Canadian economy running too hot, BoC increases Prime by .25%

Hot Economic growth leads the Bank of Canada to increase its benchmark interest rate

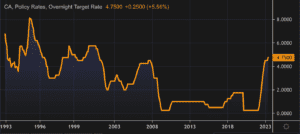

Today, the Bank of Canada increased its overnight interest rate to 4.75% (+0.25% from April) because of higher-than-expected growth in Canada’s economy in the first quarter and the view that monetary policy was not yet restrictive enough to bring inflation down to target.

BoC Holds Canadian Prime at 6.7% on April 12th – Good News!

Today, April 12, 2023, the Bank of Canada held its policy interest rate at 4.50%, a welcome outcome for borrowers after almost a year of constant increases, and a timely confidence-builder for the real estate industry as it enters the spring market.

Using Return-To-Work Income while on Maternity Leave to buy a home IS possible in Canada.

Using Return-To-Work Income while on Maternity Leave to buy a home IS possible in Canada.

Are you on maternity leave and trying to buy a home, but the bank will not use your income? This is a common reason home buyers find us on the internet or their realtors send them to us.

Bank of Canada increases its benchmark interest rate to 4.50%

Today, the Bank of Canada increased its overnight benchmark interest rate 25 basis point to 4.50% from 4.25% in December. This is the eighth time since March 2022 that the Bank has tightened money supply to address inflation.

New Mortgage Rules 2023: Expanding the “Stress Test” to Everything?

This is from the Desk of Dr. Cooper, our Economist, and this data is 1 of the reason we are at Dominion Lending – to get this data.

Below is the details of the government expanding the STRESS TEST, or other mechanisms, to make it harder to buy a home.

Work Visa’s / Non-Canadians Can’t Buy Homes: 2023 New Rules

Prohibition on the Purchase of Residential Property by Non-Canadians Act.

Summary of New Rules, 2023:

Anyone with a work visa will have to have lived here for 3 of the past 4 years and have filed taxes during those years. Here are the RULES!

Canadian Residential Mortgage Market: Inflation & Interest Rates: the Lead Characters for 2023

Summary:

- The Bank of Canada (BOC) increased interest rates 7 times in 2022. Exactly as expected 16 months ago.

- Inflation is at least 5.7%; and it needs to get down to 3%

- The BoC would rather over-tighten than under-tighten

- Normally it takes 18 to 24 months for interest rate increases to work their way into the economy and we are only about 10 months into this tightening cycle

These 4 painful data points mean Prime will increase from 6.45% to 6.70% on Jan 25th.

We now expect there to be at least 1 or 2 more o.25% increases to Prime before it is expected to hold for the rest of 2023, and then begin to decrease in 2024.

Details of Canadian Economic & Housing Market Performance, as at Dec 7, 2022

Non-technical summary of underlying economic data points causing Prime to increase to a 15-year high of 6.45% on Dev 7, 2022.

Canadian Prime Rate is now 5.95% – Mortgage Rate Analysis to End of 2022

Bank of Canada increased benchmark interest rate to 3.75%

Today, the Bank of Canada increased its overnight benchmark interest rate 50 basis point to 3.75% from 3.25% in September. This is the sixth time this year that the Bank has tightened money supply to quell inflation, so far with limited results.