What Income Do You Need to Buy a House in Calgary? Real Examples

How Much Income Do You Need to Buy a House in Calgary?

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

One of the first questions many home buyers ask is:

“How much income do I need to buy a house in Calgary?”

Quick Answer (Snippet Call-Out)

In Calgary, a household earning about $100,000 per year can typically afford a home between $450,000 and $500,000, assuming a 5–10% down payment, good credit, minimal debt, and current Canadian mortgage stress test rules.

The exact number depends on several factors including your down payment, existing debts, and the mortgage rate used in the stress test.

Below are realistic examples based on typical Calgary home buying scenarios.

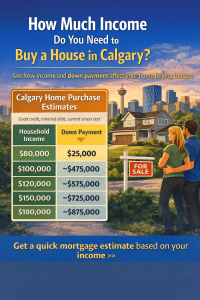

Example chart showing estimated home prices in Calgary based on household income and typical mortgage approval guidelines.

Example: Income vs Home Price in Calgary

These examples assume:

-

Good credit

-

Minimal debt

-

25-year amortization

-

Current Canadian mortgage stress test rules

-

Average Calgary property taxes

| Household Income | Down Payment | Estimated Purchase Price |

|---|---|---|

| $80,000 | $25,000 | ~$400,000 |

| $100,000 | $30,000 | ~$475,000 |

| $120,000 | $40,000 | ~$575,000 |

| $150,000 | $60,000 | ~$725,000 |

| $180,000 | $80,000 | ~$875,000 |

Calgary remains one of the more affordable major cities in Canada, which is why many first-time buyers are surprised by how much home they may qualify for.

How Mortgage Lenders Calculate Affordability in Canada

Canadian lenders use two main ratios to determine mortgage affordability.

Gross Debt Service (GDS)

Gross Debt Service measures the percentage of your income that goes toward housing costs.

Housing costs include:

-

mortgage payment

-

property taxes

-

heating costs

-

condo fees (if applicable)

Most lenders require GDS to stay below 39% of gross income.

Total Debt Service (TDS)

Total Debt Service includes all other monthly debts such as:

-

car loans

-

student loans

-

credit cards

-

lines of credit

Most lenders require TDS below 44% of income.

If your debts are higher, your mortgage approval amount may decrease.

The Mortgage Stress Test Explained

All insured mortgages in Canada must pass the mortgage stress test.

This means buyers must qualify at:

-

the contract mortgage rate or

-

the government qualifying rate

whichever is higher.

The stress test ensures borrowers can still afford payments if interest rates rise.

How Your Down Payment Changes Your Buying Power

Your down payment affects both your approval amount and whether mortgage insurance is required.

Minimum down payment rules in Canada:

-

5% on the first $500,000

-

10% on the portion between $500,000 and $999,999

-

20% for homes $1 million or higher

Many Calgary first-time buyers purchase homes using 5% down payment programs.

How Debt Affects Mortgage Approval

Existing debt can significantly reduce borrowing power.

Example:

| Monthly Debt | Approximate Mortgage Reduction |

|---|---|

| $300 car payment | ~$60,000 less borrowing power |

| $600 debt payments | ~$120,000 less borrowing power |

Paying down consumer debt before applying for a mortgage can dramatically increase your approval amount.

Calgary First-Time Buyers Often Qualify Sooner Than Expected

Many buyers assume they need a very high income before purchasing their first home.

However, programs such as:

-

insured mortgages

-

5% down payments

-

extended amortizations

allow buyers to enter the Calgary housing market earlier than they expect.

Calgary Mortgage FAQ

What salary do you need to buy a house in Calgary?

Most buyers need a household income between $90,000 and $120,000 to comfortably afford homes priced between $450,000 and $600,000, depending on their down payment and debt levels.

Can I buy a house in Calgary with $80k income?

Yes. Buyers earning around $80,000 per year may qualify for homes around $375,000 to $425,000, assuming minimal debt and a typical down payment.

How much mortgage can I qualify for in Calgary?

Most lenders allow housing costs up to 39% of gross income and total debts up to 44% of income, subject to the mortgage stress test.

Get a Personalized Mortgage Estimate

Online examples are helpful, but every mortgage approval depends on:

-

income structure

-

employment history

-

credit score

-

debt levels

-

down payment

If you want a personalized estimate of how much house you could afford in Calgary, feel free to reach out.

I’m happy to review your situation and give you a realistic price range before you start house hunting.

Author

Mark Herman, MBA

Mortgage Broker – 22 Years of Experience

Mark helps Calgary home buyers navigate mortgage approvals, complex income situations, and lender options. His goal is to help clients secure the right mortgage strategy before they start shopping for a home.