Fixed vs Variable Mortgage Calgary 2026 | Should You Lock In Now?

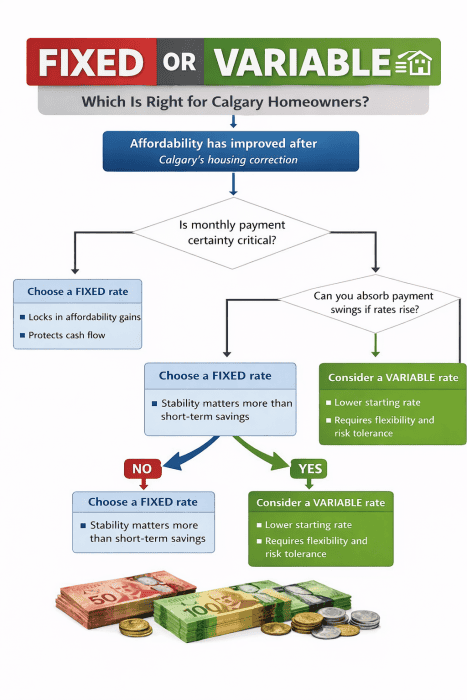

Fixed vs Variable Mortgage in Calgary (2026): Why Locking In May Be the Safer Move Right Now

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

Mortgage rates in Canada—and specifically here in Calgary—are starting to trend upward again. After a period where variable rates often came out ahead, the risk equation has shifted.

Mortgage Penalty Calculator Canada: How Fixed-Rate Penalties Are Calculated (2026 Guide)

Written by Mark Herman; MBA in Finance – Mortgage Broker with 22 Years of Experience

Quick Answer: Mortgage Penalty in Canada

If you break a fixed-rate mortgage in Canada, your penalty is usually:

- 3 months’ interest, or

- Interest Rate Differential (IRD)

You pay whichever is higher.

Most fixed-rate penalties in 2026 fall between:

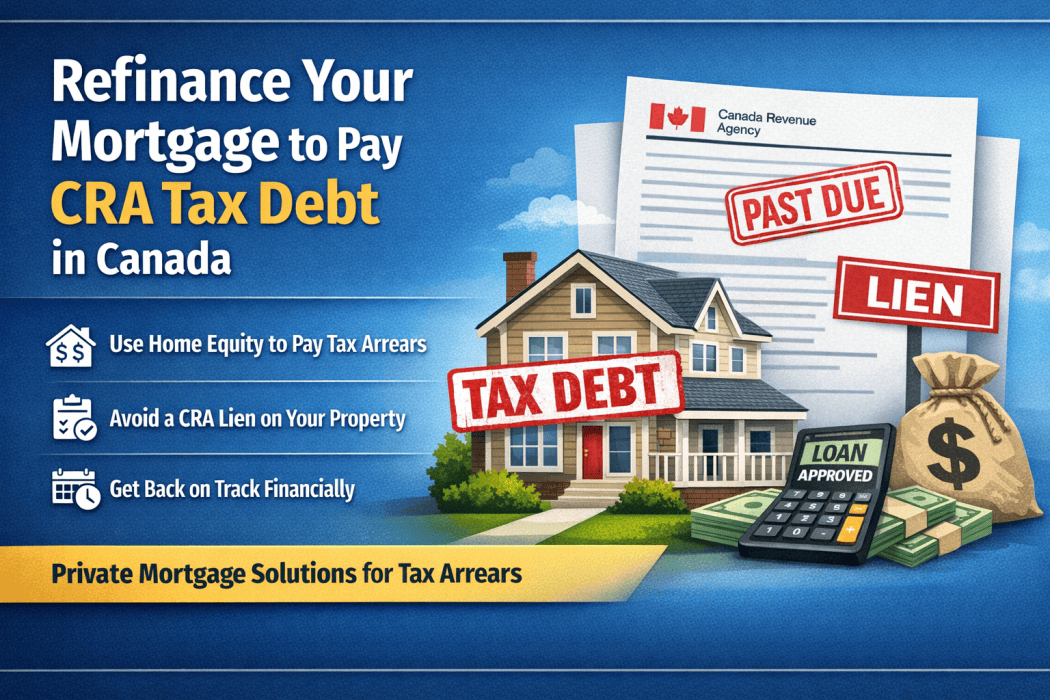

Can I Use a Mortgage to Pay CRA Tax Debt in Canada? (A Real Example of a Private Refinance)

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience specializing in new home buyers and tough deals.

Many Calgary and Canadian homeowners are surprised to learn that the CRA can place a lien on their home for unpaid taxes. Once that happens, refinancing becomes much harder.

What Income Do You Need to Buy a House in Calgary? Real Examples

How Much Income Do You Need to Buy a House in Calgary?

Written by Mark Herman, MBA – Mortgage Broker with 22 Years of Experience

One of the first questions many home buyers ask is:

“How much income do I need to buy a house in Calgary?”

Quick Answer (Snippet Call-Out)

In Calgary, a household earning about $100,000 per year can typically afford a home between $450,000 and $500,000, assuming a 5–10% down payment, good credit, minimal debt, and current Canadian mortgage stress test rules.

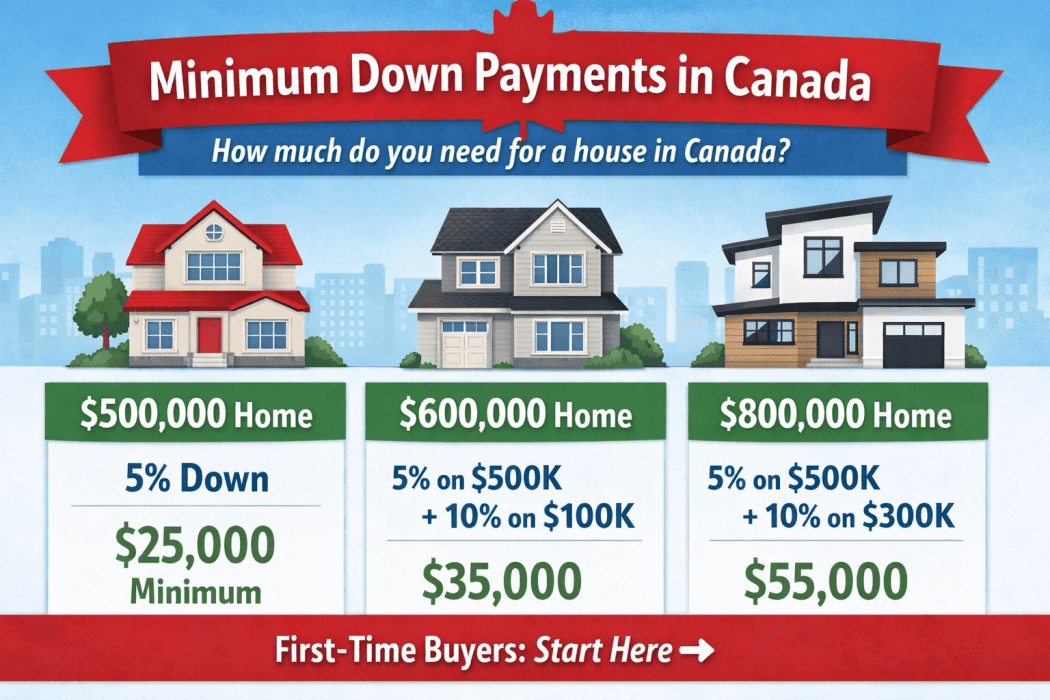

Minimum Down Payment Canada: Rules, Examples & Options, 2026 Guide for Home Buyers

Specific details of down payment requirements for home buyers in Canada 2026

OnlyFans Mortgage in Canada: How Content Creators Can Get Approved (A-Lender vs B-Lender Options)

OnlyFans Mortgage in Canada: How Content Creators Can Get Approved (Even Without a “Traditional” Job)

If you earn income through OnlyFans, YouTube, TikTok, Twitch, Instagram, or any other online platform, you’ve probably wondered:

Can I actually qualify for a mortgage in Canada with this kind of income?

Approved: Mortgage with U.S. Income, Remote Work & Gifted Down Payment (CMHC Deal)

Cross-Border Mortgage Approved: U.S. Income + Gift Funds + CMHC

This Mortgage Deal Looked Impossible (But CMHC Approved It Anyway)

We recently completed a mortgage deal that even I assumed is impossible.

We got it done — and now that we’ve successfully navigated the process, we’re ready to help more buyers in similar situations.

Advice on Mortgage Renewals Before April 2026 from an MBA

Questions on what product to pick for your upcoming mortgage renewal.

Here are the reasons that we like the 5 year fixed for Canadian mortgage renewals over the next few months.

(renewals from now, February 2nd until April 1st.)

Stress Test Continues; Was Almost Abolished

It seems to be a good thing that all the mortgages since 2018 have been “stress tested” at 5.25%. Now that we are in the middle of 3.6 million mortgages renewing over an 18 month period we find that most everyone is able to make their new mortgage payments after renewal.

Mortgage Mark Herman, MBA in Finance and 22 years experience as a mortgage broker in Western Canada

Nerd alert here!!

OSFI has also determined that loan-to-income (LTI) limits on each institution’s mortgage portfolio will remain in place, alongside the existing stress test.

LTI limits have been in place since each institution’s 2025 fiscal year start and are reported on a quarterly basis.

This is a limit on the volume of newly originated uninsured mortgage loans, at that financial institution, that exceed a 4.5x loan-to-income multiple. This is not a limit on each individual loan.

This measure was introduced in an effort to lessen the build-up of highly leveraged residential mortgage borrowers.

Buying a Home with a Basement Suite – Some Details

Buying a home with a basement suite can be a powerful way to increase affordability, improve cash flow, and build long-term wealth — but not all suites (or lenders) are treated the same. If you’re considering a home with a suite, here are four important things to think about before you buy.

1) The type of suite matters.

If a suite is legal (fully permitted and meets municipal bylaws), all lenders will accept the rental income for qualification. If it’s not legal, make sure it’s at least fully self-contained, meaning it has its own entrance, its own kitchen, and its own bathroom. Many lenders will still consider rental income from these types of suites, but not all.

2) Your lender choice can change how much you qualify for.

Different lenders treat rental income very differently. Some will only allow 50% of the rental income to be used, while others allow up to 100%. Some lenders make you debt-service property taxes and heat, while others do not. These differences can have a huge impact on your approval amount, which is why working with a broker who understands rental income policy is so important.

3) Whether the suite is already rented or not DOES matter.