Investment Mortgages WILL Be Harder to Get in 2023!

Its true! This thing called Basel 3 will make it harder to get an investment mortgage in 2023!

Lots of junk below, the short version is:

Canadian banks will need to apply more risk to investor mortgages and to lower that risk they may:

- Increase the down payment needed from 20% to a higher amount … maybe 25% or 30%

- Lend to fewer investors – which already make up 25% to 30% of the Canadian market.

- New Zealand already started 40% down payment for investment properties!

“Avoid the new rules by buying your investment property in 2022!

Mortgage Mark Herman, top Calgary, Alberta mortgage broker.”

Canadian Economic Data Points Affecting Mortgages

Below are the Bank of Canada’s updated comments on the state of the economy, the Bank and singled out the unprovoked invasion of Ukraine by Russia as a “major new source of uncertainty” that will add to inflation “around the world,” and have negative impacts on confidence that could weigh on global growth.

Rates and Prices Trending Up Due to Inflation and War

Mid-March Commentary: Rates and Prices Trending Up Due to Inflation! and War!!

On March 2nd, 2022, the Bank of Canada made its most anticipated decision on interest rates since the pandemic began. After weeks of speculation and anticipation of an increase, central bankers finally pulled the trigger and moved their overnight rate higher.

List of Data Needed for Lo/No Condition Offers

Documents needed for Low/ No Condition Offers are below.

For Employees:

Employment Data

- Employment letter ** – order from payroll or HR

- 2 x recent pay slips

Tax Data

- Last 2 years of your NOAs – Notice of Assessments – you get them back after you pay your federal income taxes

- Last 2 years T4’s – to verify continued employment in your industry

Confirmation of down payment

90 days of detailed account history is needed – by way of:

- 3 months of on-line bank statements (print-out to PDF and email is perfect) showing funds on deposit AND / OR

- For RRSP/ TFSA funds: 3 x monthly account statements OR at least 2 statements, 3 months apart OR a year-end summary and recent statement.

- If your name is not on the statements please print the “welcome page” that should show your name AND last few digits of the account numbers so they can be cross referenced.

** Employment letter – A letter of employment is needed that includes the following:

What Are the Risks Of Unconditional Offers When Buying A Home?

The process of buying a home and completing a real estate transaction typically centers on the offer. After finding the home you want to buy, you’ll need to submit an offer, which the seller will review before signing off on it.

Bank of Canada holds benchmark interest rate steady & updates 2022 economic outlook

Summary:

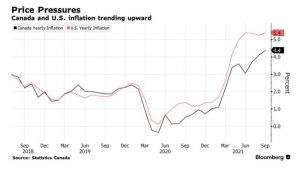

- There may be fewer increases if inflation returns to the target of 2% from today’s 40 year high of about 5%.

- The USA is seeing record 7% inflation and Canada usually gets dragged along with the US numbers so that balances the possibility of fewer increases.

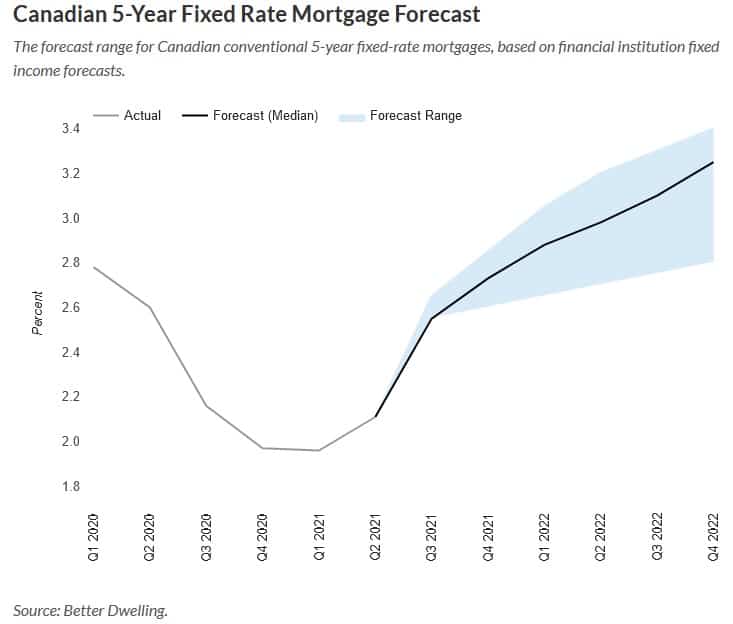

Mortgage Rates Up Due to Inflation

|