it to fund a down payment is a taxable event, and any capital gains must be reported.

However, borrowing against your crypto is not a disposition and does not trigger capital gains taxes, at least under current rules. Regardless, thorough documentation is critical.

Crypto-backed mortgages and crypto-collateralized loans offer new possibilities, but they’re not ideal for everyone. If you’re a crypto holder considering homeownership in Canada:

- Convert your crypto to Canadian dollars early, and let it seed for at least 90 days

- Alternatively, accumulate your crypto wealth in Exchange Traded Funds

- Document everything: sales, transfers, deposits, and sources of funds

- Work with professionals who understand both traditional lending and crypto

- Be ready to meet rigorous compliance and verification requirements

Canada’s mortgage landscape is still catching up to the digital asset world. Planning ahead is key to avoiding delays or declined applications.

Further reading and sources

Taxable Capital Gains on Bitcoin in Canada

When you dispose of Bitcoin (for example, selling or “cashing in”), the Canada Revenue Agency treats it as a commodity. If your transaction is considered a capital disposition, only 50% of the gain is taxable.

How It’s Calculated

- Adjusted Cost Base (ACB): The original purchase price (in CAD), plus any fees.

- Proceeds of Disposition: Fair market value (in CAD) on the date you sell.

- Capital Gain:

Gain=Proceeds−ACB−Disposal Fees\text{Gain} = \text{Proceeds} – \text{ACB} – \text{Disposal Fees}

- Taxable Capital Gain:

For example, if you bought Bitcoin for $10,000 CAD and later sold it for $15,000 CAD (with $100 fees), your gain is $15,000 – $10,000 – $100 = $4,900. You report half—$2,450—as taxable income.

Tax Payable

- The $2,450 is added to your total income for the year.

- The actual tax you owe equals your marginal tax rate multiplied by the taxable gain.

Municipal, provincial and federal rates all apply, so total tax varies by province and your income bracket.

Reporting & Recordkeeping

- Report on Schedule 3 (Capital Gains) of your T1 return.

- Keep detailed records: transaction dates, CAD valuations, fees and wallet addresses.

- Use reliable crypto-tax software or a professional to ensure accuracy.

Special Considerations

- If CRA deems your activity a business (frequent trading, mining, or providing services), 100% of profits may be taxed as business income.

- Capital losses can offset gains—claim them on Schedule 3 to reduce your taxable gain.

Beyond capital gains, remember that receiving Bitcoin as income (mining rewards, staking, payments) is taxed at 100% of its fair market value on receipt. Always consult a tax professional for personalized advice

Summer is here!

Our 55+ clients are thinking about ways to refresh their homes.

Whether it’s for comfort, safety, or curb appeal, renovations can get pricey and the CHIP reverse mortgage can really help out.

Mortgage Mark Herman, CHIP and Reverse Mortgage specialist, here to help the 55+ home owners.

The CHIP Reverse Mortgage by HomeEquity Bank can help you access the funds you need—tax-free and with no monthly mortgage payments required.

Here are just a few popular spring projects our recent customers have been planning:

- Retrofitting their home to support aging in place

- Resealing windows and doors for better energy efficiency

- Landscaping makeovers to enhance privacy and beauty

- Adding an outdoor kitchen and seating area for entertaining

- Repaving the driveway to boost curb appeal

With the CHIP Reverse Mortgage, you can unlock up to 55% of your home’s equity, giving you the freedom to renovate now and enjoy the results for years to come—all without dipping into your retirement savings.

Looking for tips on how use the CHIP in renovations? Call or email me, I’d be happy to help!

Canadian Mortgage Economic Data, June 4th, 2025

The Bank of Canada announced today that it is keeping its benchmark interest rate at 2.75%, unchanged from April (and March) of 2025.

As noted under “Rationale”, the Bank appears to be in a holding pattern until it gains more information on the direction of US trade policy and its impact on Canada.

Below, is a summary of the Bank’s observations and its outlook.

Summary – the 5-year fixed is the best option for June 2025 and July 2025 so far. ensure you get a rate hold are rates are creeping up.

Mortgage Mark Herman, top Calgary Mortgage Broker for First Time Buyers

Canadian Economic Performance, Housing, Employment and Outlook

- Economic growth in the first quarter came in at 2.2%, slightly stronger than the Bank had forecast, while the composition of GDP growth was largely as expected

- The pull-forward of exports to the United States and inventory accumulation boosted activity, with final domestic demand “roughly flat”

- Strong spending on machinery and equipment held up growth in business investment by more than expected

- Consumption slowed from its very strong fourth-quarter pace, but continued to grow despite “a large drop” in consumer confidence

- Housing activity was down, driven by a sharp contraction in resales; government spending also declined

- The labour market has weakened, particularly in trade-intensive sectors, and unemployment has risen to 6.9%

- The economy is expected to be considerably weaker in the second quarter, with strength in exports and inventories reversing and final domestic demand remaining subdued

Canadian Inflation

- Inflation eased to 1.7% in April, with the elimination of the federal consumer carbon tax shaving 0.6 percentage points off the Consumer Price Index

- Excluding taxes, inflation rose 2.3% in April, slightly stronger than the Bank had expected

- The Bank’s preferred measures of core inflation, as well as other measures of underlying inflation, moved up

- Recent surveys indicate that households continue to expect that tariffs will raise prices and many businesses say they intend to pass on the costs of higher tariffs

- The Bank will be watching all of these indicators closely to gauge how inflationary pressures are evolving

Global Economic Performance

- While the global economy has shown resilience in recent months, this partly reflects a temporary surge in activity to get ahead of tariffs

- In the United States, domestic demand remained relatively strong but higher imports pulled down first-quarter GDP

- US inflation has ticked down but remains above 2%, with the price effects of tariffs still to come

- In Europe, economic growth has been supported by exports, while defence spending is set to increase

- China’s economy has slowed as the effects of past fiscal support fade; more recently, high tariffs have begun to curtail Chinese exports to the US

- Since financial market turmoil in April, risk assets have largely recovered and volatility has diminished, although markets remain sensitive to US policy announcements

- Oil prices have fluctuated but remain close to their levels at the time of the April Monetary Policy Report

Rationale

With uncertainty about US tariffs still high, the Canadian economy softer but not sharply weaker, and some unexpected firmness in recent inflation data, the Bank’s Governing Council decided to hold the policy rate steady “as we gain more information on US trade policy and its impacts.

Looking Ahead: Uncertainty Remains High

The Bank noted that since its April Monetary Policy Report, the US administration has continued to increase and decrease various tariffs. China and the United States have stepped back from extremely high tariffs and bilateral trade negotiations have begun with a number of countries. However, the Bank said the outcomes of these negotiations “are highly uncertain,” tariff rates are well above their levels at the beginning of 2025, and new trade actions are still being threatened. Uncertainty remains high.

As a result, the Bank says it is proceeding carefully, with particular attention to the risks and uncertainties facing the Canadian economy. These include: the extent to which higher US tariffs reduce demand for Canadian exports; how much this spills over into business investment, employment and household spending; how much and how quickly cost increases are passed on to consumer prices; and how inflation expectations evolve.

Final comments

Today’s announcement ended with the following statement from the Bank’s Governing Council: “We are focused on ensuring that Canadians continue to have confidence in price stability through this period of global upheaval. We will support economic growth while ensuring inflation remains well controlled.”

Next scheduled BoC rate announcement

The Bank is scheduled to make its fifth policy interest rate decision of 2025 on July 9th.

GST Rebate for 1st Time Home Buyers

We have had lots of questions about this proram.

The legislation has been tabled, but is not done yet. As of today, and it is for contracts written May 27, 2025 or later.

Updates as they come in.

We have a 4-plex buyer who is purchasing a newly constructed 4-plex in Calgary at $1,250,000. His rebate is about 60k – now that is now pretty substantial!

Mortgage Mark Herman, 1st time buyer and move up mortgage specialist in Calgary Alberta.

Bank of Canada Lowers Consumer Prime to 4.95%

The Bank of Canada lowers its benchmark interest rate to 2.75%

In the face of significant geopolitical tensions, the Bank of Canada announced today that it has lowered its policy interest rate by 25 basis points. This marks the seventh reduction since June of 2024.

Below, we summarize the Bank’s commentary.

Canadian Economic Performance and Housing

- Canada’s economy grew by 2.6% in the fourth quarter of 2024 following upwardly revised growth of 2.2% in the third quarter

- This “growth path” is stronger than was expected when the Bank last reported in January 2025

- Past cuts to interest rates have boosted economic activity, particularly consumption and housing

- However, economic growth in the first quarter of 2025 will likely slow as the intensifying trade conflict weighs on sentiment and activity

- Recent surveys suggest a sharp drop in consumer confidence and a slowdown in business spending as companies postpone or cancel investments

- The negative impact of slowing domestic demand has been partially offset by a surge in exports in advance of tariffs being imposed

- The Canadian dollar is broadly unchanged against the US dollar but weaker against other currencies

Canadian Inflation and Outlook

- Inflation remains close to the Bank’s 2% target

- The temporary suspension of the GST/HST lowered some consumer prices, but January’s Consumer Price Index was “slightly firmer” than expected at 1.9%

- Inflation is expected to increase to about 2.5% in March with the end of the tax break

- The Bank’s preferred measures of core inflation remain above 2%, mainly because of the persistence of shelter price inflation

- Short-term inflation expectations have risen in light of fears about the impact of tariffs on prices

Canadian Labour Market

- Employment growth strengthened in November through January and the unemployment rate declined to 6.6%

- In February, job growth stalled

- While past interest rate cuts have boosted demand for labour in recent months, there are warning signs that heightened trade tensions could disrupt the recovery in the jobs market

- Meanwhile, wage growth has shown signs of moderation

Global Economic Performance, Bond Yields and the Canadian Dollar

- After a period of solid growth, the US economy looks to have slowed in recent months, but US inflation remains slightly above target

- Economic growth in the euro zone was modest in late 2024

- China’s economy has posted strong gains, supported by government policies

- Equity prices have fallen and bond yields have eased on market expectations of weaker North American growth

- Oil prices have been volatile and are trading below the assumptions in the Bank’s January Monetary Policy Report

Rationale for a rate cut

While the Bank offered that economic growth came in stronger than it expected, the pervasive uncertainty created by continuously changing US tariff threats is restraining consumers’ spending intentions and businesses’ plans to hire and invest. Against this background, and with inflation close to the 2% target, the Bank decided to reduce its policy rate by 25 basis points.

Outlook

The Bank notes that the Canadian economy entered 2025 “in a solid position,” with inflation close to its 2% target and “robust” GDP growth. However, heightened trade tensions and tariffs imposed by the United States will likely slow the pace of economic activity and increase inflationary pressures in Canada. The economic outlook continues to be subject to more-than-usual uncertainty because of the rapidly evolving policy landscape.

Final comments

The Bank noted that monetary policy “cannot offset the impacts of a trade war.” What monetary policy “can and must do” is ensure that higher prices do not lead to ongoing inflation.

The Bank said it will carefully assess: i) the timing and strength of both the downward pressures on inflation from a weaker economy and ii) the upward pressures on inflation from higher costs. It will also closely monitor inflation expectations.

It ended its statement by saying it is committed to maintaining price stability for Canadians.

More scheduled BoC news

The Bank is scheduled to make its third policy interest rate decision of 2025 on April 16th.