Variable Rate Beats BOTH 3-year & 5-year Fixed Terms

The Variable is the best way to go right now and this blue link has all the details in PDF: VARIABLE RATE beats both 3-year fixed & 5-year fixed terms

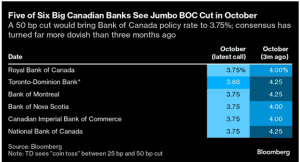

Data point 1: Variable rates should be coming down 2% in the next 13.5 months, with a “jumbo reduction” of 0.5% (1/2%) expected on Wednesday, Oct 23rd – by 5 of the 6 Big Banks.

Data point 2: Historically, fixed rates only go down about 40% of the reductions to Prime, so fixed rates will not be going down anywhere near as much or as fast as the Variable.

Data point 3: Just a 1% rate reduction is expected to “reactivate” at least half of buyers who previously stopped shopping due to “buyer fatigue.”

Data point 4: As interest rates come down, prices INCREASE because most buyer’s need to go to their max mortgage when buying.

Graphic details of expected rate reductions and the dates of expected changes, in PDF: VARIABLE RATE beats both 3-year fixed & 5-year fixed terms

Our favorite customer quote so far in October:

I am not locking in 3-year money nor 5-year money today, when the Bank of Canada has made it clear rates are coming down 2% in the next 15 months.

Mortgage Mark Herman, Top Calgary Alberta Mortgage Broker near me.

New Canadian Mortgage Rules; Sept 2024

Great news from Ottawa today on the new rules for Canadian mortgages:

- An Increase to the Insured Mortgage Price Cap: The government will raise the price cap from $1 million to $1.5 million, reflecting the realities of today’s housing market. This change, effective December 15, 2024, will help more Canadians qualify for insured mortgages and make homeownership more attainable, especially for younger Canadians.

- Expanded Eligibility for 30-Year Amortizations: First-time homebuyers and all buyers of new builds will now be eligible for 30-year insured mortgage amortizations. This is a crucial step in reducing monthly mortgage payments and helping more Canadians, particularly Millennials and Gen Z, achieve the dream of owning a home.

- Increased Mortgage Competition: The strengthened Canadian Mortgage Charter now enables insured mortgage holders to switch lenders at renewal without being subject to another stress test. This will foster greater competition and ensure Canadians have access to the best mortgage deals.

All 3 of these changes will help New Buyers / 1st Time Buyers afford to get into a home of their own.

Most of our First Time Buyers need gifts or co-signing from parents to be able to buy. The 30 year amortization and increase of CMHC insurance will totally help.

Mortgage Mark Herman, Best top Calgary Alberta mortgage broker specializing in 1st time buyers for 20 years.

Prime now 6.95% from 7.20%: BoC reduces its benchmark interest rate to 4.75%

Today, the Bank of Canada reduced its overnight policy interest rate by 0.25% to 4.75%. This welcome and widely expected decision comes on the heels of evidence pointing to a deceleration of the rate of inflation.

SUMMARY:

The “overnight rate” being quoted is the rate that Banks borrow from each other at, not consumer Prime, which is confusing.

Canadian Consumer Prime has just been reduced from 7.20% to 6.95% – this only affects Variable Rate mortgages.

Fixed rates remain unchanged because they track the Canadian Mortgage Bond Rates which are different, and similar.

There has also been about 40 “silent” fixed rate reductions of o.o5% each in 2024 that the press did not cover.

Mortgage Mark Herman, Top best Calgary Alberta mortgage broker specializing in 1st time buyers

Below we examine the Bank’s rationale for this move by summarizing its observations below, including its all-important outlook comments that are sure to shape market expectations for the remainder of the year.

Canadian inflation

- Inflation measured by the Consumer Price Index (CPI) eased further in April to 2.7%

- The Bank’s preferred measures of core inflation also slowed and three-month indicators suggest continued downward momentum

- Indicators of the breadth of price increases across components of the CPI have moved down further and are near their historical average, however, shelter price inflation remains high

Canadian economic performance and housing

- Economic growth resumed in the first quarter of 2024 after stalling in the second half of last year

- At 1.7%, first-quarter GDP growth was slower than the Bank previously forecast with weaker inventory investment dampening activity

- Consumption growth was solid at about 3%, and business investment and housing activity also increased

- Labour market data show Canadian businesses continue to hire, although employment has been growing at a slower pace than the working-age population

- Wage pressures remain but look to be moderating gradually

- Overall, recent data suggest the economy is still operating in excess supply

Global economic performance and bond yields

- The global economy grew by about 3% in the first quarter of 2024, broadly in line with the Bank’s April Monetary Policy Report projection

- The U.S. economy expanded more slowly than was expected, as weakness in exports and inventories weighed on activity

- In the euro area, activity picked up in the first quarter of 2024 while China’s economy was also stronger in the first quarter, buoyed by exports and industrial production, although domestic demand remained weak

- Inflation in most advanced economies continues to ease, although progress towards price stability is “bumpy” and is proceeding at different speeds across regions

- Oil prices have averaged close to the Bank’s assumptions, and financial conditions are little changed since April

Summary comments and outlook

The Bank cited continued evidence that underlying inflation is easing for its decision to change its policy interest rate. More specifically, it said that “monetary policy no longer needs to be as restrictive.”

Also welcome was the Bank’s statement that “recent data” have “increased our confidence that inflation will continue to move towards” its 2% target.

However, it also added this to its outlook: “Nonetheless, risks to the inflation outlook remain. Governing Council is closely watching the evolution of core inflation and remains particularly focused on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour.”

And has it has been doing for some time, it said the Bank “remains resolute in its commitment to restoring price stability for Canadians.”

Next up

The Bank returns on July 24th with its next monetary policy announcement – I think they will do another 0.25% reduction at the next meeting and they will continue to reduce at every meeting for the next 3 meetings this year.

GIFTed down Payment now possible for New-to-Canada home buyers!!

For New to Canada buyers – Expanded “GIFT-ing” is now possible for close family members!

That’s right! As of now, May 23, 2024, buyers who are New to Canada – in Canada for less than 2 years – ARE now allowed to use /receive GIFTS for down payment from “close family members.”

This is a big deal because it now includes; aunts, uncles, nephews, and cousins; all were not allowed to provide a “GIFT for down payment” before.

The standard used to be only: mother, father, brother, sister, grandparent and legal guardian; and that was it.

From our data that we have on on our own customers, this will help about 20% of our New to Canada files to buy a home, where they would have been shut out before.

Mortgage Mark Herman, top best fantastic Calgary Alberta mortgage broker, specializing in First Time Buyers.

We view that the Expanded Gift-er Options ARE needed due to the average new home price being 500k+, it is super tough for newcomers to save enough to buy a home. GIFTS are relied on all the time by 1st time home buyers.

Bank of Canada Leaves Prime the Same, April 2024

As Expected, No change in Bank of Canada benchmark interest rate for April 2024.

As noted in August 2023, the 1st Prime Rate reduction is expected in July and then Prime should come down at o.25% every 90 days so … 1 quarter percent reduction, every calandar quarter, for the next 2 years.

Mortgage Mark Herman, best top Calgary Alberta mortgage broker.

Today, the Bank of Canada announced it is keeping its benchmark interest rate at 5.0%, unchanged from July of 2023. However, much has changed in the economy and in the world since then. For evidence, we parsed today’s announcement and present a summary of the Bank’s key observations below.

Canadian Inflation

- CPI inflation slowed to 2.8% in February, with easing in price pressures becoming more broad-based across goods and services. However, shelter price inflation is still very elevated, driven by growth in rent and mortgage interest costs

- Core measures of inflation, which had been running around 3.5%, slowed to just over 3% in February, and 3-month annualized rates are suggesting downward momentum

- The Bank expects CPI inflation to be close to 3% during the first half of 2024, move below 2.5% in the second half, and reach the 2% inflation target in 2025

Canadian Economic Performance and Housing

- Economic growth stalled in the second half of last year and the economy moved into excess supply

- A broad range of indicators suggest that labour market conditions continue to ease. Employment has been growing more slowly than the working-age population and the unemployment rate has risen gradually, reaching 6.1% in March. There are some recent signs that wage pressures are moderating

- Economic growth is forecast to pick up in 2024. This largely reflects both strong population growth and a recovery in spending by households

- Residential investment is strengthening, responding to continued robust demand for housing

- The contribution to growth from spending by governments has also increased. Business investment is projected to recover gradually after considerable weakness in the second half of last year. The Bank expects exports to continue to grow solidly through 2024

- Overall, the Bank forecasts GDP growth of 1.5% in 2024, 2.2% in 2025, and 1.9% in 2026. The strengthening economy will gradually absorb excess supply through 2025 and into 2026

Global Economic Performance and Bond Yields

- The Bank expects the global economy to continue growing at a rate of about 3%, with inflation in most advanced economies easing gradually

- The US economy has “again proven stronger than anticipated, buoyed by resilient consumption and robust business and government spending.” US GDP growth is expected to slow in the second half of this year, but remain stronger than forecast in January

- The euro area is projected to gradually recover from current weak growth. Global oil prices have moved up, averaging about $5 higher than the Bank assumed in its January Monetary Policy Report

- Since January, bond yields have increased but, with narrower corporate credit spreads and sharply higher equity markets, overall financial conditions have eased

- The Bank has revised up its forecast for global GDP growth to 2.75% in 2024 and about 3% in 2025 and 2026

- Inflation continues to slow across most advanced economies, although progress will likely be bumpy. Inflation rates are projected to reach central bank targets in 2025

Outlook

Based on the outlook, Governing Council said it decided to hold the Bank’s policy rate at 5% and to continue to “normalize” the Bank’s balance sheet. It also noted that while inflation is still too high and risks remain, CPI and core inflation have eased further in recent months.

The Council said it will be looking for evidence that this downward momentum is sustained. Governing Council is particularly watching the “evolution of core inflation,” and continues to focus on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour.

As it has said consistently over the past year, the Bank will remain “resolute in its commitment to restoring price stability for Canadians.”

Next Touchpoint

On June 5th, 2024, the Bank returns with another monetary policy announcement and economists are already lining up with predictions of a rate cut either then or in July.

Net Migration to Alberta – #’s here.

the CORE reason home prices in Calgary will be going up for the next 4 years, and are 100% supported and will not be coming down is summed up in this article right here.

https://www.cbc.ca/news/canada/calgary/alberta-population-records-2023-to-2024-data-1.7157110

Summary of the Main Reasons Home Prices are Supported:

- BC and Ontario home prices are DOUBLE Calgary home prices

- 4 million New Canadians on the way here in the next 5 years.

- We hatched the largest 20 – 29 year old population Canada has EVER had, and they are moving out of their parent’s basements and buying their own homes.

- Alberta does NOT have PST

- Alberta does not have a 1% “welcome to the neighborhood tax” when buying property.

After researching the above data points we can confidently say all 5 of these stacked factors will cause home prices to increase is all price ranges for the next few years.

Mortgage Mark Herman, licensed as a top Alberta Mortgage Broker for 21 years and 1 year in BC

Why to Buy Your Home Now; Vancouver Island, Winter, 2024

Summary

We expect to see multiple & competing offers, with NO Financing Conditions for all home types, priced from $400k to $1.1M, starting now, and growing to “full-scale crazy- town” by May.

Use this time before May 2024 to take advantage of slight & short term softening of the market before:

- News of lower mortgage interest rates ignites a powder keg of sidelined, eager, competitive buyers.

- Prices continue to climb due to continued competition from 4 million New Canadian immigrants for the few homes on the market; for the next 4 years!

- Housing will remain in super-tight supply with inventory pre-sold before it gets to market.

Shameless Advertisement … then the data

Your #1 concern should be: how does my offer win among 5, 10 or 20 others?

Will you have the confidence in your broker or bank to write a No Condition or Lo Condition Offer?

We support NO CONDITION & LOW CONDITION OFFERS!

-

- with 100% pre-underwritten approvals and

- 9am to 11 pm live phone support – with me & your realtor – when writing your offer to ensure it works.

To take your 1st step to a FULLY Pre-Undewritten, Pre-Approval; that could go NO Conditions, if needed – click here.

DETAILS

1. Mortgage Rates

Have Decreased Already – but on the down low.

Without media attention, About 20 tiny reductions have already happened for FIXED RATES.

- Fixed rates have been slowly and quietly decreasing from Post-COVID 20 year highs; they were ~7% and are now ~5%

- Most people are only aware of the 10x Prime rate increases in a row post-COVID in 2023/23

- Prime has held steady at 7.2% since then,

- 1st Prime reduction expected in July and it has already been “100% priced-in” by the stock market.

- Inflation and the Consumer Price Index came in at 2.9% and is now back inside the target range of 1.0% to 3.0%.

Why the Rush?

1A. Joe Public is now correctly thinking;

-

the slight extra interest cost of buying now with marginally higher mortgage rates and some actual inventory selection to choose from; far, far, far out weighs …

- the small increase in buying power from lower rates that is sure to come with

- massive price increases when buying in the frenzy starts after the BoC rate cuts hit the news.

1B. 50% of “Exhausted Buyers” plan to re-enter the market when rates drop

A recent survey, half (51%) of those who put their home purchase plans on hold, now say they will re-enter the market when they hear that rates have dropped.

- A rate decline of just o.25% would be enough to bring 10% of those Exhausted Buyers back,

- A rate decline of 1.00% would bring back 23% of those sidelined.

- the Prime rate (for variable rates) is expected to go down 2%, and fixed rates could easily sneak down another 1.5% yet too.)

1C. AUTO_RATE_FLOAT_DOWN helps

In a decreasing rate environment, if the rates goes down AFTER you sign, you still AUTOMATICALLY get the lower rate right up until 5 business days before you move in.

See the GRITTY details of WHY THE VARIABLE RATE IS THE WAY TO GO HERE

- The Variable lets you take advantage the rates going down over the next 28 months, right now. It goes you an option to not take a fixed rate at near 10-year highs.

2. Home Pricing

Home prices on Vancouver Island are FULLY SUPPORTED, and will NOT be dropping at all, due to continuous demand from record setting immigration for the next 5 years.

- Remember in 2022, during COVID when “buyers were acting irrationally” and then home prices went up $500k over 1 year?

- That is about to happen again!

Consider this is the reason why Vancouver Island is in such demand …

- Every day, somewhere in Canada, say about 100 people retire and “sell all their things” and plan to move West, to the Island, and retire in Canada’s only temperate rain-forest. The #1 location choice for retirees.

- Right now the high interest rates are slowing the asset sales for these retirees to “move their high value assets” and move West including: primary and rental homes, cabins, businesses, vehicles and boats.

- When interest rates come down, buyers will better afford loans on these assets, and the above items will sell. The “tidal wave” of backlog retirees will all “move West to the Island” for the weather and retirement in a rush.

- With plentiful CASH reserves to haphazardly throw down on their last home purchase, completing their dream; and frustrating yours.

Prices are expected to further INCREASE for the next 5 years due to these data points below:

3. Current homes prices well below national average:

For 2023: Calgary; up 4%, Halifax; up 3%, Victoria; up 1%

- All other cities in Canada are down 18% to 21%‘; which really means Victoria is really up about 22-ish%.

- [data point here]

4. Peek New-to-Canada Immigration

Overall Canada’s population growth is 3.1% – 6x higher than the USA at o.5%.

- 1.2 million new Canadians arrived in 2022 – highest growth of all the G20.

- 4 million new Canadians are on the way before 2027; where will they live?

- That’s 2x Canada’s already hefty overall population increase, which also broke records.

- “We have never seen the young adult population growing anywhere nearly this fast before,” an analyst wrote. “Putting additional pressure on rents now, and in the medium term, it will put pressure on home prices.”

- See the red-blue graph below

5. Renting in the Wild West

37% of Canadian households are renters.

- New renters are on the scene from an unprecedented rise in working age population – up 874,000 in 2023

- Rent inflation was 8.2% in October 2023 – highest in over 40 years.

- The difference between rent inflation and “standard inflation” is the highest in 60+ years.

Costs to build a home are up 51% since 2020.

- High costs for all inputs, scarcity of skilled construction workers, higher mortgage interest rates for builder’s financing, supply-chain bottlenecks from COVID. (See the graphics below.)

- Forest fires from 2020 to 2023 have reduced the supply of lumber.

- 100,000 new construction workers are needed in Canada.

- Most will be “temporary foreign workers” also hoping to become citizens and buy the same home supply they are producing.

- Construction wages were up 11.5% in 2023.

{Lots of fantastic graphs go here.

For a copy of the actual report in PDF, please request from me in email.}

What about COMPETING / Multiple Offers?

- We do Lo/No CONDITION OFFERS with Pre-underwritten, Pre-approvals that actually work.

- And I answer my phone from 9-9 x 360 so you can win your competing deals at the last second.

- Banks don’t offer this service. We have been doing this since “the Rush of 2007” when home prices were going up $1000/ day. This will be similar.

Why Buy Your Home Today: Data Points, Alberta, Winter, 2024

|

Underlying Economic data on BoC holding Prime rate the same, December 5, 2023

Bank of Canada holds its policy interest rate steady, updates its outlook

Against the backdrop of a decelerating economy and growing calls for less restrictive monetary policy, the Bank of Canada made its final scheduled interest rate decision of the year today.

That decision – to keep its overnight policy interest rate at 5.00% – was broadly expected. What was not entirely expected (or welcome) was the Bank’s statement that it is “still concerned” about risks to the outlook for inflation and “remains prepared to raise” its policy rate “further” if needed.

The Bank’s observations are captured in the summary below.

Since August, we have been saying the VARIABLE RATE mortgage is the way to go, and this proves we were right on the money.

Mortgage Mark Herman, top Calgary Alberta and Victoria BC mortgage broker

Inflation facts and housing market commentary

- A slowdown in the Canadian economy is reducing inflationary pressures in a “broadening range” of goods and services prices

- Combined with a drop in gasoline prices, this contributed to easing of CPI inflation to 3.1% in October

- However, “shelter price inflation” picked up, reflecting faster growth in rent and other housing costs along with the continued contribution from elevated mortgage interest costs

- In recent months, the Bank’s preferred measures of core inflation have been around 3.5-4%, with the October data coming in towards the lower end of this range

- Wages are still rising by 4-5%

Canadian economic performance

- Economic growth “stalled through the middle quarters of 2023 with real GDP contracting at a rate of 1.1% in the third quarter, following growth of 1.4% in the second quarter

- Higher interest rates are clearly restraining spending: consumption growth in the last two quarters was close to zero, and business investment has been volatile but essentially flat over the past year

- Exports and inventory adjustment “subtracted” from GDP growth in the third quarter, while government spending and new home construction provided a boost

- The labour market continues to ease: job creation has been slower than labour force growth, job vacancies have declined further, and the unemployment rate has risen modestly

- Overall, these data and indicators for the fourth quarter suggest the economy is “no longer in excess demand”

Global economic performance and outlook

- The global economy continues to slow and inflation has eased further

- In the United States, growth has been stronger than expected, led by robust consumer spending, but is “likely to weaken in the months ahead” as past policy rate increases work their way through the economy

- Growth in the euro area has weakened and, combined with lower energy prices, has reduced inflationary pressures

- Oil prices are about $10-per-barrel lower than was assumed in the Bank’s October Monetary Policy Report

- Financial conditions have also eased, with long-term interest rates “unwinding” some of the sharp increases seen earlier in the autumn. The US dollar has weakened against most currencies, including Canada’s

Summary and Outlook

Despite (or in the Bank’s view because of) further signs that monetary policy is moderating spending and relieving price pressures, it decided to hold its policy rate at 5% and to continue to normalize its balance sheet.

The Bank also noted that it remains “concerned” about risks to the outlook for inflation and remains prepared to raise its policy rate further if needed. The Bank’s Governing Council also indicated it wants to see further and sustained easing in core inflation, and continues to focus on the balance between demand and supply in the economy, inflation expectations, wage growth, and “corporate pricing behaviour.”

Once again, the Bank repeated its mantra that it “remains resolute in its commitment to restoring price stability for Canadians.” As a result, we will have to wait until next year for any sign of rate relief.

What’s next?

The Bank’s next interest rate announcement lands on January 24, 2024.

In the meantime, please feel free to call me and discuss financing options that will empower you in this economic cycle, and the ones ahead.

BoC Holds Canadian Prime at 6.7% on April 12th – Good News!

Today, April 12, 2023, the Bank of Canada held its policy interest rate at 4.50%, a welcome outcome for borrowers after almost a year of constant increases, and a timely confidence-builder for the real estate industry as it enters the spring market.

The Bank also issued its latest Monetary Report with updated risk assessments and base-case projections for inflation.

We highlight the Bank’s latest observations below.

Inflation acts and outlook

- In Canada, the Consumer Price Index (CPI) inflation eased to 5.2% in February, and the Bank’s preferred measures of core inflation were just under 5%

- The Bank expects Canadian CPI inflation to “fall quickly” to around 3% in the middle of 2023 and then decline more gradually to the 2% target by the end of 2024

- Recent data is reinforcing Governing Council’s “confidence” that inflation will continue to decline in the next few months

- Similarly, in many countries, inflation is easing in the face of lower energy prices, normalizing global supply chains, and tighter monetary policy

- At the same time, labour markets remain “tight” and measures of core inflation in many advanced economies suggest persistent price pressures, especially for services

Canadian economic performance and outlook

- Domestic demand is still exceeding supply and the labour market remains tight

- Economic growth in the first quarter looks to be stronger than was projected in January, on a “bounce” in exports and solid consumption growth

- While the Bank’s Business Outlook Survey suggests acute labour shortages are starting to ease, wage growth remains elevated relative to productivity growth

- Strong population gains are adding to labour supply and supporting employment growth while also boosting aggregate consumption

- Softening foreign demand is expected to restrain exports and business investment

- Overall, GDP growth is projected to be weak through the remainder of this year before strengthening gradually next year, implying the Canadian economy will move into excess supply in the second half of this year

- The Bank now projects Canada’s economy will grow by 1.4% this year – an improvement over its last forecast of 1% growth – 1.3% in 2024 (a downgrade from its last forecast of 2% for 2024) and then pick up to 2.5% in 2025

Canadian housing market

- Housing market activity remains subdued

- As more households renew their mortgages at higher rates and restrictive monetary policy works its way through the economy more broadly, consumption is expected to moderate this year

Global economic performance and outlook

- The Bank’s April Monetary Policy Report projects global growth of 2.6% in 2023 – an improvement over its last forecast of 2% offered in January – and then fall to 2.1% in 2024 (lower than it last forecast of 2.5%), and rise to 2.8% in 2025

- Recent global economic growth has been stronger than anticipated with performance in the United States and Europe surprising on the upside

- However, growth in those regions is expected to weaken as tighter monetary policy continues to feed through those economies

- In particular, US growth is expected to “slow considerably” in the coming months, with particular weakness in sectors that are important for Canadian exports

- Activity in China’s economy has rebounded, particularly in services

- Overall, commodity prices are close to their January levels

Outlook

While holding the line on interest rates, the Bank also noted in today’s announcement that it is continuing its policy of quantitative tightening and remains “resolute in its commitment to restoring price stability for Canadians.” There was nothing new in that statement. However, it also posited that getting inflation the rest of the way back to 2% “could prove to be more difficult because inflation expectations are coming down slowly, service price inflation and wage growth remain elevated, and corporate pricing behaviour has yet to normalize.”

As it sets monetary policy going forward, the Bank’s Governing Council indicated that it will be “particularly focused” on these indicators, and the evolution of core inflation as it gauges the progress of returning CPI inflation back to its 2% target.

The Bank also said it continues to assess whether monetary policy is “sufficiently restrictive” to relieve price pressures and “remains prepared to raise the policy rate further if needed” to return inflation to its 2% target.

Next Announcement is …

We will have to wait until April 20th to get the next CPI reading to gauge progress in one of the Bank’s determining indicators and June 7th for the Bank’s next scheduled policy interest rate announcement.

Inflation is slowing and that is great news for Canadian home buyers

Mortgage Mark Herman, Top Calgary Alberta Mortgage Broker