Korean Mortgage in Canada Using Korean Income & Credit History | Calgary Mortgage Broker

Korean Home Buyers in Canada: Get a Mortgage Using Korean Income, Korean Tax Documents, and Korean Credit History

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience specializing in unique and difficult to do deals.

Buying a home in Canada can be challenging if you recently arrived from Korea or still earn most of your income there. Many (as in ALL) of the traditional Canadian lenders (Big6- banks) require extensive Canadian employment history, Canadian tax returns, and established Canadian credit.

The good news is that there are specialty lenders in Canada that understand the needs of Korean home buyers and can approve mortgages using Korean income, Korean employment documents, and even Korean credit reports.

If you’re a Korean citizen, permanent resident, or newcomer to Canada, this specialized mortgage program may help you qualify sooner than you think.

Can I Get a Canadian Mortgage Using Korean Income?

Yes!!

Certain specialty lenders in Canada work specifically with Korean borrowers and can evaluate income earned in Korea. Instead of relying solely on Canadian tax returns and Canadian employment history, these lenders can review:

- Korean tax documents

- Korean employment verification

- Korean pay records

- Korean credit reports

- Korean property ownership documents

This can be especially valuable for:

- New immigrants from Korea

- Permanent residents who recently moved to Canada

- Families with income earned in Korea

- Professionals working for Korean companies

- Individuals relocating to Calgary or other Canadian cities

“Our Korean customers were just as surprised as I was when we found that we can do a mortgage for them, in Canada, using their existing documents from Korea!”

Mortgage Mark Herman, MBA mortgage broker in Calgary specializing in new buyers from Korea

What Documents Are Required?

For Husband and Wife Applicants

The lender typically requires:

Income Verification

2024 and 2025 Certificate of Income from the National Tax Service of Korea (국세청)

These documents help verify historical income earned in Korea.

Employment Verification

Letter of Employment (재직증명서)

The employment letter confirms position, employment status, and employer information.

Income Evidence

- Most recent three pay stubs (급여명세서)

- Three months of direct deposit history

These documents help confirm current earnings and consistency of income.

Existing Property Information

If the applicants own property in Korea:

- Current mortgage statement

- Property tax statement

These documents allow the lender to calculate any existing debt obligations.

For Adult Children Who May Be Co-Signing or On the Mortgage

If an adult child is participating in the application, lenders may require:

- Letter of employment

- Recent pay stubs

- Three months of direct deposit history

- Most recent Notice of Assessment (NOA)

- Proof of no tax owing

Identification Requirements

- Passport

- Driver’s license

- Korean Passport

- Canadian Permanent Resident Card

- Korean Resident Registration Card (주민등록증)

Korean Credit Report

One unique feature of this program is that the lender can often obtain and review a Korean credit report directly.

Applicants will generally be required to sign a credit consent form authorizing the Korean credit search.

How Does the Lender Calculate Foreign Income?

The lender uses a specific formula to determine qualifying income:

Foreign Income = (Gross Foreign Income – Foreign Debt Service) × Recognition Ratio (80%) × Exchange Rate

This means:

- Gross Korean income is reviewed.

- Existing debt obligations are deducted.

- The lender recognizes 80% of the remaining income.

- The income is converted to Canadian dollars using the applicable exchange rate.

Example of Foreign Income Qualification

Let’s assume:

- Annual Korean income: CAD equivalent of $150,000

- Existing Korean debt payments: $20,000 annually

Calculation:

- $150,000 − $20,000 = $130,000

- $130,000 × 80% = $104,000 qualifying income

In this example, the lender would use approximately $104,000 of qualifying income for mortgage approval purposes.

104k income gets about a $425,000 mortgage amount (+ down payment = purchase price)

Important Translation Requirements

All Korean documents must be accompanied by English translations.

Applicants should submit:

- Original Korean documents

- Certified English translations

Providing complete translations early in the process can help avoid delays and speed up approval.

Conditions of Financing Needs to be 14 Days.

This mortgage program requires additional underwriting compared to a standard Canadian mortgage.

Borrowers should allow approximately two weeks for the lender to review the Certificate of Income documents and complete the approval process.

If you are planning to purchase a home, it is important to start the mortgage application early so financing is ready before you remove conditions.

Why Work With a Mortgage Broker Familiar With Korean Mortgage Programs?

Not every mortgage broker understands foreign-income lending or Korean documentation requirements.

An experienced broker can help:

- Review Korean income documents

- Coordinate English translations

- Calculate qualifying income accurately

- Structure the application properly

- Navigate specialty lender requirements

- Avoid unnecessary delays

For Korean families buying property in Calgary and throughout Canada, working with a broker who understands these programs can significantly improve the approval process.

Frequently Asked Questions

Can I qualify for a mortgage in Canada without Canadian income?

Yes. Some specialty lenders can use Korean income and Korean employment documents to qualify borrowers.

Can a lender use my Korean credit report?

Yes. Certain lenders can obtain and review Korean credit reports with your written authorization.

Do my Korean documents need to be translated?

Yes. All Korean documents must be submitted with English translations.

How long does approval take?

Borrowers should generally allow at least two weeks for the lender to review foreign income documentation and issue approval.

Can permanent residents use this program?

Yes. Permanent residents with Korean income may qualify, depending on the lender’s guidelines.

Final Thoughts

Many Korean families assume they must wait years to build Canadian credit and employment history before buying a home.

In reality, some Canadian lenders can use Korean tax documents, Korean employment records, Korean income, and Korean credit history to help qualified borrowers purchase a home much sooner.

If you’re a Korean citizen, newcomer, or permanent resident looking to buy property in Calgary or anywhere in Canada, exploring these specialized mortgage programs could open the door to homeownership sooner than expected.

Author Bio

Mark Herman, MBA is a Calgary mortgage broker with 22 years of experience helping Canadians, newcomers, business owners, and foreign-income borrowers secure mortgage financing. With an MBA in Finance, Mark specializes in finding mortgage solutions that traditional lenders often overlook, including programs for international buyers and families with foreign income.

Should You Replace Poly B Before Selling in Alberta?

Should You Replace Poly B Plumbing Before Selling Your Home in Alberta?

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

If you’re selling a home with Poly B plumbing in Alberta, you’re facing a key decision:

Replace it now—or let buyers deal with it?

The answer can significantly impact your sale price, time on market, and deal success rate.

How Poly B Affects Selling Your Home

Poly B creates:

- Buyer hesitation

- Financing complications

- Insurance concerns

Full buyer-side breakdown:

→ https://markherman.ca/how-to-buy-a-home-in-alberta-with-poly-b-plumbing/

Option 1: Replace Poly B Before Listing

Pros:

- Higher sale price

- More buyer interest

- Fewer deal conditions

Cons:

- Upfront cost

- Renovation hassle

Option 2: Sell As-Is With Poly B

Pros:

- No upfront cost

- Faster listing

Cons:

- Lower offers

- More failed deals

- Smaller buyer pool

What the Calgary Market Typically Does

Most sellers:

- Do NOT replace upfront

- Accept a negotiated discount

How Much Value Does Replacement Add?

Typical:

- Replacement cost: $8K–$20K

- Value increase: often similar or slightly higher

But the real benefit is:

Deal certainty

When You SHOULD Replace Poly B

- Competitive market

- Higher-end home

- You want top dollar

When You SHOULDN’T Replace It

- Entry-level home

- Investor buyers

- Fast sale priority

Negotiation Strategy for Sellers

If not replacing:

- Price slightly below market

- Be transparent upfront

- Expect inspection-based negotiation

Pricing strategy guide:

→ https://markherman.ca/home-appraisal-alberta/

FAQ

Do buyers always ask for a discount?

Almost always.

Does Poly B stop homes from selling?

No—but it narrows the buyer pool.

Bottom Line

Replacing Poly B doesn’t always increase profit—but it often increases certainty and speed.

Author Bio

Mark Herman is a Calgary mortgage broker with 22 years of experience helping sellers and buyers navigate complex property issues.

Buying a Home With Poly B Plumbing in Alberta (2026 Guide)

Buying a Home in Alberta With Poly B Plumbing (2026 Guide for Buyers & Sellers)

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

Buying a home with Poly B plumbing in Alberta can feel like a deal-breaker—but it doesn’t have to be. The reality is that thousands of homes in Calgary and across Alberta still have Poly B, and many are financed every year.

The key is understanding the risks, how lenders and insurers view it, and how to structure your purchase properly.

What Is Poly B Plumbing?

Poly B (polybutylene) is a grey plastic piping used in homes built roughly between 1978 and the mid-1990s.

It was popular because it was:

- Cheap

- Easy to install

- Flexible

Unfortunately, it turned out to have serious long-term reliability issues.

There are still hundreds of thousands of homes across Canada with Poly B, especially in Alberta.

Why Poly B Plumbing Is a Problem

Poly B isn’t just “older plumbing”—it’s considered high-risk plumbing.

Key issues:

- Internal deterioration from chlorine in water

- Brittle pipes that crack over time

- Leaks that start inside walls (hard to detect)

- Sudden pipe failures without warning

In Alberta, the problem can be worse due to:

- Temperature swings

- Water chemistry

- Aging housing stock

This combination leads to:

- Water damage

- Mold issues

- Expensive repairs

How to Tell If a Home Has Poly B

Look for:

- Grey (sometimes blue/black/white) plastic pipes

- Markings like “PB2110”

- Visible piping near:

- Hot water tank

- Basement ceiling

- Under sinks

If the home was built between 1980–1995, there’s a strong chance it has Poly B.

Can You Get a Mortgage on a Home With Poly B in Calgary Alberta?

Yes—but it depends on the lender and the overall deal.

Most lenders will:

- Still approve the mortgage

- Focus more on:

- Property value

- Down payment

- Borrower strength

However…

The real issue is insurance (not the mortgage)

The Insurance Problem (This Is What Actually Kills Deals)

Insurance companies are the biggest hurdle.

Many insurers:

- Refuse coverage entirely

- Require full replacement before closing

- Or charge higher premiums

Without insurance, your mortgage cannot fund. SURPRISE – we DO have access to insurance companies that will cover Poly B at normal rates!

This is the #1 reason Poly B deals fall apart.

Typical Solutions for Buyers

1. Replace Poly B Before Closing

- Seller completes replacement

- Cleanest solution for financing

- Helps protect property value

2. Negotiate a Price Reduction

- Buyer takes on replacement cost

- Common in Calgary market

- Requires lender + insurer alignment

3. Insurance Exception Strategy

- Some insurers still accept Poly B (case-by-case)

- Often requires:

- Inspection

- No existing leaks

How Much Does It Cost to Replace Poly B?

Typical cost range:

- $3,000 to $25,000+ depending on home size

Factors:

- Square footage

- Accessibility

- Whether walls need repair afterward

Most homeowners replace with:

- PEX

- Copper

Does Poly B Affect Home Value in Alberta?

Yes—but not always dramatically.

What happens in the market:

- Buyers use it as a negotiation tool

- Some walk away entirely

- Others expect a discount

In practice:

- Homes still sell

- But usually with pricing adjustments

Should You Buy a Home With Poly B?

It depends on your situation.

You should consider it if:

- The price reflects the risk

- You have a plan to replace it

- Insurance is confirmed upfront

You should avoid it if:

- Insurance is unclear

- Budget is tight

- You want a “turnkey” home

Mortgage Strategy Tips (This Is Where You Win or Lose the Deal)

As a mortgage broker, this is where I see deals succeed—or fail.

Key strategies:

- Confirm insurance FIRST (before removing conditions)

- Work with a broker who understands:

- Lender flexibility

- Insurance workarounds

- Budget replacement into your financing plan

Real Example (Calgary Scenario)

Purchase price: $500,000

Poly B replacement estimate: $12,000

Negotiation:

- Buyer reduces offer to $488,000

- Uses savings to replace plumbing after closing

Result:

- Deal goes through

- Property value protected long-term

Bottom Line

Poly B isn’t a deal killer—but it is a strategy issue.

Handled correctly:

- You can buy below market value

- Upgrade the home

- Build equity quickly

Handled poorly:

- The deal collapses due to insurance

FAQ (Featured Snippet Section)

Is Poly B plumbing illegal in Alberta?

No, but it is no longer used in new construction and is considered outdated and high-risk.

Can you insure a home with Poly B?

Sometimes—but many insurers restrict or refuse coverage.

Do lenders allow Poly B homes?

Yes. The bigger issue is insurance approval, not the mortgage.

Should I replace Poly B immediately?

Most experts recommend replacement due to unpredictable failure risk.

Final Advice

If you’re considering buying a home with Poly B, don’t guess.

This is one of those situations where:

- The right mortgage strategy saves the deal

- The wrong approach kills it

Author Bio

Mark Herman is a Calgary-based mortgage broker with 22 years of experience and an MBA in Finance. He specializes in helping home buyers navigate complex mortgage situations—including properties with Poly B plumbing, rental income, and non-traditional borrowers.

Divorce and Mortgage Options in Calgary: What to Know Before You Sign

Divorce and Mortgages in Canada: What You Need to Know Before Signing a Separation Agreement

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience, specializing in complicated and standard divorces in Alberta and BC.

Divorce is one of the most stressful financial events you’ll go through. Emotions are high, timelines are tight, and most people just want to get things settled and move on.

But here’s the mistake I see all the time:

People sign separation agreements that unintentionally destroy their ability to qualify for a mortgage afterward.

And by the time they find out—it’s too late. And that is why we have lawyers that send us their drafts of separation agreements so we can ensure that both parties can still buy a home after the agreement is signed.

Why Your Separation Agreement Matters More Than You Think

In Calgary, I regularly get calls from divorce lawyers before agreements are finalized.

Why?

Because experienced lawyers understand something critical:

Just because a separation agreement is legally “fair” doesn’t mean it works from a mortgage perspective.

They want to make sure:

-

Both parties can qualify for financing afterward

-

Support payments aren’t structured in a way that kills borrowing power

-

Debt division doesn’t create unintended consequences

That’s the right approach.

Unfortunately, many people don’t have that conversation until after everything is signed.

Your Mortgage Options During Divorce

Most situations fall into one of four scenarios.

Most people want to do #4, keep the home, increase the mortgage to buy out the ex-partner.

| Scenario | Scenario #1 | Scenario #2 | Scenario #3 | Scenario #4 |

|---|---|---|---|---|

| Overview | Sell your home, no new property | Sell your home, buy another home | Hold onto your home, keep mortgage same | Hold onto your home, increase mortgage |

| What will you do with the existing house? | Sell and not buy another property | Sell and buy another property | Keep | Keep |

| Do you need to take out home equity? | Not applicable | Not applicable | No, sufficient cash to buy out spouse | Yes, need to tap equity to buy out spouse |

| What will happen to your current mortgage? | Pay out existing mortgage | Pay out existing mortgage or port mortgage | Assume or transfer existing mortgage | Refinance existing mortgage |

| Do you need a new mortgage? | No | Yes (unless porting) | No | No (but mortgage increases) |

| Do you need to re-qualify for a mortgage? | Not applicable | Yes | Yes | Yes |

Breaking Down the 4 Common Scenarios

1. Sell the Home and Don’t Buy Again (Yet)

This is the cleanest option financially.

-

Mortgage gets paid out

-

No re-qualification needed

-

You walk away with your share of equity

This works well if you want a reset—but it delays re-entering the market.

2. Sell and Buy Another Home

This is what most people want to do.

But here’s the catch:

You have to fully re-qualify on your own.

That means:

-

Your income must support the new mortgage

-

Any support payments (paid or received) are factored in

-

Debts from the separation count against you

This is where a lot of deals fall apart.

3. Keep the Home and Take Over the Existing Mortgage

This sounds simple—but it’s not automatic.

Even if the lender allows a transfer:

-

You still need to qualify on your own

-

The other spouse must be fully removed from liability

If you can qualify, this is often the least disruptive option.

4. Keep the Home and Refinance (Buy Out Your Ex) – what you probably want to do.

This is very common in Calgary.

You:

-

Refinance the mortgage

-

Pull out equity

-

Use it to buy out your spouse and pay out debts that may also be involved.

But this increases your mortgage balance—and your payment.

So again, you must qualify at the higher amount.

The Biggest Mistake I See (And It’s Costly)

Here’s the real issue:

Someone agrees to:

-

High support payments

-

Taking on too much debt

-

Or an aggressive buyout structure

Then they come to me after the agreement is signed…

…and they can’t qualify for a mortgage anymore.

Not for the home they wanted.

Sometimes not for any home.

How Support Payments Affect Mortgage Approval

This is where things get technical.

If you pay support:

-

It reduces your borrowing power directly

If you receive support:

-

It may help—but only if it’s structured properly

-

Lenders often require consistency and documentation

Not all support income is treated equally.

Why Divorce Lawyers Call Me Before Agreements Are Signed

The better family lawyers in Calgary will loop in a mortgage broker early.

They want to avoid:

-

Structuring payments that make financing impossible

-

Creating agreements that look good on paper but fail in reality

-

Clients getting stuck renting long-term unintentionally

It’s a small step that prevents major problems later.

What You Should Do Before Signing Anything

If you’re going through a separation, do this before finalizing your agreement:

1. Get a Mortgage Feasibility Check

Find out:

-

What you can qualify for today

-

What different scenarios look like

2. Run Multiple Scenarios

Don’t assume one outcome.

Look at:

-

Keeping the home

-

Selling and buying

-

Different support structures

3. Coordinate With Your Lawyer

Your mortgage plan and legal agreement should work together—not against each other.

Calgary-Specific Considerations

In Calgary, this matters even more because:

-

Home prices are still relatively accessible compared to other major cities

-

Many people can buy again—if the structure is right

-

But small changes in income or obligations can make or break approval

Final Thoughts

Divorce is emotional—but your mortgage decisions are purely financial.

And once a separation agreement is signed, you don’t get a do-over.

If you’re in this situation, the best move you can make is simple:

Talk to a mortgage broker before you sign anything.

FAQ: Divorce and Mortgages in Canada

Can I get a mortgage after a divorce?

Yes—but you must qualify on your own, and your separation agreement plays a major role.

Can I keep the house after divorce?

Only if you can qualify for the mortgage independently or refinance to remove your ex.

Do support payments affect mortgage approval?

Yes. Paying support reduces borrowing power; receiving support may help depending on how it’s structured.

Do I need to refinance to remove my spouse?

Often yes, unless the lender allows a transfer and you qualify on your own.

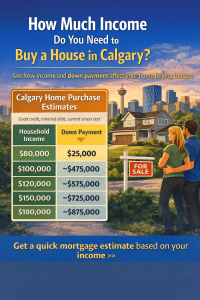

What Income Do You Need to Buy a House in Calgary? Real Examples

How Much Income Do You Need to Buy a House in Calgary?

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

One of the first questions many home buyers ask is:

“How much income do I need to buy a house in Calgary?”

Quick Answer (Snippet Call-Out)

In Calgary, a household earning about $100,000 per year can typically afford a home between $450,000 and $500,000, assuming a 5–10% down payment, good credit, minimal debt, and current Canadian mortgage stress test rules.

The exact number depends on several factors including your down payment, existing debts, and the mortgage rate used in the stress test.

Below are realistic examples based on typical Calgary home buying scenarios.

Example chart showing estimated home prices in Calgary based on household income and typical mortgage approval guidelines.

Example: Income vs Home Price in Calgary

These examples assume:

-

Good credit

-

Minimal debt

-

25-year amortization

-

Current Canadian mortgage stress test rules

-

Average Calgary property taxes

| Household Income | Down Payment | Estimated Purchase Price |

|---|---|---|

| $80,000 | $25,000 | ~$400,000 |

| $100,000 | $30,000 | ~$475,000 |

| $120,000 | $40,000 | ~$575,000 |

| $150,000 | $60,000 | ~$725,000 |

| $180,000 | $80,000 | ~$875,000 |

Calgary remains one of the more affordable major cities in Canada, which is why many first-time buyers are surprised by how much home they may qualify for.

How Mortgage Lenders Calculate Affordability in Canada

Canadian lenders use two main ratios to determine mortgage affordability.

Gross Debt Service (GDS)

Gross Debt Service measures the percentage of your income that goes toward housing costs.

Housing costs include:

-

mortgage payment

-

property taxes

-

heating costs

-

condo fees (if applicable)

Most lenders require GDS to stay below 39% of gross income.

Total Debt Service (TDS)

Total Debt Service includes all other monthly debts such as:

-

car loans

-

student loans

-

credit cards

-

lines of credit

Most lenders require TDS below 44% of income.

If your debts are higher, your mortgage approval amount may decrease.

The Mortgage Stress Test Explained

All insured mortgages in Canada must pass the mortgage stress test.

This means buyers must qualify at:

-

the contract mortgage rate or

-

the government qualifying rate

whichever is higher.

The stress test ensures borrowers can still afford payments if interest rates rise.

How Your Down Payment Changes Your Buying Power

Your down payment affects both your approval amount and whether mortgage insurance is required.

Minimum down payment rules in Canada:

-

5% on the first $500,000

-

10% on the portion between $500,000 and $999,999

-

20% for homes $1 million or higher

Many Calgary first-time buyers purchase homes using 5% down payment programs.

How Debt Affects Mortgage Approval

Existing debt can significantly reduce borrowing power.

Example:

| Monthly Debt | Approximate Mortgage Reduction |

|---|---|

| $300 car payment | ~$60,000 less borrowing power |

| $600 debt payments | ~$120,000 less borrowing power |

Paying down consumer debt before applying for a mortgage can dramatically increase your approval amount.

Calgary First-Time Buyers Often Qualify Sooner Than Expected

Many buyers assume they need a very high income before purchasing their first home.

However, programs such as:

-

insured mortgages

-

5% down payments

-

extended amortizations

allow buyers to enter the Calgary housing market earlier than they expect.

Calgary Mortgage FAQ

What salary do you need to buy a house in Calgary?

Most buyers need a household income between $90,000 and $120,000 to comfortably afford homes priced between $450,000 and $600,000, depending on their down payment and debt levels.

Can I buy a house in Calgary with $80k income?

Yes. Buyers earning around $80,000 per year may qualify for homes around $375,000 to $425,000, assuming minimal debt and a typical down payment.

How much mortgage can I qualify for in Calgary?

Most lenders allow housing costs up to 39% of gross income and total debts up to 44% of income, subject to the mortgage stress test.

Get a Personalized Mortgage Estimate

Online examples are helpful, but every mortgage approval depends on:

-

income structure

-

employment history

-

credit score

-

debt levels

-

down payment

If you want a personalized estimate of how much house you could afford in Calgary, feel free to reach out.

I’m happy to review your situation and give you a realistic price range before you start house hunting.

Author

Mark Herman, MBA

Mortgage Broker – 22 Years of Experience

Mark helps Calgary home buyers navigate mortgage approvals, complex income situations, and lender options. His goal is to help clients secure the right mortgage strategy before they start shopping for a home.

Approved: Mortgage with U.S. Income, Remote Work & Gifted Down Payment (CMHC Deal)

Cross-Border Mortgage Approved: U.S. Income + Gift Funds + CMHC

This Mortgage Deal Looked Impossible (But CMHC Approved It Anyway)

We recently completed a mortgage deal that even I assumed is impossible.

We got it done — and now that we’ve successfully navigated the process, we’re ready to help more buyers in similar situations.

This file was a great example of how the right strategy, documentation, and lender experience can turn a complicated deal into a clean approval.

Mortgage Mark Herman, Best Alberta, Canada mortgage broker for Americans buying in Canada.

The Buyers

This purchase involved two applicants:

-

Buyer #1: Canadian citizen, stay-at-home mom, currently with no income

-

Buyer #2: Permanent resident (PR), employed as a lawyer for a U.S. company, paid in U.S. dollars

Files like this can get tricky quickly, especially when one borrower has no income and the other is employed outside of Canada.

The Property

This was a primary residence purchase.

The buyers also had no other properties, which helped strengthen the application and simplify insurer review.

The Biggest Challenge: U.S. Income + Remote Work

The income-earning borrower worked for an American employer and was able to work 100% remotely.

The key detail? Their employment letter confirmed remote work was permanent, not temporary.

The documentation included:

-

Employment letter confirming permanent remote work status

-

U.S. income documents (W-2 and 1040)

-

A clear written narrative summarizing income and filing history

When borrowers are paid in U.S. dollars, lenders and insurers need to clearly understand consistency, deductions, and income stability. Presentation matters.

Down Payment Structure

The buyers had a 15% down payment, structured as follows:

-

5% from their own funds

-

10% gifted from a family member in the United States

Gifted down payments are common, but cross-border gifted funds require extra documentation and clean sourcing. We made sure everything was properly verified and acceptable for insurer guidelines.

CMHC Approval (Including an American Credit Report)

This mortgage was approved through CMHC, and one of the most interesting parts of the deal was that CMHC accepted an American Equifax credit bureau report.

That’s something many buyers don’t realize is even possible — but in the right scenario, it can absolutely work.

Why This Deal Was Unique

This was not a typical mortgage approval.

It required:

-

Cross-border income verification

-

Review of U.S. tax documents

-

Confirmation of permanent remote employment

-

Gifted down payment verification from the U.S.

-

Credit review using an American credit bureau report

-

Proper structuring and presentation for insurer underwriting

But in the end, the deal was approved — and the buyers are now homeowners.

The Takeaway

If you’re a Canadian citizen or PR earning U.S. income, working remotely, or receiving gifted funds from outside Canada, you may still qualify for a mortgage — even if your situation feels complicated.

A bank “no” doesn’t always mean the deal is dead. It often just means it needs the right approach.

Need Help With a Complex Mortgage File?

If you’re buying in Canada but your income, credit, or down payment involves the U.S., I can help you structure it properly from the start.

Mark(at)MaMaRv.ca

Or call/text directly to discuss your options.

Advice on Mortgage Renewals Before April 2026 from an MBA

Questions on what product to pick for your upcoming mortgage renewal.

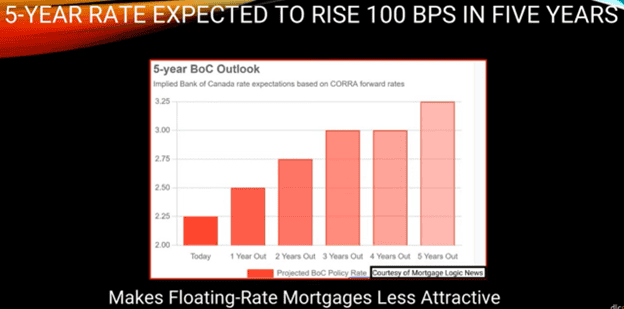

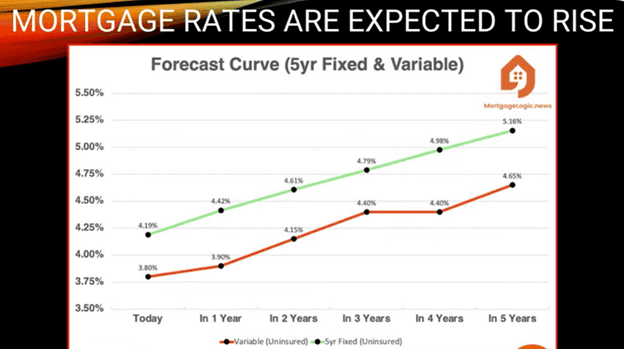

Here are the reasons that we like the 5 year fixed for Canadian mortgage renewals over the next few months.

(renewals from now, February 2nd until April 1st.)

This data is recent and should be good for the next few months.

Below are the graphs that show that rates are trending up and are on the increase.

Q: Why are rates trending up?

A: Because Trump policy is generally inflationary, and add in the “cost of uncertainty” due to changing tariffs and other world political issues we have an increasing rate environment.

Big Picture Perspective

I also look at from this perspective, rates were close to 4% BEFORE Covid in 2020, and we are now back to about the same; 3.99% for a 3-year fixed and 4.25% to 4.54% for a 5 year fixed rate term.

- Comparing these rates, there is not much room for rates to go down; maybe .5%, half a percent.

- But there is lots of room for them to go up.

What if things get out of hand and rates are at 6% or 7%?

When I started out in 2004, my first customer’s rate was 8.99% and they were happy it did not start with a 9. (You always remember your first deal.)

Summary

The rates for the 3 year fixed and the 5 year fixed are similar so take the 5 year and know you are getting a good rate at the bottom of the rate cycle.

If you take the 3 year and rates DO go up, and you then renew 2 years sooner into what could be 6% or 7% rate environment (when you could have had 2 more years at 4.zz%.) You will be pretty upset as your new monthly payment would now be higher even though your balance is lower.

If you take the 3 year fixed and the rates stay low then you gain a slightly lower payment ($25/ month) over the first 3 years.

Most of our customers agree the safer bet is less expensive when you factor in how sound you will sleep at night.

Mortgage Mark Herman, best Calgary broker for mortgage renewals and advice.

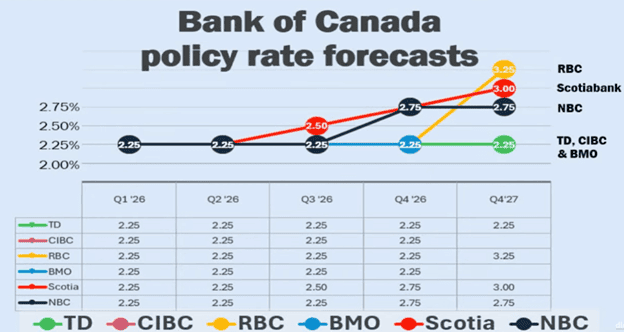

Stress Test Continues; Was Almost Abolished

Yes, the Stress Test was almost done away with but it continues.

It seems to be a good thing that all the mortgages since 2018 have been “stress tested” at 5.25%. Now that we are in the middle of 3.6 million mortgages renewing over an 18 month period we find that most everyone is able to make their new mortgage payments after renewal.

Mortgage Mark Herman, MBA in Finance and 22 years experience as a mortgage broker in Western Canada

Nerd alert here!!

OSFI has also determined that loan-to-income (LTI) limits on each institution’s mortgage portfolio will remain in place, alongside the existing stress test.

LTI limits have been in place since each institution’s 2025 fiscal year start and are reported on a quarterly basis.

This is a limit on the volume of newly originated uninsured mortgage loans, at that financial institution, that exceed a 4.5x loan-to-income multiple. This is not a limit on each individual loan.

This measure was introduced in an effort to lessen the build-up of highly leveraged residential mortgage borrowers.

Background

Canada’s federal mortgage stress test began on January 1, 2018, when the Office of the Superintendent of Financial Institutions (OSFI) introduced it for uninsured mortgages.

Key Details of the Stress Test

- Introduced: January 1, 2018

- Regulator: OSFI (Office of the Superintendent of Financial Institutions)

- Applies to: Uninsured mortgages (20%+ down payment) at federally regulated lenders

- Purpose: Ensure borrowers can afford payments at a higher qualifying rate than their contract rate

Buying a Home with a Basement Suite – Some Details

Buying a home with a basement suite can be a powerful way to increase affordability, improve cash flow, and build long-term wealth — but not all suites (or lenders) are treated the same. If you’re considering a home with a suite, here are four important things to think about before you buy.

1) The type of suite matters.

If a suite is legal (fully permitted and meets municipal bylaws), all lenders will accept the rental income for qualification. If it’s not legal, make sure it’s at least fully self-contained, meaning it has its own entrance, its own kitchen, and its own bathroom. Many lenders will still consider rental income from these types of suites, but not all.

2) Your lender choice can change how much you qualify for.

Different lenders treat rental income very differently. Some will only allow 50% of the rental income to be used, while others allow up to 100%. Some lenders make you debt-service property taxes and heat, while others do not. These differences can have a huge impact on your approval amount, which is why working with a broker who understands rental income policy is so important.

3) Whether the suite is already rented or not DOES matter.

If the suite is currently rented, you should obtain a copy of the lease, make sure the purchase contract clearly states that the tenant is staying, and ensure the monthly rent amount is documented. If the suite is not already rented when you purchase the home, lenders will typically require an appraisal to confirm market rent. It’s very important to be conservative about what you expect the suite to rent for — especially if that rental income is crucial to comfortably affording the home.

What about adding a basement suite OR Mother-in-Law suite to the home I am buying?

Great idea, adding a suite to the home that you are buying AND at the same time, using the expected rental income from that same suite to qualify for the mortgage IS possible. There are a few lenders that allow this to happen and we do deals like this all the time. (No shortcuts though, as the final step is a final inspection and also providing the lender a copy of the occupancy permit from the City before the funds can be released.

Obviously there are some details involved but adding a suite and using the expected rental income to qualify for the mortgage is a huge helper for buyers looking to push a bit higher and get a “mortgage helper.”

Mortgage Mark Herman, 1st time home buying mortgage specialist