RRSP vs TFSA vs FHSA for Down Payments in Canada (2026 Complete Guide)

RRSP vs TFSA vs FHSA for Down Payments in Canada (2026 Guide)

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience in First Time Buyers and Move Ups, and New Builds, in Calgary, Alberta & Victoria, BC.

If you’re buying a home in Canada, you have three powerful tools to build your down payment: RRSP (Home Buyers’ Plan), TFSA, and FHSA.

Used properly, these accounts can combine into $100,000+ per person tax-efficiently—but the rules, tax treatment, and transfer strategies are very different.

This guide breaks it down clearly—and shows how to stack them strategically.

Quick Comparison: RRSP vs TFSA vs FHSA

| Feature | RRSP (HBP) | TFSA | FHSA |

|---|---|---|---|

| Tax deduction on contribution | ✅ Yes | ❌ No | ✅ Yes |

| Tax-free withdrawal | ⚠️ Yes (if repaid) | ✅ Yes | ✅ Yes (if buying home) |

| Repayment required | ✅ Yes (15 years) | ❌ No | ❌ No |

| Max usable for down payment | $60,000 per person | No limit | $40,000 lifetime |

| First-time buyer required | ✅ Yes | ❌ No | ✅ Yes |

RRSP Home Buyers’ Plan (HBP): Powerful—but Comes With Strings

How it works

The RRSP Home Buyers’ Plan allows you to withdraw up to:

$60,000 per person

-

Couples can access $120,000 combined

-

Withdrawals are not taxed upfront

-

BUT treated like a loan to yourself

Key rules

-

Must repay over 15 years

-

Payments start after a grace period (typically year 2–5 depending on timing)

-

Missed payments = taxable income

What the chart got right…

✔ Tax deductible going in

✔ Tax-deferred on withdrawal

✔ Contribution room is lost permanently

What it missed (important nuance)

-

It’s not truly tax-free—it’s a tax deferral

-

Repayment reduces your future investing capacity

TFSA: The Most Flexible (But No Tax Break Up Front)

How it works

-

Contributions are not tax deductible

-

Growth and withdrawals are completely tax-free

-

No restrictions on use (including down payment)

Key advantages

✔ Withdraw anytime, for any reason

✔ Contribution room comes back the next year

✔ No repayment required

Limits

-

Annual limit: ~$7,000 (2025)

-

Lifetime room accumulates

Best use case

Emergency fund + down payment flexibility

Bridge gaps between FHSA/RRSP strategies

FHSA: The Ultimate First-Time Buyer Account

This is the most powerful tool right now.

How it works

-

Contributions are tax deductible (like RRSP)

-

Withdrawals are tax-free (like TFSA)

Limits

-

$8,000/year

-

$40,000 lifetime

Key benefits

✔ No repayment required

✔ Tax deduction on contributions

✔ Tax-free withdrawal for home purchase

Your chart nailed it:

✔ “Best of both worlds” (RRSP + TFSA)

How These Accounts Work Together (The Real Strategy)

Here’s where things get interesting—and where most buyers miss opportunity.

The “Stacked Down Payment” Strategy

You can combine:

-

FHSA: $40,000 (tax-free, no repayment)

-

RRSP (HBP): $60,000 (must repay)

Total = $100,000 per person

Couples = $200,000+ potential down payment

Transferring Between Accounts (Critical Planning Tool)

1. RRSP ➜ FHSA (Allowed + Strategic)

-

You can transfer RRSP funds into FHSA

-

No immediate tax consequence

-

Does NOT restore RRSP room

Strategy:

-

Move RRSP funds → FHSA

-

Convert “repayable” money → non-repayable tax-free money

2. FHSA ➜ RRSP (If You Don’t Buy a Home)

-

Fully allowed, tax-deferred rollover

-

No impact on RRSP contribution room

Safety net: no downside to opening FHSA early

3. FHSA ➜ TFSA (Not Efficient)

-

Treated as:

-

Taxable withdrawal

-

New TFSA contribution

-

Avoid this move unless necessary

4. TFSA ➜ RRSP or FHSA

-

Allowed, but:

-

No tax advantage on transfer itself

-

Only useful if creating deduction room

-

Which Account Should You Use First? (Simple Priority Order)

1. FHSA (Always first)

-

Tax deduction + tax-free withdrawal

-

No repayment

2. RRSP (If income is high)

-

Use if:

-

You’re in a high tax bracket

-

You want refund to boost savings

-

3. TFSA

-

Use for:

-

Flexibility

-

Overflow savings

-

Short-term timelines

-

Example: Smart Calgary Buyer Strategy

Let’s say a buyer earns $110,000:

-

Max FHSA → $8,000/year

-

Contribute to RRSP → get ~$3,000 tax refund

-

Put refund into TFSA

-

Repeat annually

Result:

-

Tax refunds accelerate savings

-

FHSA builds tax-free down payment

-

RRSP adds leverage via HBP

Common Mistakes to Avoid

❌ Using RRSP before FHSA

❌ Not planning RRSP repayment impact

❌ Ignoring contribution room strategy

❌ Missing transfer opportunities

Bottom Line

-

FHSA = best account (no debate)

-

RRSP = powerful but comes with repayment

-

TFSA = flexibility tool

The real advantage comes from using all three together strategically

FAQ

How much can I take from my RRSP for a down payment?

Up to $60,000 per person under the Home Buyers’ Plan.

Can I use RRSP and FHSA together?

Yes—you can use both for the same home purchase.

Do I have to repay FHSA withdrawals?

No—FHSA withdrawals are tax-free and do not require repayment if used for a qualifying home.

What’s the best account for first-time buyers?

The FHSA, because it combines RRSP tax deductions with TFSA tax-free withdrawals.

Rental Property Mortgage Renewal Alberta: Insured vs Insurable Rates Explained

Minimum Down Payment Canada: Rules, Examples & Options, 2026 Guide for Home Buyers

written by Mortgage Mark Herman; MBA with 22 years as a top mortgage broker

Minimum Down Payment in Canada: What Home Buyers Need to Know

One of the first questions people ask when they start thinking about buying a home is:

What is the minimum down payment in Canada?

The answer depends on the price of the home and how the mortgage is structured.

Understanding the rules early can help you figure out how much you need to save and what you qualify for.

Let’s walk through the basics.

Minimum Down Payment Rules in Calgary, and all of Canada

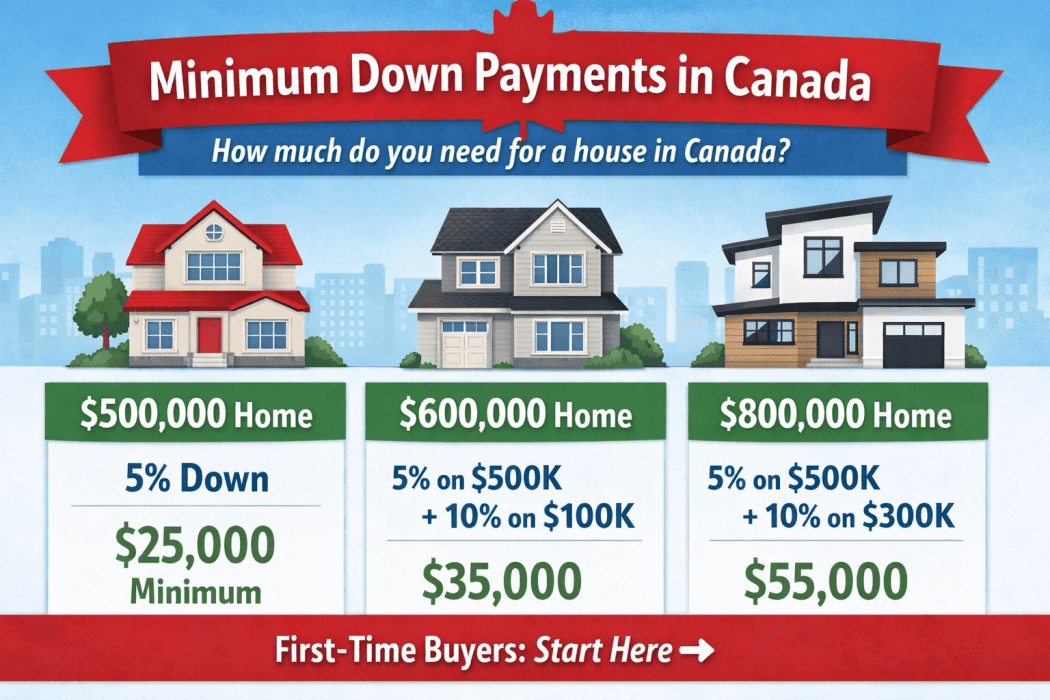

In Canada, the minimum down payment depends on the purchase price of the home.

Current rules are:

-

5% down on the first $500,000

-

10% down on the portion between $500,000 and $999,999

-

20% down for homes $1,000,000 or more

For example:

If you buy a $600,000 home, the minimum down payment would be:

-

5% on the first $500,000 = $25,000

-

10% on the remaining $100,000 = $10,000

Total minimum down payment = $35,000

High-Ratio vs Conventional Mortgages

Your down payment also determines the type of mortgage you qualify for.

High-Ratio Mortgage (5% – 19% Down)

If your down payment is less than 20%, your mortgage is considered a high-ratio mortgage.

This means the mortgage is more than 80% of the home’s value, so lenders require mortgage default insurance through providers like:

-

CMHC

-

Sagen

-

Canada Guaranty

The insurance premium is added to your mortgage amount and paid over time.

The upside? High-ratio mortgages often qualify for lower interest rates.

Conventional Mortgage (20% Down or More)

If you put 20% down or more, the mortgage is considered conventional.

This means:

-

No mortgage insurance required

-

Lower borrowing costs overall

-

More flexibility with lenders

Down Payment Requirements for Calgary Buyers

The minimum down payment rules in Canada apply nationwide, including here in Calgary.

However, many Calgary buyers are surprised to learn how little down payment they actually need. For example, a $500,000 home in Calgary could require as little as $25,000 down, which is often less than people expect.

If you’re buying in Calgary or Alberta and want to see what your numbers look like, it’s worth running the calculations early so you know your options.

Where Your Down Payment Can Come From

Lenders also need to verify where the down payment funds come from.

Here are the most common sources.

Savings or Investments

If your down payment is coming from:

-

savings

-

chequing accounts

-

investments

Lenders will require 90 days of account history.

This verifies that the funds belong to you and were not recently borrowed.

Your statements must clearly show:

-

your name

-

the account number

-

the transaction history

Gifted Down Payment in Canada

A gift from family is one of the most common ways buyers fund their down payment.

The gift can come from a family member not only in Canada but from almost anywhere in the world. It does need to be transferred into any Canadian financial institution to be used though.

However, lenders require confirmation that the gift does not need to be repaid.

This is done with a gift letter signed by both parties confirming it is a non-repayable gift.

The gift must come from a direct family member; mother, father, brother, sister, grandparent, legal guardian.

Using RRSPs for Your Down Payment

Canada has a program called the Home Buyers’ Plan (HBP).

It allows first-time buyers to withdraw up to $35,000 from their RRSP tax-free for a down payment.

Key details:

-

You have 15 years to repay it

-

Repayment starts two years after withdrawal

-

If you don’t repay it, the amount becomes taxable income

To verify RRSP funds, lenders will need:

-

the RRSP withdrawal form

-

your RRSP statement

Using RRSPs if You’re Not a First-Time Buyer

You can still withdraw RRSP funds even if you’re not a first-time buyer, but it will be taxed as income.

The financial institution usually withholds about 30% for taxes.

This isn’t always ideal, but it can still work depending on the situation.

Borrowing Against Another Property

If you already own property, you may be able to use the equity in that property for your down payment.

This can be done through:

-

a refinance

-

a home equity line of credit (HELOC)

We just need to verify the available equity through your current mortgage statements.

Down Payment From the Sale of Your Current Home

Many buyers use equity from selling their existing home as their down payment.

In that case lenders require:

-

the firm sale contract

-

your current mortgage statement

-

confirmation of the sale proceeds

If your purchase closes before your sale, bridge financing can cover the gap.

This is a very common situation and usually easy to arrange.

Borrowing Your Down Payment

Some borrowers with strong income can qualify to borrow their down payment from an unsecured line of credit.

This strategy isn’t right for everyone, but it can work if your income supports the additional debt.

With rents rising and many buyers trying to enter the market, some people choose this route instead of continuing to rent.

Down Payment Examples in Canada

Here are some quick examples of minimum down payments based on purchase price:

$500,000 home

Minimum down payment:

5% = $25,000

$600,000 home

5% on first $500,000 = $25,000

10% on remaining $100,000 = $10,000

Minimum down payment = $35,000

$800,000 home

5% on first $500,000 = $25,000

10% on remaining $300,000 = $30,000

Minimum down payment = $55,000

FAQ: Down Payment Questions in Canada

What is the minimum down payment for a house in Canada?

The minimum down payment is 5% for homes under $500,000, with additional requirements for higher price ranges.

Can my down payment be a gift?

Yes. Many buyers use gifted down payments from family, but lenders require a signed gift letter confirming it is not repayable. Each bank has it’s own template so don’t try to do one yourself, we will send it to you to fill in and e-sign.

Can I borrow my down payment?

In some cases, yes. Borrowers with strong income may qualify to borrow their down payment from a line of credit.

Can I use my RRSP for a down payment?

Yes. The Home Buyers’ Plan allows withdrawals of up to $60,000 tax-free, with 15 years to repay the funds.

Final Thoughts

There are many ways to structure a down payment, and the right strategy depends on your finances and long-term plans.

If you’re thinking about buying, it’s worth running the numbers early so you know exactly what you qualify for and how much you need to save.

If you want help figuring out your options, you can start here:

https://markherman.ca/contact

About the Author

Mark Herman is a mortgage broker with 22 years of experience helping Canadians finance their homes. He holds an MBA in Finance and specializes in structuring mortgages for first-time buyers, self-employed borrowers, and real estate investors. He can be reached at 403-681-4376.

Stress Test Continues; Was Almost Abolished

Yes, the Stress Test was almost done away with but it continues.

It seems to be a good thing that all the mortgages since 2018 have been “stress tested” at 5.25%. Now that we are in the middle of 3.6 million mortgages renewing over an 18 month period we find that most everyone is able to make their new mortgage payments after renewal.

Mortgage Mark Herman, MBA in Finance and 22 years experience as a mortgage broker in Western Canada

Nerd alert here!!

OSFI has also determined that loan-to-income (LTI) limits on each institution’s mortgage portfolio will remain in place, alongside the existing stress test.

LTI limits have been in place since each institution’s 2025 fiscal year start and are reported on a quarterly basis.

This is a limit on the volume of newly originated uninsured mortgage loans, at that financial institution, that exceed a 4.5x loan-to-income multiple. This is not a limit on each individual loan.

This measure was introduced in an effort to lessen the build-up of highly leveraged residential mortgage borrowers.

Background

Canada’s federal mortgage stress test began on January 1, 2018, when the Office of the Superintendent of Financial Institutions (OSFI) introduced it for uninsured mortgages.

Key Details of the Stress Test

- Introduced: January 1, 2018

- Regulator: OSFI (Office of the Superintendent of Financial Institutions)

- Applies to: Uninsured mortgages (20%+ down payment) at federally regulated lenders

- Purpose: Ensure borrowers can afford payments at a higher qualifying rate than their contract rate

Canadian Mortgage with American Income, 2025

Yes, that headline is true!!

August 15, 2025

We finally have an “A lender” in the Canadian mortgage broker space that will allow a buyer’s USA/ American income to be used.

Quick summary of the details.

- 30% down

- 80% of USA salary to be used, income based on USA tax docs

- Almost any standard residential property in Canada

- “A lender,” at A rates, no lender fee, no broker fee, underwritten the same as all Canadian mortgages

- No funny business here. This is a normal mortgage, that you would want. The same as what expect from any of the Big-6 banks in Canada.

For more data or to ask about a deal, contact Mortgage Mark Herman, on his cell phone. He usually answers his own phone; from 9 am to 9 pm MST daily.

Data points below summarize key criteria and parameters for an “A-lender” in the Canadian mortgage broker channel that accepts US income.

Borrower Eligibility

- Citizenship: any (US, Canadian, or other)

- Canadian residency: no minimum length of stay required

- Tax history: two consecutive years of US tax filings (no CRA filings needed – its true!)

Income Documentation

- W-2 forms (equivalent to Canadian T4 slips)

- IRS Form 1040 (equivalent to Canadian T1 returns)

- US Tax Return Transcripts or Notices of Assessment (NOA – Notice of Assessment)

- All documents must cover the most recent two-year period

Income & Loan Parameters

- Income recognized: up to 80% of gross US salary

- Income types accepted: salary only (sorry, the bank can’t use fee-for-service, or self-employed/ BFS income)

- Maximum loan-to-value ratio (LTV): 70%, means 30% down payment

- Credit underwriting conforms to Canadian mortgage regulations

Property Types

- Primary residence

- 2nd home / Secondary or vacation home and even…

- Rental or investment property

Notes

- No requirement for employer size, industry, or Canadian work history

- Simplified process: bypass CRA income filings entirely

- Ideal for US-based clients relocating, investing, or holding dual residences

We used to run into a few of these deals ever year, and now we see one every month so we found a lender that can do this business for our realtor partners.

The buyers only need 30% down, and the bank will use 80% of their USA salary as the income.

Mark Herman, top Calgary Alberta and Vancouver Island mortgage broker

GST Rebate for 1st Time Home Buyers

We have had lots of questions about this proram.

The legislation has been tabled, but is not done yet. As of today, and it is for contracts written May 27, 2025 or later.

Updates as they come in.

We have a 4-plex buyer who is purchasing a newly constructed 4-plex in Calgary at $1,250,000. His rebate is about 60k – now that is now pretty substantial!

Mortgage Mark Herman, 1st time buyer and move up mortgage specialist in Calgary Alberta.

BMO & CIBC: Not on list of Top-11 banks in Canada

Wow hey??

Who would guess that 2 of Big-6 banks that millions of Canadians “think they have a financial relationship with” did not even make the list of the Top-11 banks in Canada.

It is surprising the amount of customers that call us looking to “beat their bank’s mortgage rate” when they should be looking at if they should even be doing mortgage business at their main personal bank.

Mortgage Mark Herman, Calgary Alberta new home buyer and mortgage renewal specialist of 21 years.

We recommend that they also look at the T’s & C’s – Terms and Conditions – to their own bank’s mortgages to find:

- Payout penalties that are 500% to 800% – yes, 5x to 8x the amount of payout penalties at broker banks.

- Their renewal rates are usually always at rates higher than what Broker Banks offer – because Broker Banks know the broker that placed you there will jump at the chance to move them to a different bank, for a better/ market rate, and then we get paid again. Big-6 banks don’t have to worry about that because you are usually not aware of market rates.

- SELF-employed mortgage holders are often “worked over by the Big-6 banks” whereas, Broker Banks are more than happy doing tons for self-employed business owners.

Here’s the full list of Canada’s best banks for 2025, according to Forbes:

- Tangerine

- Simplii Financial

- RBC

- PC Financial

- Vancity

- EQ Bank

- TD

- Scotiabank

- National Bank

- Desjardins

- ATB Financial

footnote: link action here https://www.narcity.com/best-banks-in-canada-forbes-2025

Summary of Mortgage Rule Changes

Key Mortgage Rule Updates

30-year amortization for insured mortgages

Starting December 15, 2024, 30-year amortizations will be available for insured mortgages. This option is open to first-time homebuyers and those purchasing newly built homes, including condos.

Higher insured mortgage limits

Applications for insured mortgages will now be accepted for properties valued under $1.5 million, giving more buyers access to high-value homes with lower down payment requirements.

Stress test simplification

In line with OSFI’s guidance, current stress test requirements will continue for insurable, uninsurable, and uninsured applications. Eligible insured transfers and switches will remain qualified at the contract rate.

How these changes benefit you

✔️ Reduced monthly payments

Extending amortizations to 30 years will lower monthly payments, helping clients manage affordability amidst rising living costs and fluctuating interest rates.

It usually works out to reduce your payment by 9% or lets yo buy 9% more home (increases the mortgage amount but about 9%.)

✔️ Expanded opportunities for buyers

Higher insured mortgage limits make it possible for more Canadians to purchase homes in competitive urban markets like Toronto and Vancouver for up to $1,500,000 with 5% down on the 1st 500k and 10% down payment on the balance.

This set of mortgage rule changes should make it easier for buyers to get into a home now.

More importantly, it lets buyers purchase up to $1.5M with $125k down, where before they would have topped out at $1m with $75k down payment.

- Mortgage Mark Herman, top best Calgary mortgage broker,

- 403,681-4376

New Housing Rules for 1st First-Time Buyers and New Builds

If you’re a first-time home buyer or looking to purchase a new build, this affects you.

Here’s a quick summary of the changes coming in December 2024:

What’s New?

30-Year Amortizations Now Available for First-Time Buyers and New Build Purchases

- First-time home buyers can now access 30-year amortizations for insured mortgages.

- This increases the amount you qualify for by about 9% or lowers your monthly payment about the same.

- 30-Year Amortization for New Builds – Technically, this took effect on August 1, 2024, and is available to everyone, not just First-Time Homebuyers.

Price Cap Increase for Insured Mortgages

- The price cap (purchase price) for insured mortgages has been raised from $999,999 to $1,499,999 million.

- EG: if you were to purchase a home today priced at $1.1 million, your minimum down payment to qualify for a mortgage would be 20% or $220,000. After December 15th, the minimum down payment required decreases to $85,000.

- If that $1.1 million dollar home also has a self contained suite, you can use the rent or “potential” rent that suite will generate to help qualify for a bit more of a mortgage too.

The Fine Print

Down payment – Great news, minimum requirements stay the same:

- 5% on the portion up to $500,000

- 10% on the portion between $500,000 and $1.5 million

* Previously, the down payment on a $1.5 million home for a First-Time Home buyer was $300,000.

FTHB’s can now get into that same home with $125,000.

This will undoubtedly take some pressure off the Bank of Mom and Dad.

Effective Date

These changes will apply to mortgage insurance applications submitted on or after December 15, 2024. The key word here is ‘submitted.’ Your offer will need to be timed just right if you wish to take advantage of the new 30-year amortization.

Potential Impacts on the Housing Market:

We are in an interesting position right now. On one hand, lenders are competing for new business in what could be described as a ‘rate war.’

Additionally, with First-Time Home Buyers (FTHB) set to qualify for 30-year amortizations after December 15th, we can expect an uptick in demand.

Historically, higher demand leads to higher prices and rate decreases cause an equal and opposite increase in home prices.

Buy or Sell – Now or Later?

While there’s no crystal ball, consider these possibilities:

- Buy Now: Prices are expected to rise once the new rules take effect, so purchasing before December could mean less competition and potentially lower prices.

- Sell Later: If your home is priced between $1 million and $1.5 million, waiting until after December 15th could attract more qualified buyers and possibly higher offers.

More details will emerge as lenders and insurers prepare to offer the new 30-year amortization, such as how lenders will view the minimum down payment.

If you want to discuss how these changes might impact your plans to buy or sell, feel free to reach out!

Typical income documentation requirements – Canadian mortgage

Below are the typical income documentation requirements for each type of income.

-

Salaried employees & commission income

Salaried

Salaried and hourly employees may need to supply:

- A job letter and a recent pay stub to show consistent salary

If your hours aren’t guaranteed or if there is a lot of overtime, you may also be asked for a 2-year income history.

Commissioned

Commissioned salespeople typically need the same documents as a salaried employee except they may also need to provide:

- 2 years of T1 Generals with corresponding NOA’s – Notice of Assessments to establish a 2-year income average.

-

Self-employed: Incorporated & Sole Proprietor

Incorporated

Self-employed clients who are incorporated and can provide traditional income verification may need to supply:

- Most current T1 General including statements of business activities. To establish a stable income, but also so a lender can see your sources of income.

- Confirmation of no taxes owed

- Accountant prepared company financials supported by business bank statements. To establish your company is in good financial standing and to compare the income level being pulled out of the company is sustainable.

- Current corporate search to confirm business ownership.

Sole Proprietor

Self-employed clients who are sole proprietors and can provide traditional income verification may need to supply:

- Most current T1 General including statements of business activities. To establish a stable income, and so a lender can see their sources of income.

- Confirmation no taxes owed

- One of the following: Business license/registration, trade license, or GST registrations/returns to prove business ownership/partnership

Alternative provable income & other documentation

Alternative provable income verification

This is a proprietary, specialized approach using gross-ups and add-backs available.

Alternative verification of income can be provided via the following documents:

Sole proprietor/partnership

- Most current T1 General

- Confirmation no taxes owed

- Recent financial statements or statement of business activities to indicate a level of income

- One of the following: business license/registration, trade license, or GST registrations/returns to prove business ownership/partnership

Incorporated or limited company

- Most current accountant prepared financials or corporate T2s

- Most current T1 General and confirmation no taxes owed

- Corporate search/articles of incorporation – for business ownership

- Six months of bank statements

Gross-ups and add-backs approach is considered in this instance.

Other documentation

There are other income sources that can help your client’s application get approved.

-

-

- Canada Child Benefit (CCB)

- Alimony/child support

- Government and/or private pension

- Rental property income

- EI benefit for maternity leave

-

Buying a Rental property — this is the income documentation needed.

You can verify rental income via the following:

- Full T1 Generals showing net rental income

- If not reported in T1 General, market rent from an approved appraiser

Verified Income

- A job letter and recent paystub. If the client’s hours aren’t guaranteed, underwriter may also ask for a 2-year income history.

Alternative Proveable Income

Proprietary, specialized approach using gross-ups and add-backs.

Sole Proprieter

- Most current T1 General

- Confirmation no taxes owed

- Recent financial statements or statement of business activities supported by business bank statements

- One of the following: business license/registration, trade license or GST registration/returns

Incorporated or limited company

- Most current accountant prepared financials or corporate T2s

- Most current T1 Generals and confirmation no taxes owed

- Corporate search/articles of incorporation

- Six months bank statements