Data on those negative amortization mortgages

Queston 1: What about all these (negative amortizing) mortgages that will now take 71 years to pay off?

Answer:

Yes, they are called VRMs – Variable rate Mortgages – and we don’t really offer/sell /even talk about them for that exact reason – what if the rates rates jump? And they did.

Winning Variable Rate Strategy: end-2023

Here are the current Canadian mortgage rates and the Variable looks to be the best for these reasons ...

When Will Canadian Mortgage Rates Begin to Fall?

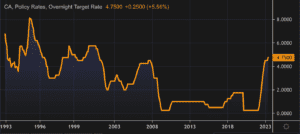

Last week, the Bank of Canada held its policy rate at 5%. The decision was expected given slowing in the economy and modest improvement to core inflation measures.

The Bank is likely at the end of its tightening cycle. How soon it eases rates – and how low will rates go in the near to medium term – is the question #1

Canadian Economic Forecast – Nov- Mortgage related use

Bank of Canada holds its interest rate steady, publishes updated economic forecasts

On October 25th, the Bank of Canada announced that it would maintain its Canadian Prime Rate stays at 7.3% – stating that there is “growing evidence” that past interest rate increases are dampening economic activity and relieving price pressures.

Persistent inflation leads the Bank of Canada to increase benchmark interest rate

UGH! The BoC whacks borrowers again.

Mark Herman, Top Calgary Alberta Mortgage Broker

Yesterday, the Bank of Canada increased its overnight interest rate to 5.00% (+0.25% from June) because of the “accumulation of evidence” that excess demand and elevated core inflation are both proving more persistent and after taking into account its “revised outlook for economic activity and inflation.”

Canadian economy running too hot, BoC increases Prime by .25%

Hot Economic growth leads the Bank of Canada to increase its benchmark interest rate

Today, the Bank of Canada increased its overnight interest rate to 4.75% (+0.25% from April) because of higher-than-expected growth in Canada’s economy in the first quarter and the view that monetary policy was not yet restrictive enough to bring inflation down to target.

BoC Holds Canadian Prime at 6.7% on April 12th – Good News!

Today, April 12, 2023, the Bank of Canada held its policy interest rate at 4.50%, a welcome outcome for borrowers after almost a year of constant increases, and a timely confidence-builder for the real estate industry as it enters the spring market.

Using Return-To-Work Income while on Maternity Leave to buy a home IS possible in Canada.

Using Return-To-Work Income while on Maternity Leave to buy a home IS possible in Canada.

Are you on maternity leave and trying to buy a home, but the bank will not use your income? This is a common reason home buyers find us on the internet or their realtors send them to us.

Bank of Canada increases its benchmark interest rate to 4.50%

Today, the Bank of Canada increased its overnight benchmark interest rate 25 basis point to 4.50% from 4.25% in December. This is the eighth time since March 2022 that the Bank has tightened money supply to address inflation.

New Mortgage Rules 2023: Expanding the “Stress Test” to Everything?

This is from the Desk of Dr. Cooper, our Economist, and this data is 1 of the reason we are at Dominion Lending – to get this data.

Below is the details of the government expanding the STRESS TEST, or other mechanisms, to make it harder to buy a home.